From Businessweek:

With plans for dozens of the multibillion-dollar export terminals in North America alone, the industry is headed toward an overbuild that may depress Asian prices for a decade, according to a Rice University analysis. Capacity from proposed North American LNG terminals is more than triple the forecast growth in Asian gas demand by 2020, data from HSB Solomon Associates LLC’s Ziff Energy Group show.

“Capital flows to where it sees opportunity and everybody’s trying to grab that flag first,” Kenneth B. Medlock III, senior director of the Center for Energy Studies at Rice University’s Baker Institute for Public Policy in Houston, said in a March 3 interview. “What happens is that you see too many people trying to grab the flag.”

…The industry won’t overbuild LNG export capacity because the facilities are too expensive to do without signed contracts from buyers in hand, John Watson, chief executive officer of Chevron, told reporters yesterday after speaking at the CERAWeek conference. Many of the proposals will fall away without guaranteed buyers so supply won’t exceed demand, he said.

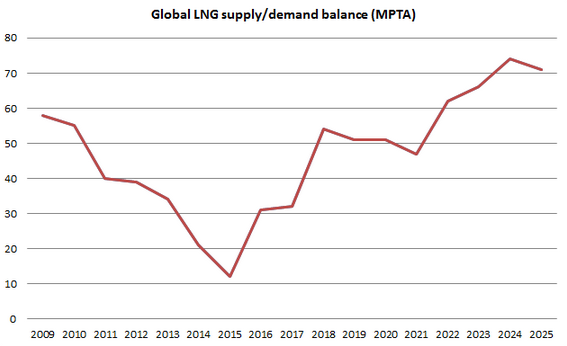

This is another way to frame the argument I’ve been making for two years that Australia’s projects are going to come under price pressures from 2017 and even more so from 2020 as global competition rises. Here is the supply and demand balance chart once more:

This forecast includes the current batch of approved DOE US exporters and the IEA sees this scenario eventually driving prices close to the $12mmbtu break even cost for Australia’s magnificently expensive seven.

If the US approves more projects the market will tilt further in favour of supply. Though it is likely true that new Australian projects won’t be built without long-term contracts (Woodside is proceeding with Browse FLNG for now without any) other international projects that can undercut Australian costs can do so.

Ironically, the very existence of Australia’s contract-underpinned seven projects at the wrong end of the cost curve, where they are the marginal or swing supplier, means cheaper late comers can proceed with less certain customer commitment.