From Westpac, here is their latest on jobs growth in the next quarter or so. I agree with these findings and am getting some reports of my own from sources in middle management employment agencies that a little bull run is underway. Positions like business and change managers, project managers etc are in demand suddenly. These are ‘first hires’ for new capex and likely to trickle down to more in the coming months.

There are two issues that I can see with this report. The first is Westpac does not discount the distortions within the February numbers enough. The underlying trend was better but not as much as they make out. Second, the estimates of how much jobs can grow as investment shrinks strike me hopeful beyond the first half. Still, by and large I agree with the report’s conclusion for the short term.

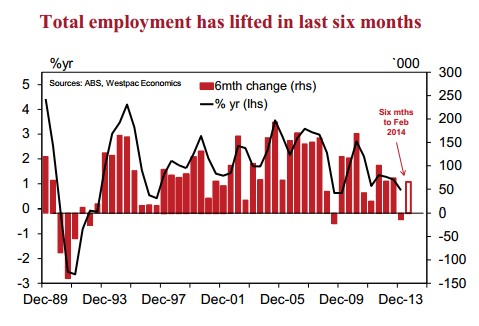

While one month does not make a trend, in Feb total employment rose 47.3k rise – full-time employment rose 80.5k, male employment +51k – was much stronger than expected and break the soft patch through 2013H2. In fact, in the six months to Feb total employment has lifted 65.4k, full-time employment is up 33.7k and male employment has risen 50.6k.

Compare this to the 13.8k fall in employment in the six months to Dec 2013, full-time employment was down 53.2k and male employment had fallen 18.9k. We are interested in male employment as has tended to be more cyclical being linked to the industries such as mining, construction, manufacturing, transport and wholesale.

Given this shift in momentum in employment we thought it was timely to release a chart pack of our suite of leading indicators. This includes the various business surveys, consumer unemployment expectations, job ads and Westpac’s outlook for non-mining investment, domestic demand and household demand.

The first set is based on the various business surveys that are released. We compile the employment indicators from the surveys – questions on employment (actual & expected), overtime worked (actual and expected) –to generate composite employment indicators. By using as many surveys as possible we hope to create a deep (covers many firms) and broad (covers many sectors) employment indicator as possible. Westpac’s Jobs Index lifted to 48.6 in Feb from 48.3 in Jan and a recent low of 44.4 in Apr 2013.

The Westpac-Melbourne Institute Unemployment Expectations Index provides an insight not only on household perception of the labour market but it is also a real time indictor of the strength of the labour market. Unemployment Expectations rose 5.5% in Mar; up 8.6% so far in 2014 and 17.7% higher in 12 months. But the recent lift in the Westpac Jobs Index, if it flows through to a lift in employment, should translate into an improvement in unemployment expectations.

Job advertisements rose 5.1% in Feb, the strongest monthly rise since the 11.1%mth print in Feb 2010. The robust Feb rise breaks a long down trend with job ads falling in 21 of the 23 months leading up to Feb. Job ads are now down just 4.8%yr (they troughed at –18.8%yr in Jun 2013). Ads are, however, still at a historic low level and 21% below the Feb 2012 print. The business surveys suggest the recent upturn is likely to be sustained.

Westpac focuses on household demand (household consumption plus dwelling investment) as a key lead indicator of employment turning points – it suggests a more positive Q1 compared to Q4.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.