The Abbott government yesterday confirmed that it will push ahead with plans to sell Medibank Private through an initial public offering (IPO) next financial year, in a move which industry analysts expect will raise around $4 billion for the government.

In October last year, the Government launched a scoping study into the sale, which according to Finance Minister Mathias Cormann “reaffirmed our long-held view that there is no compelling reason for the government to own Medibank Private…[and]…found no evidence that premiums would increase as a result of the sale of Medibank Private”.

The Government is expected to recycle proceeds from the sale into “productivity-enhancing infrastructure” projects.

Whether Medibank’s privatisation is likely to be a winner for the public hinges on it passing two broad tests.

The first is purely financial, and depends on whether the upfront funds received by the Government will outweigh the expected net present value of future dividends.

The opposition’s finance spokesman, Tony Burke, claims that the government would lose annual dividends of up to $500 million by selling Medibank, adding to the long-term deficit.

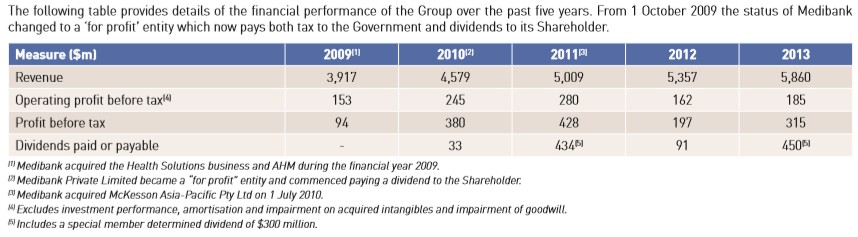

However, a quick analysis of Medibank’s 2013 annual report shows that Medibank averaged profit before tax of $330 million over the past 4 years, implying an average net profit after tax of $231 million (assuming a 30% tax rate).

Given dividends can only be sustainably paid out of profits, Labor’s $500 million dividend claim appears to be highly exaggerated, with the real sustainable figure likely to be around half that level.

Whether the sale price of $4 billion outweighs the loss of future dividends would depend on the discount rate applied, as well as assumptions about profit growth and perhaps the economic and social returns from the alternative infrastructure investments funded from the sale. What we can say with certainty is that the Budgetary impact from Medibank’s sale is nowhere near as dire as implied by Labor.

The second test that needs to be satisfied is whether the privatisation of Medibank is beneficial from an efficiency or equity perspective. Given that Medibank competes directly with a range of private health insurers, and there is already significant competition in the marketplace, there would not appear to be any competition concerns arising from Medibank’s sale. The new private owner would not be able to unnecessarily raise premiums and gouge consumers for risk of losing market share to its competitors.

Balancing up the above considerations, there would appear to be reasonable grounds for privatising Medibank.