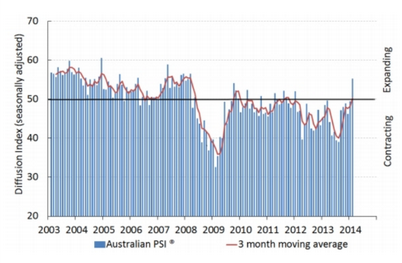

The AIG Performance of Services (PSI) is out this morning and will give the cyclically-focused more to crow about:

The latest seasonally adjusted Australian Industry Group Australian Performance of Services Index (Australian PSI®) jumped by 5.8 points to 55.2 points in February.

This was the first expansion for the Australian PSI® (a reading above 50 points) since January 2012 and the highest reading since March 2008.

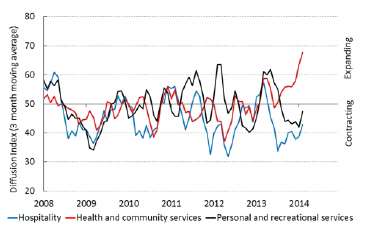

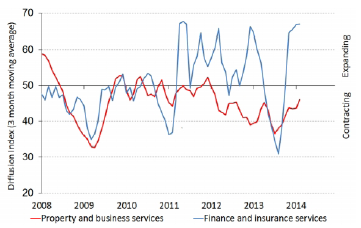

Despite the strong result in the Australian PSI® this month, growth was concentrated in just a few services sectors, primarily health and community services (67.7 points) and finance and insurance (67.0 points). Both of these sub-sectors have been performing more strongly than other services sub-sectors over the last six months, and both are relatively large – and therefore statistically dominant – in the Australian PSI®.

Other sub-sectors improved but remained below 50 points. The large retail trade subsector moved very close to stabilising at 49.5 points (in 3 month moving averages).

Feedback from respondents in many services sector indicates that local demand conditions remain challenging for a large number of services businesses and the outlook continues to be fragile for them.

All of the activity sub-indexes of the Australian PSI® moved above 50 points in February. The sales sub-index rose to its highest level (58.8 points) since October 2009, while the new orders sub-index pointed towards a second month of expansion. Services employment also expanded in February following two months of contraction (readings below 50 points). In addition, both the supplier deliveries and stocks sub-indexes strengthened to above 50 points this month, suggesting businesses were replenishing their stock levels after the Christmas/New Year trading period.

That’s a much more decisive jump out of recession than we’ve seen in many months. However, as the AIG itself says, it’s very narrow, with expansion confined to just health and finance:

Advertisement

I’ve got no reason for the jump in health and community services. Perhaps attending ailments is the first phase of purse loosening. Finance could rightly be seen as a leading indicator for a broadening of activity but that hasn’t been the case over the previous three years.

Here are the internals:

Advertisement

More evidence of cyclical bounce and perhaps a hint of broadening. It’s good to see some momentum in services as we head into the capex cliff. At least now it’s a little bit of a contest.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.