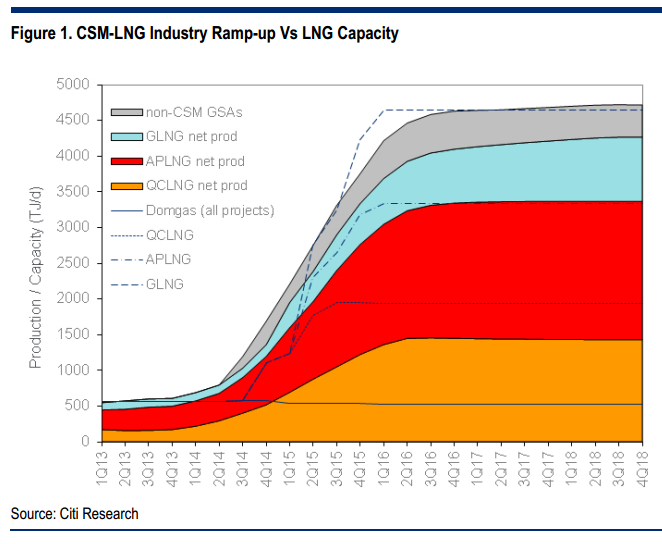

Given upstream delays, CSM-LNG looks short gas — We have built well-by-well models to define likely gas production for the GLNG, APLNG and QCLNG projects. Given delays in upstream facilities of 3-6 months for all projects, we think the industry will be short gas for 12 months from 4Q15, when all 6 LNG Trains are operational. We forecast each project will face supply shortages which limit ramp-up of respective second trains. Given these project delays, we expect APLNG will only supply ~135PJ to QCLNG in first 2 years (not 190PJ), and we no longer forecast an excess of APLNG gas during its ramp-up – reducing the options GLNG has for find 3rd party gas to fill ullage.

We think all 3 projects are looking for short term gas, and will remain in market longer term — Based on our forecasts, all three projects are short gas to some extent short term and, while well outperformance (peak-rates / ramp-up) vs conservative planning assumptions could resolve shortfall, companies are likely to de-risk gas supply by contracting additional 3rd party gas if available. We think all projects will remain in market for vols longer term to maximise capital efficiency by buying gas on long-term supply if cheaper than developing own resources. We think such a decision should be seen as a prudent use of capital, but may disappoint some.

Higher domgas prices to be underpinned by ongoing market participation — We estimate it is DCF neutral (10% IRR) for a project like GLNG to buy gas at ~A$7/GJ and offset drilling, buy gas at ~A$8/GJ to delay developments of new fields (ie Arcadia CY19), and DCF neutral to buy gas at ~A$12/GJ to back-fill when reserves decline. While short-term ullage in LNG facilities may see gas spike to A$10-12/GJ for 12 months from 4Q15, we think gas prices will return to ~A$8/GJ longer term, in the absence of material new volumes of cheap gas and/or material high price demand.

Small window for shortfall, limited opportunity for Cooper unconventional — We forecast a small window of opportunity for 3rd parties to supply the CSM-LNG industry at higher prices before the industry moves towards being self-sufficient. We think the producers/retailers that can benefit from this market tightness are those with uncontracted gas in this time frame, including ORG (which has option to supply ~57TJ/d to GLNG or higher priced domestic market, and gas flexibility in generation portfolio, & Ironbark development), and STO (Kipper project ~75TJ/d – STO 75% interest first 2 years).

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.