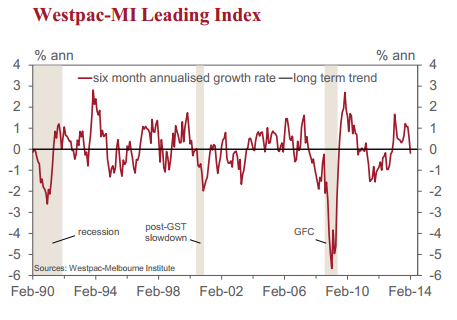

The six month annualised deviation from trend growth rate of the Westpac Melbourne Institute Leading Index which indicates the likely pace of economic growth three to nine months into the future fell from 0.53% in January to –0.19% in February.

The Index is showing a sharp loss of momentum since late 2013 with February marking the first sub-trend reading since December 2012. That earlier period was part of a two year stretch in which the Leading Index registered below trend growth rates in 22 out of 24 months. The economy struggled to sustain momentum in 2012 and early 2013 and although conditions have improved since June, today’s Leading Index result points to a loss of momentum heading into mid-2014. That is consistent with Westpac’s view that GDP growth remains sluggish at 2.7% in 2014.

The sharp slowdown since October has seen the Leading Index growth rate drop from 1.22% to –0.19%. The main drivers of the 141bp swing have been: weakening in the Expectations component of the Westpac Melbourne Institute Index of Consumer Sentiment (–51bps) and the Westpac Melbourne Institute Index of Unemployment Expectations (–29bps); and moderating positive signals from the yield curve (–41bps) and dwelling approvals (–0.16bps). Declining commodity prices and hours worked have also contributed to the slowdown (–9bps and –5bps respectively).

These negatives outweighed gains in the S&P/ASX 200 (+2bps) and rising US industrial production (+9bps). The level of the Index fell by 0.06 points (0.06%) in February. Three of the eight components contributed positively and five negatively in the month. The S&P/ASX 200 index rose 4.06%, US industrial production was up 0.62% and dwelling approvals rose by a further 6.6%. More than offsetting this was the Westpac- Melbourne Institute Unemployment Expectations Index, which rose 5.3% (recalling that higher readings on this Index indicate a more pessimistic outlook), and declines in the Westpac-Melbourne Institute Consumer Sentiment expectations index (–0.8%), commodity prices (–2.2%) and aggregate monthly hours worked (–0.9%). The yield spread also narrowed by 7bps.

The Reserve Bank Board next meets on April 1. This week Westpac revised its outlook for the overnight cash rate by no longer forecasting rate cuts in the second half of 2014. This decision was partly made because of the considerable comfort that the Board holds with the current policy stance. That was clear in the minutes to the RBA’s March Board meeting released yesterday with the Bank pointing to gradual improvement in the economy; and expectations that growth in 2015 will be a little above trend and inflation contained within the 2-3% band. These are the hallmarks of a central bank that anticipates remaining on hold for some extended period. The Bank is setting a very high hurdle for any further policy stimulus.

We still see a number of headwinds for employment; the consumer; business investment and confidence restraining the

pace of recovery. Today’s Leading Index report already points to a significant loss of momentum consistent with this view. However we do not expect the type of growth profile emerging over the course of the next 12 months that would shock the Bank out of its current comfort zone.

Reader will know I’m no huge fan of this index’s predictive powers, even if I agree with it today.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.