Markets are ruthless. That’s why they’re (sometimes!) efficient. I do not expect a long or difficult period of adjustment to the emerging reality of Ukraine’s situation.

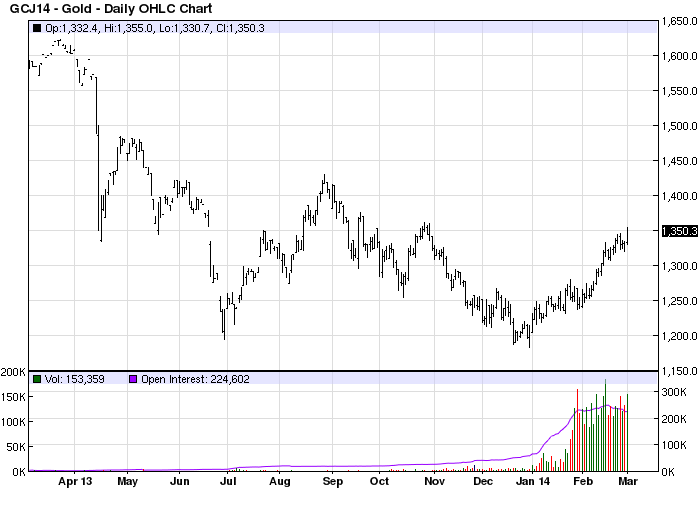

Yes, overnight gold jumped a couple of percent to within spitting distance of another technical breakout:

But I don’t buy it. In fact, I’d consider fading it. In the scheme of things, Ukraine is just not that big a deal. Why? Because it’s a client state of Russia and Russia intends to keep it that way. It sits firmly within Russia’s sphere of influence and the only action that could change that is if Ukraine were to join NATO, an outcome that has now been circumvented.

There is nothing anyone can do about it. The US is too weak and its interests are not served by intervention. Europe is too divided and is over the barrel of Russian gas supplies.

The main risk to markets and economies comes from the Urainian’s themselves. If their blood gets up in defense of a different national vision than that Vladimir Putin has in mind then a civil war would be very difficult for Europe to handle as gas becomes a strategic bargaining chip.

In that event, it’s not easy to see what Europe would do. Its interests would be better served by selling out Ukraine that fighting a proxy war that drove its gas prices to crippling highs.

Gold, then, will have support so long as Ukraine itself makes noise about a desire for independence.

The market moves that have hit Russia’s currency, debt and equity markets – Moscow’s Micex index fell by 10.8 per cent and the central bank jacked rates by 1.5 percentage points to 7 per cent as the rouble fell to all-time lows against the US dollar – seem to me to be over-reactions to the strategic reality.

As for wider markets, some reaction looks about right. The S&P down one percent is an acknowledgement of risk with appropriate larger falls in European markets on the gas risk. The US bond market was heavily bid, however, with yields on the thirty year close to breaking down at 3.55% and the ten year likewise at 2.6%. This was despite generally positive economic news with US ISM firming in February at 53.2% and a decent Personal Income and Outlays report which showed consumer spending on trend in January despite the weather. The data was taper positive so it’s worth watching what this means.

Forex markets were fairly calm. The yen and US dollar both enjoyed a little safe haven strength and the Aussie was flat.

For the time being at least, markets are well short of panic over Ukraine .