From Westpac’s Elliot Clarke comes the below interesting update on the US housing market:

This week we return to familiar territory: the housing market. We attempt to disentangle noise from signal in the recent data, rather than merely screaming “weather” and moving on.

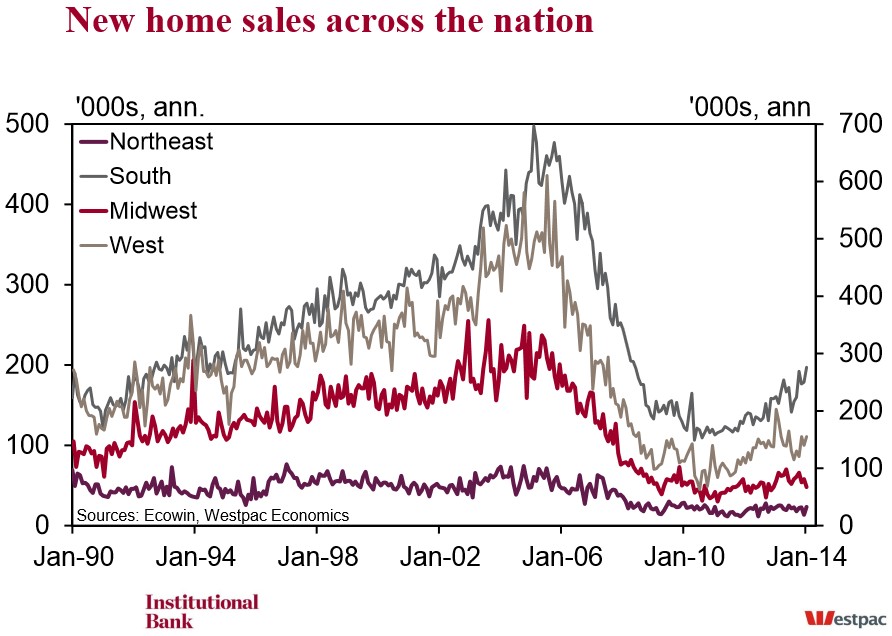

Over the three months to January 2014, existing home sales have fallen 9.9% while new home sales rose 3.5%. At face value, the argument in favour of the weather being to blame finds support in the first result, but not the latter. However, by region, there is clearer evidence in favour of a weather effect for existing and new sales. For existing, the Midwest and Northeast have seen respective declines of 9.6% and 4.6%. And for new homes, sales in the Midwest have fallen by over 27%, though they have risen by 6.5% in the Northeast. (Being a very small market in a volatile survey, there may be a greater sampling issue in the Northeast; that said, the Midwest market is not much larger.)

While we have no issue with saying that the unseasonable weather has negatively impacted activity (particularly in the Midwest), other housing market detail point to underlying weakness not associated with the weather.

For new home sales, high volatility and limited signal is the key takeout. In the South, sales growth has clearly slowed, with sales up 2.6% over the past three months versus 11.6% in the previous four. And in the West, sales have rebounded 29% in the past three months following a 27% slump over the four months to October. The picture does not become much clearer when we consider the change over the past year: over this period, sales have risen 23% in the South and 3.1% in the Northeast, but have fallen 14% in the Midwest and 23% in the West. Abstracting from this volatility, what we clearly can say about new home sales is that they remain at historically low levels, with gains focused in the South.

Turning to existing sales, we find a picture of broad-based weakness. Apart from the falls noted above for the Midwest and Northeast, the West has also seen a 2.8% decline in sales over the three months to January, and sales in the South have fallen 2.0%. From these regional results, there is clearly evidence in favour of a weak underlying trend, sans the weather.

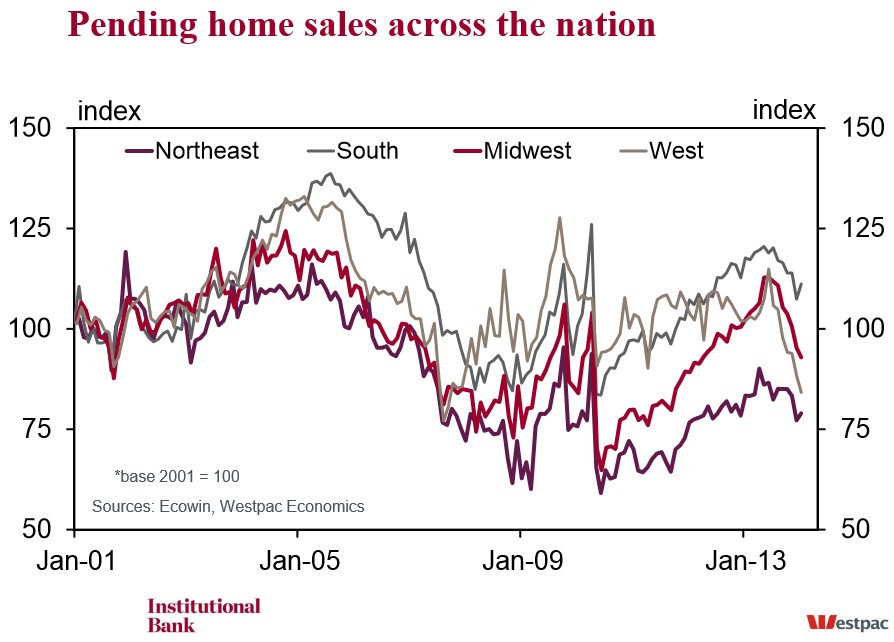

Aside from the breadth of this weakness, another key point which needs to be recognised is that existing home sales are measured at closing. As such, they represent transactions which likely commenced two months prior to the recorded month. Hence, much of the weakness noted above actually pre-dates the weather. Extending our sample period, we actually see that the peak in existing and pending sales (measures sales of existing homes at the time contracts are signed as opposed to deal completion) was in the middle of 2013. Since this time, both series have declined by around 14%. So, while the weather may have accentuated the weakness, it was not the catalyst.

If the weather is not the primary catalyst, what is? Two other factors are clearly at play. The first is affordability, current and projected. Affordability can be decomposed into three parts. The price of housing; the level of income; and the cost of servicing mortgage debt. All other things unchanged, a rise in the first or the last reduces affordability. A rise in income increases it.

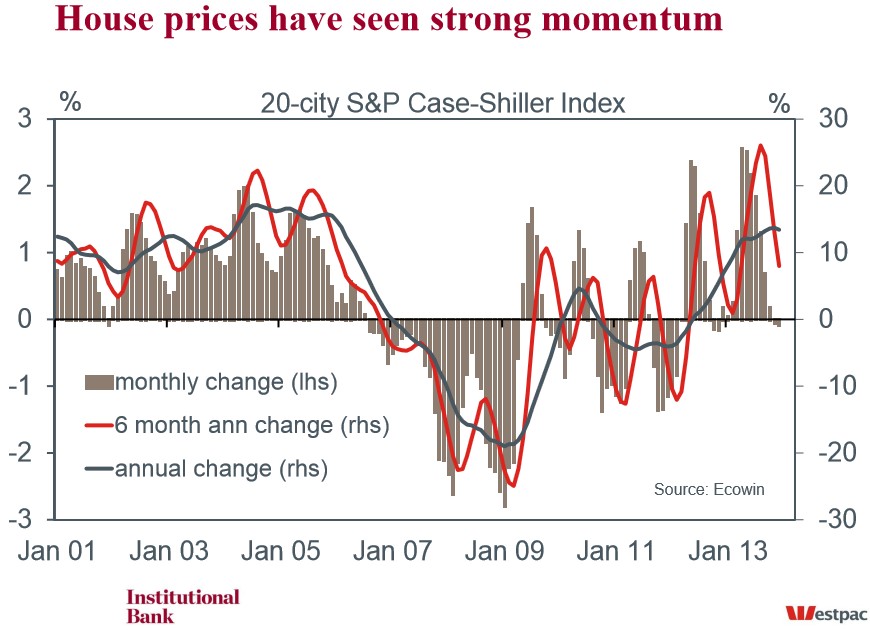

We have detailed at length on numerous occasions the absence of real discretionary income growth for households. House price inflation coming out of the trough has been of the double-digit variety, leaving those on average incomes behind. And, while it is not strictly related to the narrow definition of affordability, households’ growing stock of student and auto liabilities, not to mention pre-GFC housing debt, holds credit scores down and reduces how much can be borrowed. As detailed last week, that many young US households only have poor-to-fair credit scores and that bank lending standards remain tight makes house purchase all the more problematic. Affordability is also highly vulnerable to a rise in term interest rates. We saw this at times in 2013 due to speculation over tapering, and the impact on refinancing activity was large and immediate. Highlighting the impact higher rates and prices have had, since early May 2013, mortgage purchase approvals have fallen around 23% and refinancing approvals have fallen a staggering 69%.

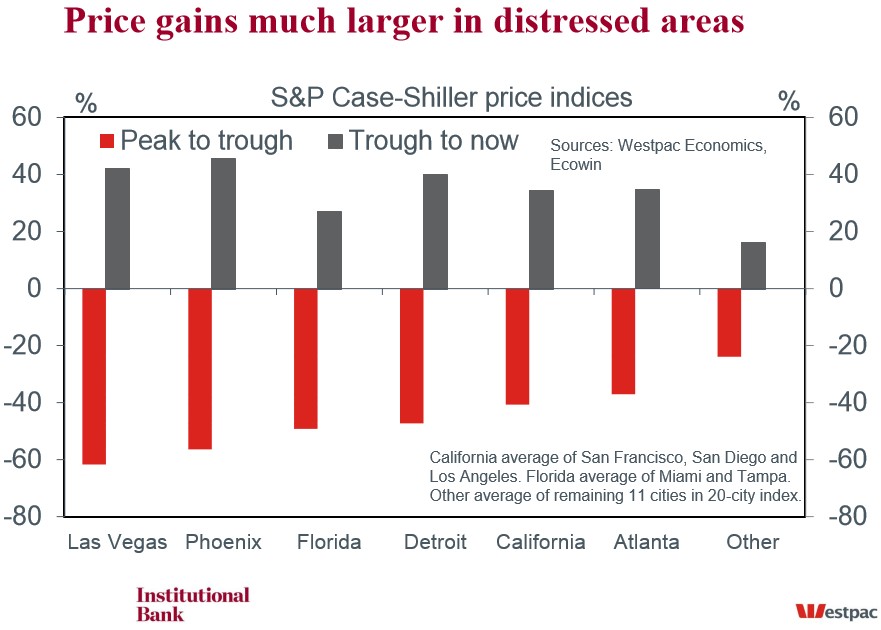

The second factor which needs to be discussed is the importance of investors to the residential property market, particularly in areas hard hit by the GFC. As we highlighted last November, areas such as Las Vegas, Phoenix and Detroit continue to experience soft economic conditions, yet prices have risen by around 40% from their respective troughs, seemingly in large part due to investor activity, not owner occupiers. The removal of excess supply from the market is a positive, as is the benefit to existing home owners’ balance sheets of higher prices. However, there is reason to suspect investors have now pushed prices above the level an ordinary household can afford. If this proves to be true, weaker investor appetite – institutional investors’ share of residential sales fell to 5.2% in January 2014 versus 7.9% in December and 8.2% a year ago, according to RealtyTrac – gives cause for concern over the structural integrity of the US housing market. The immediate effect is simply that, absent the rekindling of investor interest, price growth is unlikely to surge again. Not only that, but materially adverse conditions could return to the housing market should economic conditions disappoint.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.