1. A significant step toward stimulus would be a step back from reforms intended to control runaway corporate credit and local government debt. Doing so might risk a sharper correction down the road.

2. The State Council’s statement suggests little in the way of new government spending. It promises to accelerate existing projects rather than to start new ones, indicating little additional impetus from the public purse.

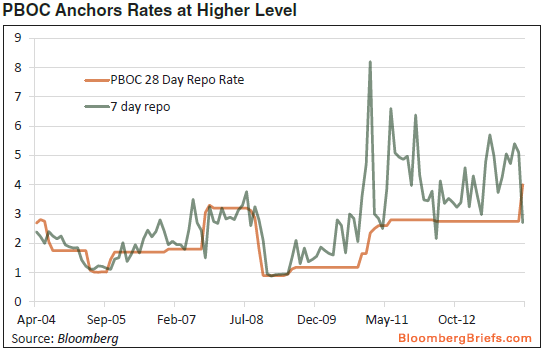

3. Similarly, the People’s Bank of China’s recent reintroduction of the 28-day repo at a rate of 4 percent suggests the central bank wants to re-anchor rates at a higher level. At the recent National People’s Congress, PBOC Governor Zhou Xiaochuan said interest rate liberalization is on an accelerated track and isexpected to push rates higher.

4. A growing number of analysts expect a cut in the reserve requirement ratio, which would boost bank lending. The reserve requirement ratio is a blunt instrument, and a cut would signal to the markets that the central bank is stepping back from its deleveraging agenda. Finetuning liquidity via open-market operations may be a preferable alternative at this point.

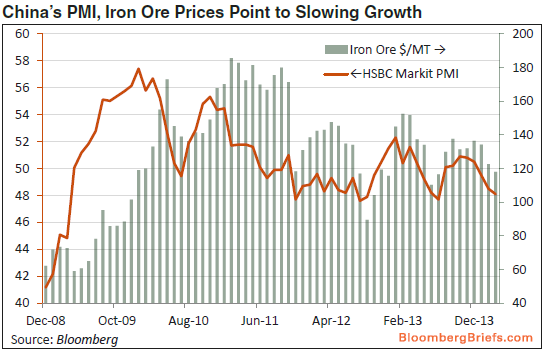

5. In the details of the PMI release, deteriorating output and new orders paint a bleak picture of domestic demand. Rebounding export orders suggest February’s pronounced drop might overstate the weakness of foreign sales. Employment showed signs of stabilizing. Labor markets are a primary focus for China’s policy makers, and that’s another reason to think a wholesale shift to stimulus may not be in the cards.

Statement 1, 3 and 4 are right. Statement 2 is a semantic game; accelerated spending is stimulus. Statement 5 is right but of marginal value.

Bloomberg Briefs also released a special report on mining and Chinese reform:

The new China is likely to be one of more moderation, discipline and control. China’s raw material production system

has relatively high electricity costs. Large hydro or nuclear or natural gas-driven turbines provide the lowest-cost electric power. To keep costs as low as possible in China, pollution controls were not put in place. In addition, lower-quality coals are used to produce power and a lower-cost form of nickel called “nickel pig iron.” As a result, China is suffering from contamination and its new government has decided to take action.

The implementation of this new “war on pollution” has already started to take place. The government is vowing to cut 27.5 million metric tons of highly polluting steel mills and 30 million metric tons of cement capacity. This is a small percentage of China’s more than 1 billion metric ton capacity, yet it is the largest cut of old, inefficient capacity that the country has ever taken, and equates to almost one-third of U.S. capacity.

With less steelmaking capacity may come a decline in steel production. The third plenum calls for moderation — of pollution and of the country’s fast and perhaps undisciplined lending practices — with new controls and taxes being placed on growth. This may result in lower steel demand, meaning decreased iron ore imports, and could benefit the global aluminum industry by increasing imports due to the shutting of smelters in China.

The new property taxes being considered would have a multi-pronged impact. A large number of vacant apartments may need to be filled by rent-paying tenants to cover the property taxes. This may slow development of new apartment buildings. A decline in growth in the building industry may cut demand for steel, copper and other base metals.

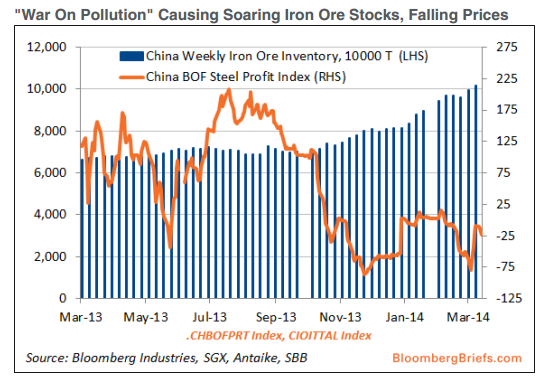

Recent increases in inventories, along with falling prices, may be the first signs of these slowdowns and market observers should carefully monitor these trends, which are tracked weekly and monthly in the Bloomberg Industries data modules and presented in BI’s metals and mining research.

Also correct.

China will stimulate but it will be more targeted and less commodity intensive in the past and will not take the pressure off the over-indebted sectors of property and steel.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.