For two years I’ve been harping on this theme and Mac Bank today delivers categorical support:

Growth a story of international vs. domestic

Offshore exposures better growth opportunities at this stage of economic cycle

We continue to prefer Global Cyclical stocks for their access to greater growth opportunities offshore and higher earnings leverage. Australian companies are increasingly recognising opportunities to expand offshore into new markets as a source & driver of growth. This reporting season alone the following companies have talked to increasing investment & resources to support expansion into these regions including:

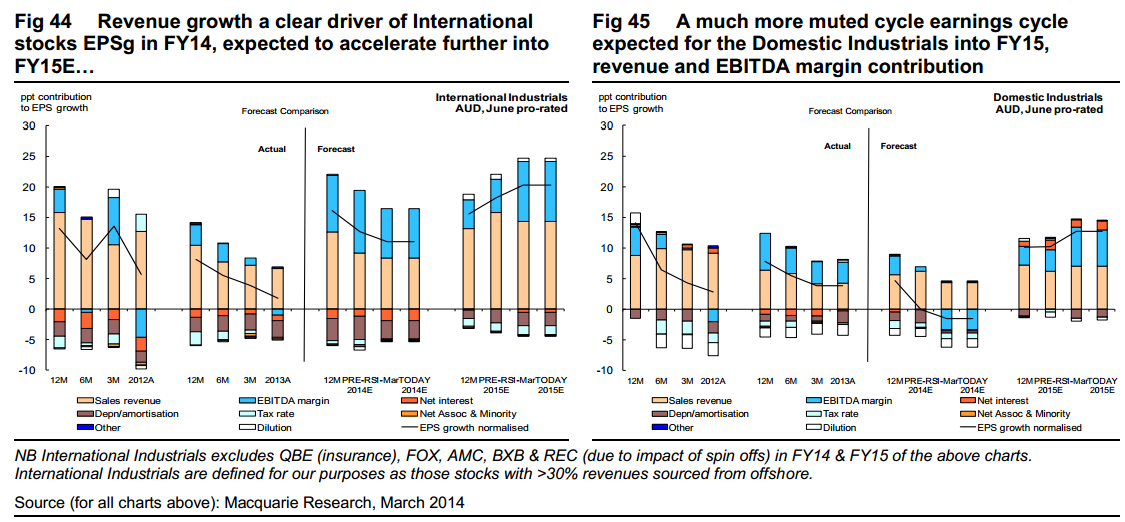

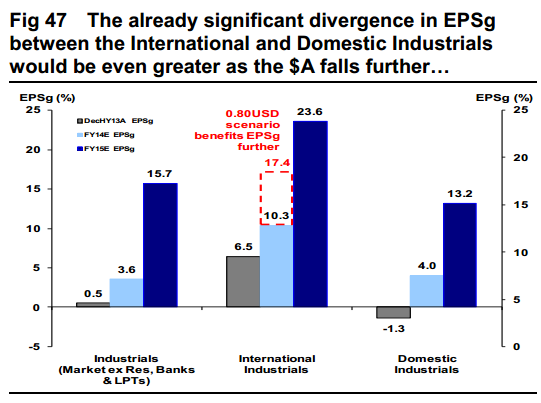

…[the] distinction in economic cycles between Australia & its developed world peers suggests that those companies able to access offshore markets have and will be able to drive higher earnings growth (including stocks listed above). This was already evident this reporting season, with many standout DecHY13 results being driven by stocks’ international assets.

That’s the macro backdrop we’re all now familiar with and profits season has borne it out:

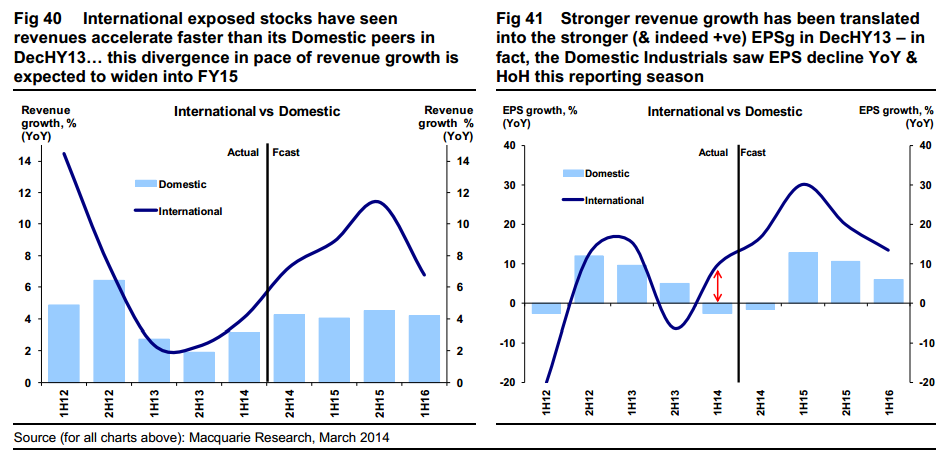

This reporting season saw the International exposed stocks’ revenues accelerate faster than its Domestic peers in the DecHY13 and the pace of revenue growth is expected to widen into FY15. The International Industrials grew revenues by +4.1% YoY compared with its domestic peer group at +3.2%. Both are expected to see revenues accelerate into the JunHY14 and into FY15 however the International stocks are expected to accelerate at a much faster pace, widening the divergence (see Fig 40 below) to the Domestic Industrials, which is expected to see a less cyclical profile of revenue growth.

Advertisement

And then there’s the upside (and hedge) in the dollar:

Avoid miners with their toxic exposure to China and where earnings forecasts are all going to get caned in the months ahead. International industrials are the growth play with a built-in hedge!

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.