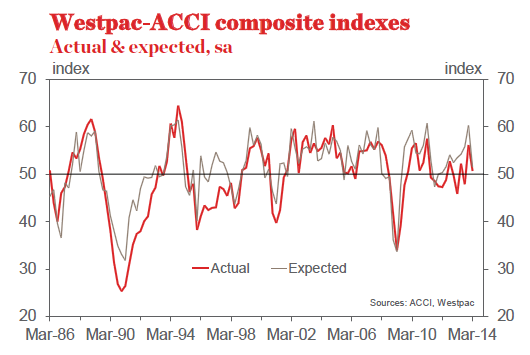

Following the retracement in the NAB business survey last week, two more out today show similar falls. The first is the Westpac-ACCI manufacturing index:

The Westpac-ACCI Actual Composite printed at 50.9 in the March quarter, down 5.4pts from 56.2 in the final quarter of 2013.

A pull-back of the index in the March quarter could be viewed as an indication that strength in December was a one-off post Federal election bounce. However, the balance of evidence suggests that this, the first backto- back expansionary reading for the sector since early 2011, is suggestive of improved conditions.

Manufacturing is benefitting from a strengthening of consumer spending and a housing building upswing, as well as a modest lift in export orders.

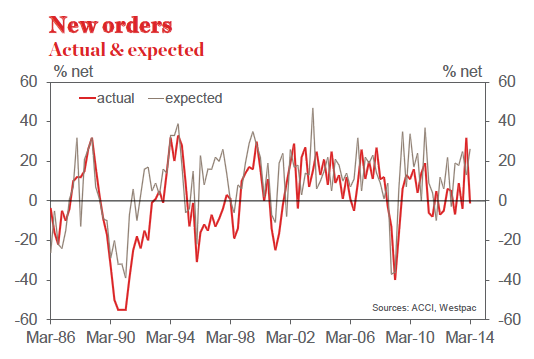

New orders were broadly flat in the March quarter, with a net 1% reporting a decline. A consolidation was to be expected following the strongest reading since 1994 the quarter prior. Recent strength in orders is having flow-on effects to the labour market and spare capacity, which has decreased from mid-2013 levels.

Respondents remain optimistic, with a net 17% of firms in the March quarter expecting the general business environment to improve over the coming six months. The average for the past three quarters is +26%, a level well above trend and up from +6% over the first half of 2013.

Jobs growth across the Australian economy is likely to improve over the coming six months, as suggested by the survey’s Labour Market Composite index, which was positive for a second consecutive quarter.

Selling prices are on the rise, following persistent cuts over the four year period 2009 to 2012, reflective of a lift in import costs flowing through the pricing chain.

Profits and wages remain under pressure. Profit expectations turned negative in the quarter and a net 31% of firms expect their next wage deal to deliver wage growth below the last, which is below the 2009 low.

Investment prospects remain uncertain at this stage of the cycle. A plus is that firms report that the ease of accessing finance is the most favourable since 1999.

While the overall positive tone of the survey over the past two quarters is welcome, the durability of this upturn remains uncertain. The recent retreat of consumer sentiment raises the risk of a mid-year setback.

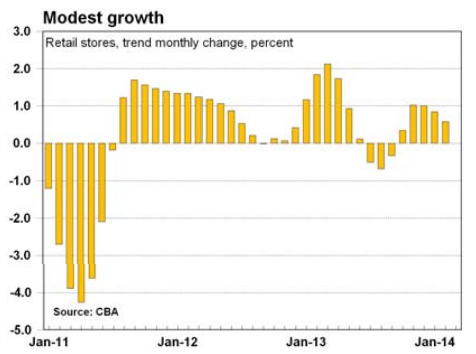

Economy-wide spending expanded at a slower, more sustainable pace in February according to a new survey. The Commonwealth Bank Business Sales Indicator (BSI) – a measure of economy-wide spending– rose by 0.7 per cent in trend terms in February, down from 1.0 per cent in January, 1.1 per cent in December and 1.2 per cent in November. It was the 18th consecutive month of spending growth.

The more volatile seasonally adjusted estimate of spending eased by 0.3 per cent in February after lifting by 2.2 per cent in January. Annual growth eased from 11.9 per cent to 10.7 per cent in the month.

The seasonally adjusted and trend estimates of the BSI results are derived via the SEASABS statistical program from the Australian Bureau of Statistics.

At a sectoral level, 17 of the 19 industry sectors expanded in trend terms in February, a similar result to December and January. And for the sixth straight month, seven of the eight states and territories recorded firmer sales in trend terms in February.

The Commonwealth BSI is obtained by tracking the value of credit and debit card transactions processed through Commonwealth Bank merchant facilities. The BSI covers spending broadly across the economy rather than just retail sales, including spending on automobiles, personal services and airlines.

Advertisement

If you look through CBA’s reflexively bullish spin it looks like a fading pulse.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.