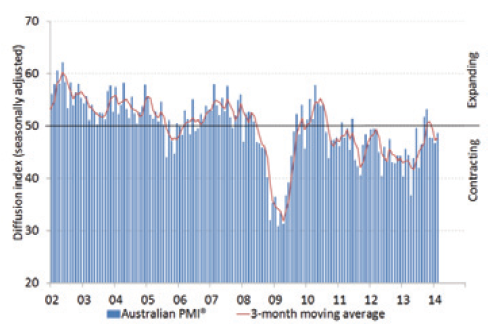

The latest Australian Industry Group Australian Performance of Manufacturing Index (Australian PMI®) firmed by 1.9 points in February, rising to 48.6 points (seasonally adjusted). The Australian PMI® has signalled contraction in the sector in each of the past four months (readings below 50 points indicate contraction), following a brief period of expansion in September and October 2013.

This month the production sub-index of the Australian PMI® showed a strong improvement, increasing by 6.3 points to 51.5 points. The new orders sub-index also edged higher in February to reach 50.0 points, suggesting new orders were broadly stable in February. The sub-indexes for employment, stocks and supplier deliveries however, continued to indicate contraction in the month with readings below 50 points. Export markets remain extremely tough for manufacturers, with the sub-index falling below 30 points again in February.

Manufacturing selling prices stabilised at 50.3 points in February, with this sub-index moving (marginally) above 50 points for the first time in almost three years. Input prices continue to rise strongly however and margins remain under significant pressure.

Across the sub-sectors, the food and beverages sub-sector has now being expanding (readings above 50 points) since March 2013 (three month moving averages). The petroleum, coal, chemicals and rubber products sub-sector index indicated growth for a second month. Both nonmetallic minerals and wood and paper products expanded in February, in line with rising construction activity. In contrast, the large metal products and machinery and equipment manufacturing sub-sectors continued to contract in February (three month moving averages).

Several respondents to the Australian PMI® said the Australian dollar is still too high to support their business. A number of respondents voiced their concerns for the broader manufacturing sector arising from Toyota’s announcement in early February that it will cease Australian automotive production in 2017. Feedback from participants indicates that this announcement has already affected business confidence.

The internals are nothing flash but if you squint you’ll some hope of a rebound with trends in selling prices and new orders firming:

And it looks like ye auld j-curve is at work in the falling dollar with costs rising more than demand and margins likely to get worse before they get better:

Advertisement

Comfort yourself in the knowledge that it’s a shit sector of rent-seekers that we don’t need anyway! Full report here.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.