This time it’s from Nomura via the AFR:

Analysts at Japanese broker Nomura said in a note: “Can growth stabilise without a major change of policy stance? We believe it cannot, as tight labour market conditions suggest that potential growth has already dropped to around 7 per cent or below.

“From a cyclical perspective, the cumulative policy tightening since mid-2013 will likely damage investment momentum in coming quarters unless the policy stance loosens.”

…“When short-term objectives are challenged, the government usually shifts its focus toward promoting growth,” the analysts wrote. “We have witnessed this ‘two step forward, one step back’ style of policy swings in the past.”

Policy levers that the central government looks most likely to pull include cuts to banks’ reserve requirement ratio (RRR) to boost growth amid high overall financing costs. Nomura’s analysts are tipping RRR cuts of half a percentage point in the second quarter of this year, and further easing of half a percentage point in the third quarter.

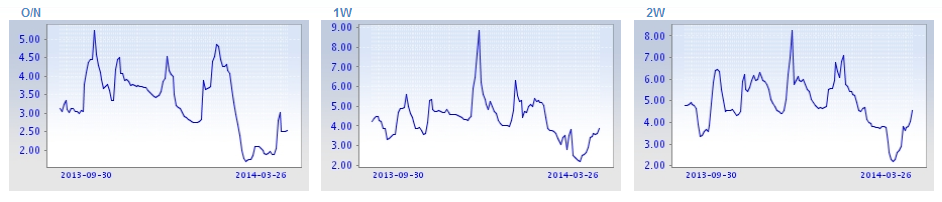

I don’t think so. Recent PBOC policies have been tightening credit again. SHIBOR appears to be returning to its former previously tight range:

Though that may also be the result of the traditional end of month lending binge. But Reuters is reporting tight credit conditions:

Some of China’s struggling firms are finally getting the reception that regulators have been hoping for — a cold shoulder from banks in the form of smaller and costlier loans.

Reuters has contacted over 80 companies with elevated debt ratios or problems with overcapacity. Interviews with 15 that agreed to discuss their funding showed that more discriminate lending, long a missing ingredient of China’s economic transformation, has become a reality.

Up against a cooling Chinese economy and signs that authorities will not step in every time a loan goes bad, banks are becoming more hard-nosed and selective about whom they lend to.

There are signs that even state-owned firms, in the past fawned over by lenders for their government connections, have to contend with higher rates, lower lending limits and more onerous checks by banks.

…To be sure, several companies with strong balance sheets and profits reported no significant changes in their funding conditions.

That in itself is a welcome sign that banks are finally differentiating between the strong and the weak, more aware that they are on the hook for losses if businesses fail.

The recent move to dump the yuan also mitigates against hopes for monetary easing. It is an explicit warning to hot money flow to stay out and that chokes credit. Back to Nomura:

Nomura’s analysts said: “Policymakers do not want to give the impression they are embarking on wholesale easing, as it risks reigniting excesses in shadow financing, [local government financing vehicles], property and hot money inflows.

“We view this policy easing as similar to the easing in the second half of 2013, when total social financing rose in the absence of any government-announced major stimulus.”

That’s it. It will will be fiscal, it will be targeted, it will be stimulus but it will be disguised.