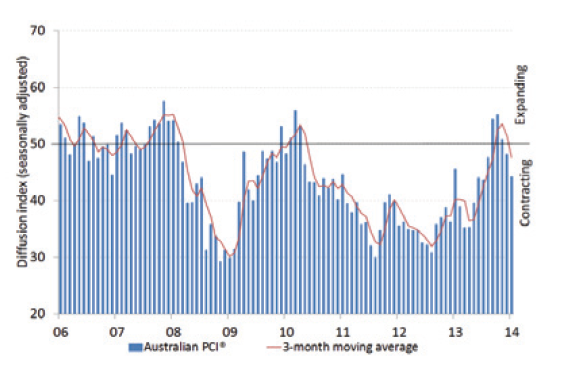

The national construction industry contracted at a steeper rate in February as activity returned to negative territory for the first time in five months, after a sharper fall in new orders. Reflecting this deterioration, both employment and deliveries from suppliers continued to decline.

The seasonally adjusted Australian Industry Group/ Housing Industry Association Australian Performance of Construction Index (Australian PCI®) fell by 4.0 points to 44.2 points in February. This was below the critical 50 points level that separates expansion from contraction and signalled the industry’s weakest performance in six months.

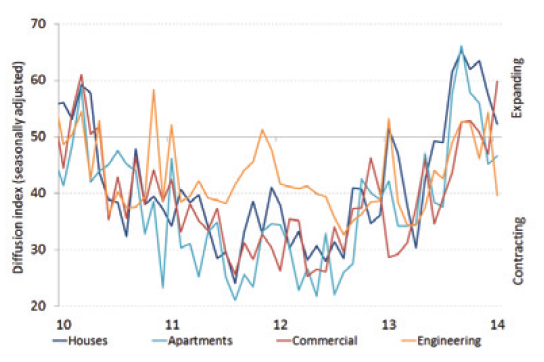

Across the construction sub-sectors, house building activity showed continued growth in February, although its rate of expansion moderated to the slowest pace in the past six months.

A return to growth was evident in commercial construction, which helped to soften the overall decline in construction activity. This sector’s rate of expansion picked up to its fastest rate in almost four years. Weighing heavily on the headline Australian PCI® however, engineering construction activity turned down sharply in February, to be at its most subdued level in the past eight months. Apartment construction also contracted for a second consecutive month, albeit at a slightly slower pace than in January.

This latest set-back in industry conditions coincided with reports of fewer new contracts and project completions, most notably in the engineering construction sector. Tight credit conditions and a lack of public sector tenders were other major factors generally cited as inhibiting activity. House builders pointed to a reduction in new orders and fewer customer inquiries, although investor activity was seen as remaining resilient in the house building sector.

Activity was OK in residential despite a bad trend:

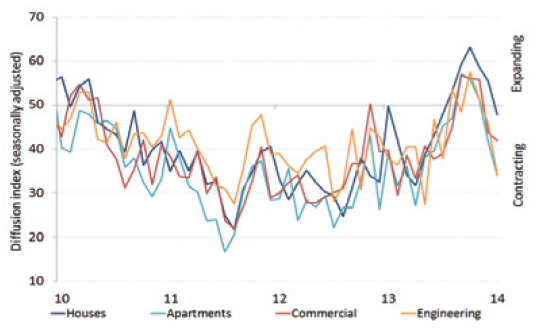

New orders fell across the board:

Advertisement

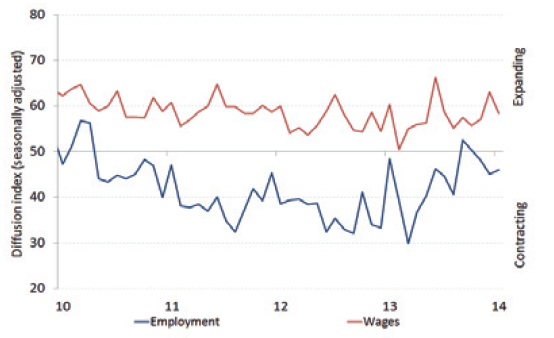

And employment is still contracting:

Here are the internals:

One could be tempted to see the leading edge of softening consumer sentiment in falling residential new orders but these indexes are not reliable enough to draw that conclusion. At this stage I’d put it down to volatility. It is totally unreliable when it comes to engineering construction. Still, a poor report.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.