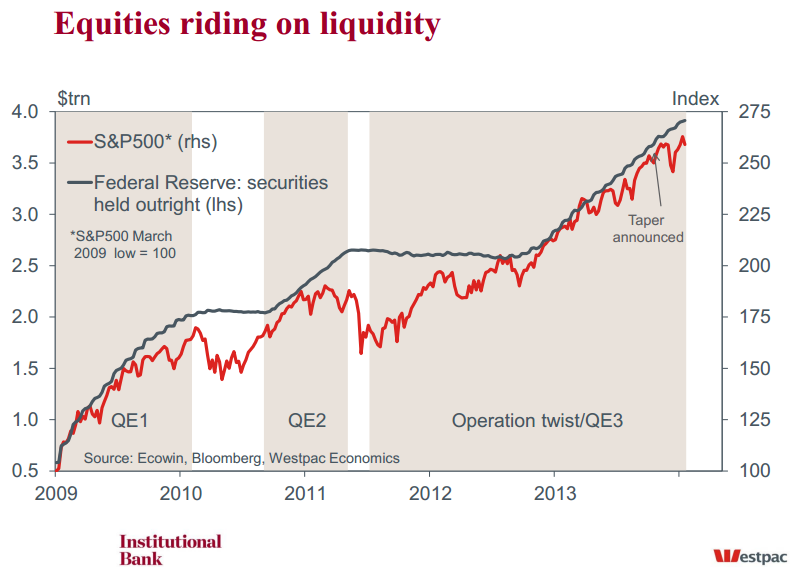

Find below Westpac’s Elliot Clarke on the prospects of taper next. Check out the chart, which never ceases to amaze not to mention terrify!

Next week’s big event will undoubtedly be the 18–19 March FOMC meeting. Since the January meeting: Q4 GDP has been revised down; inflation has remained soft; employment has disappointed; the housing market has continued to weaken; and the ISMs and NFIB business surveys have fallen sharply. All told, economic conditions have been much more in line with our own expectations than those of the FOMC.

Despite this being the case, the FOMC will almost certainly stand its ground in March, reducing the pace of asset purchases by another $10bn, while remaining optimistic about the outlook for growth in 2014 and 2015. Said decision will be due to expectations that better weather will beget much more favourable data outcomes as well as the FOMC’s position that tapering has a neutral impact on real activity.

One of the crucial details to investigate in the wake of the March meeting will therefore be any changes to the FOMC’s published forecasts. We doubt they will be material. Yes recent data has raised doubts over economic momentum, but the weather is an easy scapegoat and we are less than three months into the year. Even if sub-trend growth persists in the months to come, there is no guarantee that the FOMC will respond with a pause. The January minutes made clear that ‘tapering the taper’ would only be appropriate “if the economy deviated substantially from its expected path”. What this means is not exactly clear, but arguably it means we are more likely to see more accommodative qualitative forward guidance around the 6.5% unemployment rate threshold than a near-term pause. (Note, it is important to recognise that, in contrast to their position on tapering, the FOMC believe changes to their forward guidance have a real impact on the economy.)

The tone of the narrative offered in the decision statement and subsequent remarks by Chair Yellen will also be worthy of assessment, particularly for inflation, financial conditions, investment, and jobs.

Starting with inflation, two months ago, FOMC participants noted that while “Inflation remained below the Committee’s longer-run objective”, “transitory factors that had been dampening inflation [are] likely to recede”. The implication was that there was no need to be concerned about disinflation let alone deflation. On this point, we concur. Ever-present price rises for non-discretionary consumption categories such as health care and shelter will continue to offset non-durables disflation and durables deflation, keeping PCE inflation circa 1–1.5% annualised.

Financial conditions have oft been talked about by the FOMC, principally as a support for consumption. This will remain the case in March. Equity markets remain near historic highs and, while house price growth has lost momentum, we have not seen a consolidation of 2012 and 2013’s strong gains. Our own concerns over affordability for the average owner occupier are not shared by the FOMC; rather, participants are (justifiably) focused on the implications of a pullback in investor demand which, as noted last week, is becoming evident.

The final point to consider for financial conditions is the level of term interest rates. Here the FOMC has received a free pass during the tapering episode. A combination of FOMC forward guidance, subsequent soft economic data, and recent geopolitical tensions have kept a lid on US 10yr Treasury yields and related market rates. This will allow the FOMC to maintain its view that tapering is neutral for policy and that forward guidance is effective.

In terms of investment, we will be watching for any discussion of housing investment momentum sans the weather. But of more interest will be discussions around business investment. In the January minutes, FOMC participants alluded to an expectation that “the business sector was willing to increase spending on capital projects”. Since then, momentum in core capital goods data has remained modest and, of late, we have seen a sharp deterioration in key business surveys. An absence of momentum in fixed asset investment should be concerning for the FOMC at any time, but all the more so when inventories are expected to moderate from an “unusually high level”.

On employment, the current three-month pace of nonfarm payrolls is a decidedly underwhelming 129k. Revisions tend to the upside and the weather can be blamed to a degree, but it is still a material step down from the 193k three-month pace at the time of the December taper decision – later revised up to 225k. Further, the household survey’s 42k February job gain indicates January’s 638k surge was more noise than a sign of stronger employment growth. The communications following the meeting will therefore be a test of the FOMC’s ‘cumulative improvement’ benchmark. If literally true, then only no jobs growth or job declines in coming months would see a pause in the tapering process. Needless to say, being comfortable with soft jobs growth could prove quite dangerous given the US’ structural concerns and dependence on household demand.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.