For those with a memory, it was the positive findings of a study by the macro consultancy NERA for the US Department of Energy that opened the way for the US entry into global LNG markets. That study has been updated:

This report is an update to the study of the macroeconomic impacts of liquefied natural gas (LNG) exports that was issued by the US Department of Energy (DOE) in December 2012. The new study, “Updated Macroeconomic Impacts of LNG Exports from the United States,” updates all 63 LNG export scenarios modeled in the DOE study and adds several new scenarios. The new study, which was sponsored by Cheniere Energy, Inc., includes additional analysis of the cumulative impacts of LNG exports up to the maximum amounts that the market would allow under various domestic and international market scenarios.

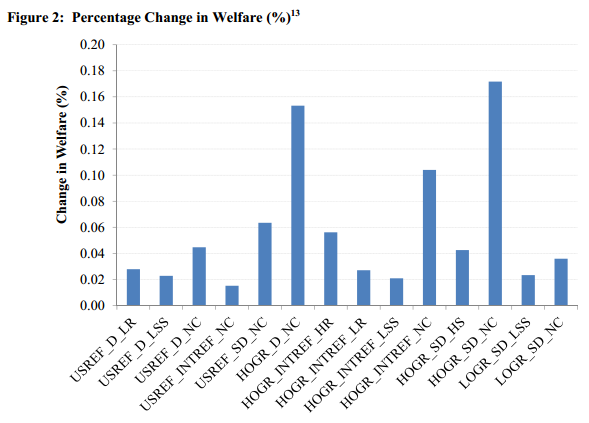

The findings of the updated study confirm and extend the findings of the previous study that were endorsed by DOE in its Freeport Order (No. 3282) and subsequent LNG application approvals. LNG exports provide net economic benefits in all the scenarios investigated, and the greater the level of exports, the greater the benefits. The market for LNG exports is self-limiting, in that little or no natural gas will be exported if the price of natural gas in the US increases much above current expectations. High levels of exports can be expected only if natural gas is plentiful and inexpensive enough to produce so that prices remain below current levels, even with high levels of exports.

The new report responds to several issues raised since the DOE issued NERA’s first report, including use of more current data, the cumulative impacts of additional license approvals, impacts on the competitiveness of the US chemicals industry, and impacts of LNG exports on employment.

The new report is based on the EIA’s Annual Energy Outlook 2013 and International Energy Outlook 2013, which provide the most recent relevant data and available forecasts. The study findings show that the US is projected to remain one of the lowest cost producers of chemicals in the world even with the highest levels of LNG exports considered. For its longer-term forecasts of impacts on jobs creation, the NERA study uses the same assumption as the most recent Congressional Budget Office budget and economic outlook: the economy will return to effective full employment by 2018. The investment required by 2018 to build export facilities and increase natural gas production will speed the predicted return to full employment and is forecast to put up to 45,000 currently unemployed workers back to work during this period.

In short, the more the better. Full report here. Meanwhile, if you’d like to know on which side of the sovereign fence The Australian sits, check out the uncritically recycled propaganda leading its business section today from US Ambassador John Berry, from a trip funded by the Australian-American Leadership Dialogue:

“We are in the market now. We will continue to be in the market in the future. That may increase the competitive pressures but Australia will be able to very effectively compete,” Mr Berry told The Australian.

“The demand that is going to be in Asia — from Japan, Indonesia, Vietnam, Malaysia, China, from all of those places together — is an enormous demand that cannot only accommodate Australia but the US and more.

“This is a marketplace that needs this cleaner source of energy so we can continue economic progress in a cleaner way than we have been able to in the past. It is in both of our interests to encourage the development of our respective markets to meet that demand.”

Australian producers are also battling multi-billion-dollar cost blowouts because of soaring labour and raw materials costs.

Asked if these could make Australian projects less competitive with their US rivals, Mr Berry said: “Companies are smart — they make their own projections and they rise and fall based on the quality of those projections. Australian companies are pretty darn good at that, as are US companies. I have full confidence that both are going to be successful in this marketplace for the foreseeable future.”

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.