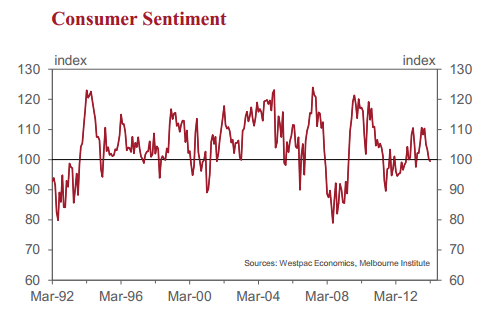

It’ll be no great surprise to anyone not dug into a bullish bunker but consumer sentiment has sagged again in March. From Westpac:

The Westpac Melbourne Institute Index of Consumer Sentiment declined by 0.7% in March from 100.2 in February to 99.5 in March.

The Index has now fallen 10.9% from its November peak of 110.3 and is at its lowest level since May last year. The initial declines in December-January looked to be mainly the unwinding of the election-related sentiment boost. More recent falls though have had a very clear theme centring on a sharp loss of confidence in the economic outlook and escalating job-loss fears.

The run of ‘bad news’ around the motor vehicle industry, other manufacturers and Qantas has clearly rattled consumers. Additional questions surveyed this month on news recall found over two thirds of consumers heard news on ‘economic conditions’ with most viewing the news as negative. Within this broad topic, 37% recalling news specifically about ‘business profitability’ – the highest level of recall since the Global Financial Crisis in 2008 and, prior to that, since the sharemarket crash in 1987. Consumers also had a very high recall rate for ‘employment’-related news with 45% reporting items on this topic, the highest reading since we began running these questions in 1976.

The survey detail reflects these concerns. The March survey showed a continued collapse in near term expectations for the economy – the sub-index tracking consumer views on outlook for “economic conditions over the next 12 months” dropped 4.0%, following a 7.1% fall in February. The sub-index is at its lowest level since December 2011, at the height of the European sovereign debt crisis.

In contrast, other components of sentiment were more mixed in March. The sub-index tracking views on the ‘economic outlook over the next 5 years’ rose 4%, reversing much of last month’s 4.6% decline but still down 12.2% from its November level. The sub-index tracking views on “family finances compared to a year ago” edged up slightly (0.3%), as but those tracking forward views on family finances and ‘time to buy major household item’ slipped 2.3% and 1% respectively.

It should also be noted that the forward view on family finances and ‘time to buy a major item’ have been resilient throughout the decline since November suggesting that while people are more concerned about the economy and jobs, so far these concerns are not seen to be directly impacting their own finances. It may be being viewed more as a risk than an expectation.

The degree of concern around jobs is very high. The Westpac-Melbourne Institute Index of Unemployment Expectations rose by 5.5% to be 13.6% above its November level. At 164.4, the Index is at an extreme high only eclipsed by readings during 2008-09 and the recessions in the early 1990s and early 1980s. Higher readings indicate more consumers expect unemployment to rise in the year ahead. The surge in the Index reflects a severe loss of confidence around job security that can be expected to impact consumers’ financial decisions.

The March survey also included additional questions on the ‘wisest place for savings’. Responses show a shift back towards ‘risk aversion’ with 15% nominating ‘pay down debt’ in March compared to 11% in December. That is still well below the consistent 20-25% readings on this option between 2008 and 2012. The proportions favouring ‘bank deposits’ (29.7%) and ‘real estate’ (26.5%) were largely unchanged from December although there was a sharp decline in the proportion favouring ‘shares’ (7.4% down from 11.6%). The mix suggests some renewed consumer caution but not a return to the levels seen early last year.

While housing may still be finding some favour as an investment option, consumers reported a sharp drop in assessments of whether now is a ‘good time to buy a dwelling’ amidst waning expectations for house prices. The ‘time to buy a dwelling’ Index dropped 6.7% in March and is now down 16.8% from its September high. The sharp drop has taken the Index below its long run average for the first time since August last year. This likely reflects deteriorating affordability due to higher prices and a shift in expectations for interest rates (our February survey showed most consumers now expect mortgage interest rates to rise over the next 12 months). The Westpac-Melbourne Institute House Price Expectations Index has been more resilient, but it also fell by 2.7% to be 6.8% below its December high. At 155.1 though the Index level is still in strongly positive territory implying most consumers expect prices to continue rising over the next year.

The Reserve Bank Board next meets on April 1. The RBA is clearly firmly on hold awaiting more information, around the inflation picture in particular. We retain our view that rates will remain unchanged over the first half of 2014, but with two further 25bp rate cuts in the second half. The ongoing downturn in mining; fiscal consolidation; a stubbornly high currency amidst a fall in the terms of trade combine with two important macro dynamics the Bank is presently choosing to understate: the feedback on confidence and incomes from continued labour market weakness and ongoing caution amongst business and consumers. Today’s consumer sentiment release and recent updates on business confidence and conditions suggest this feedback is still operating and has intensified since late last year.

Kick-arse recovery, this one! Dollar sank too to the low of the day approaching 89.50.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.