The submission first provides nine metrics illustrating Australia’s residential property bubble, which include the following:

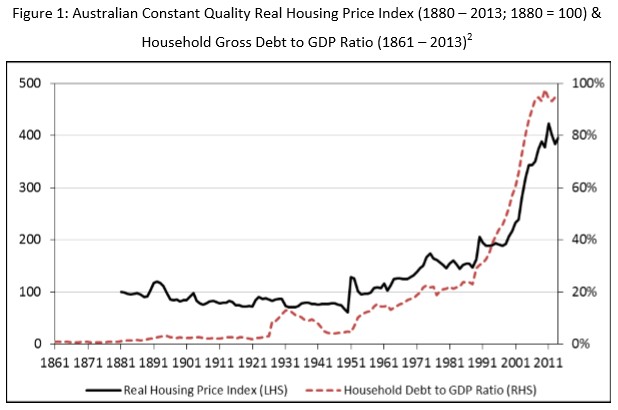

It took forty years from 1950 to 1990 for housing prices to double, but only fifteen years between 1996 and 2010 to double again. The surge in housing prices is driven by the tremendous growth in household debt, as owner-occupiers and investors take out ever larger mortgages to speculate on housing. The household debt to GDP ratio reached a record high of 98 per cent in 2010, the same year real housing prices peaked. In 2013, the mortgage and personal debt ratios were 86 and 9 per cent, respectively, for a combined household debt ratio of 95 per cent.

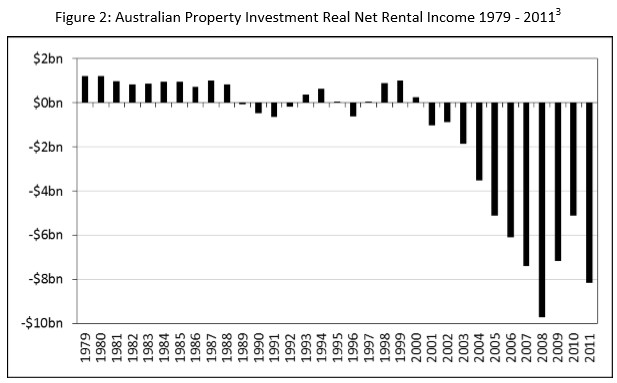

As mortgage debt escalated, investors’ net rental losses increased rapidly from 2001 onwards. In that year, net rental income losses were just over $1 billion, rising to $9.7 billion in 2008 as the cash rate peaked at 7.2 per cent. By 2010, when mortgage debt reached its historical peak relative to GDP, investor losses eased to $5.1 billion as the cash rate fell to a then historic low of 3 per cent in 2009 following the global financial crisis (GFC). The latest data shows income losses rose to $8.2 billion in 2011, the second largest absolute loss on record…

The housing market meets economist Hyman Minsky’s definition of a Ponzi scheme, as gross rental incomes minus expenses are clearly insufficient to meet principal and interest repayments.7 As 67 per cent of property investors are negatively-geared as of 2011, investment decisions are predicated upon expected rises in land values, not rents. This strategy will inevitably fail, as the escalation in real housing prices can only be sustained by a continual acceleration or exponential rise in mortgage debt.

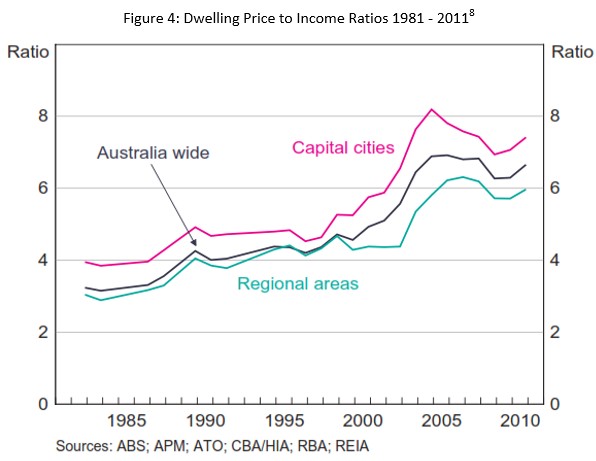

The price to income (P/I) ratio, otherwise known as the median multiple, is another measure of residential property valuation…

From the mid-1990s onwards, housing prices outpaced household incomes, and the P/I ratio increased from 4 to 7 nationwide. It is impossible for household incomes to match the rise in housing prices during the boom phase of a property bubble, as wages grow more slowly, usually just above the rate of inflation…

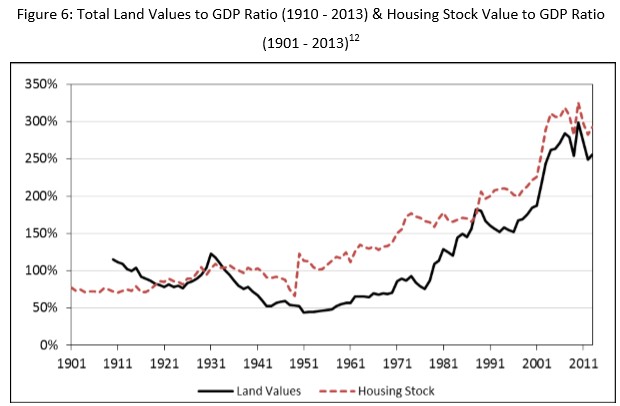

Land is the largest tangible market in Australia… Our housing bubble is actually a residential land bubble, as the total land values to GDP ratio doubled between 1996 and 2010, when it reached a record high of 298 per cent ($4.1 trillion). In real terms, residential land values rose from $895 billion in 1996 to a peak of $3.2 trillion in 2010, a relative increase of 262 per cent. This ratio is closely matched by a similar rise in the value of the residential housing stock. The rise in residential land values, rather than structures, is responsible for almost all of the increase in the value of the housing stock…

Advertisement

Prosper then places the blame for Australia’s expensive housing on convergence of factors, with Australia’s inefficient tax system front-and-centre:

A convergence of factors are responsible: a large cohort of irrational investors gambling on housing prices, a FIRE sector willing and able to facilitate a credit boom, and low property and land taxes attracting speculators to this asset class…

A positive feedback loop has emerged between housing prices and mortgage debt, with rising prices prompting the take-up of more debt in an upwards spiral…

An inefficient taxation system, comprised of low property and land taxes, allows landowners to expropriate ‘geo-rent’ (economic rent derived from land) by capturing the uplift in land values generated by taxpayer-funded infrastructure and rising economic productivity… Government willingness to tax wages and business ahead of land has elevated its privileged status, resulting in larger capital sums being paid by owner-occupiers and investors.

It also advocates land tax reform, which it claims would significantly improve incomes, affordability, and productivity:

Advertisement

Counter-intuitively, reducing wage and business taxation and increasing land tax would not necessarily lower fundamental land prices, given the offsetting boost to disposable wages, profits and hence rents, but it would certainly lower bubble-inflated land prices. Land tax reform – urged on government by every independent tax review in living memory – would firmly correct the price to rent and income ratios. If Australia wishes to escape or ameliorate the profound financial destruction of a bursting land bubble, the solution lies in this equation…

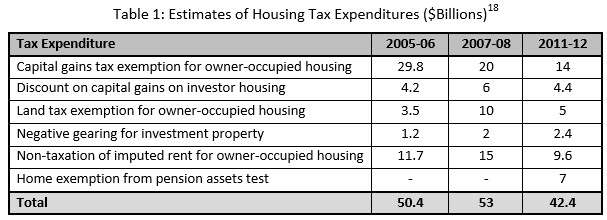

Prosper also slams housing-related tax expenditures, which undermine the integrity of the tax system:

The generous scope of tax expenditures relating to the housing market has served to further increase prices. Tax expenditures are defined as a deviation from the commonly accepted tax structure, whether it is a tax exemption, concession, deduction, preferential rate, allowance, rebate, offset, credit or deferral. Australia has the highest rate of tax expenditures among our OECD peers, at more than 8 per cent of GDP.20 Tax expenditures are vulnerable to lobbying, and often compromise the fairness and efficiency of the tax system. Lavish tax expenditures for both owner-occupied and investment property has significantly worsened housing affordability because they allow landowners to capture greater amounts of geo-rent and prioritise unearned wealth and income over what is earned. Existing home owners capture the most benefit, ahead of first home buyers, investors and tenants.

These tax expenditures provide a strong incentive to speculate on housing prices, and are reinforced by already low property taxes. Investors perceive rental income as secondary to expected rises in capital prices, while first home buyers over-leverage themselves to enter a bubble-inflated market…

Tax expenditures, combined with the ongoing deregulation of the banking and financial system, has transformed the housing market into a casino. Residential property is commonly viewed as a speculative asset to flip, rather than shelter to raise a family in…

Advertisement

Finally, Prosper provides two recommendations to the Senate Inquiry:

Recommendation 1: Reform Land Value Tax. The ideal tool to moderate land bubbles and properly fund infrastructure already exists in the hands of state and territory governments: state land tax (SLT). Unfortunately, this tax has been so riddled with exemptions and concessional treatments it must be considered dormant…

We suggest the current government introduce a nationwide one per cent federal land tax (FLT) – fully rebatable on SLT paid – to oblige the states and territories to use their taxing powers properly. State governments could adjust their tax rules and keep every dollar the FLT raises, to the benefit of all Australians. The Commonwealth Parliament would be entitled to argue this intervention is for sound economic reasons and dissipate the political fallout. Placing state and territory finances on sound bases would vastly improve the federal system mandated by Australia’s Constitution. Transitional arrangements would need to be considered. Rebating all stamp duty paid against a hypothetical past SLT obligation would address concerns of fairness and equity…

Recommendation 2: Macroprudential Regulation. A range of macro-prudential tools are needed to moderate housing price inflation and subdue credit growth in a pro-cyclical financial system, such as those affecting the loan to value, (LVR), debt servicing (DSR) and debt servicing to income (DSTI) ratios.26 Quantitative restrictions should be placed on the share of new mortgages with moderately high LVRs…

To reduce systemic risk, a large rise in capital and liquidity ratios (buffers) is required to ensure banks can withstand a future economic downturn, bank run or large fall in the value of collateral. Research suggests the probability of a banking crisis can be reduced to a 1 in 100 year event by raising core equity (Tier 1) capital ratios to 11 per cent in isolation or raising core equity to 10 per cent with an addition rise in liquid assets of 12.5 per cent (the rise in liquid assets over total assets). For the Big Four banks, this would represent a rise of around 3 per cent in core equity…

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.