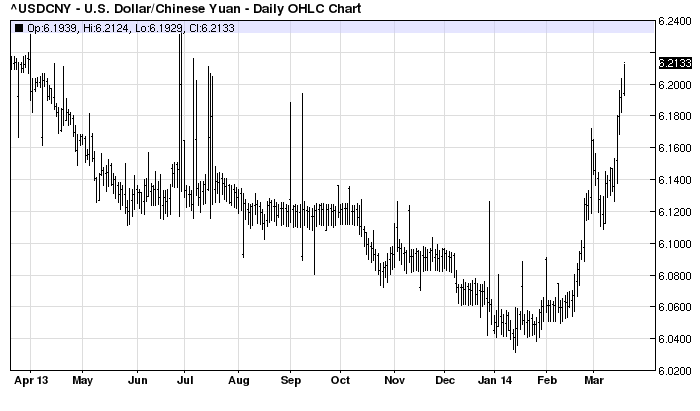

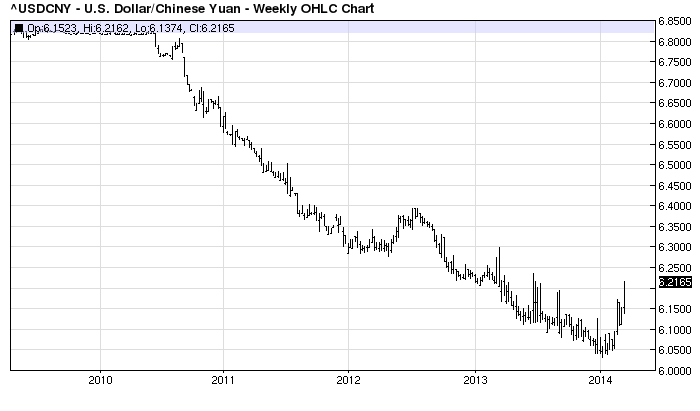

The Chinese yuan has spiked again within in its new 2% fixing band, and how:

A year’s worth of depreciation now gone. Over the longer term the move is taking on material dimensions:

Remember that the 6.20 levels is seen as a tipping point for more selling. From Goldman’s report on the commodity scam unwind yesterday:

An increasing range of commodities are being used to raise foreign financing, which now includes iron ore, soybeans, palm oil, rubber, zinc, and aluminum, as well as gold, copper, and nickel. CCFDs create excess physical demand and tighten the physical markets artificially; in contrast, an unwind creates excess supply and thus is bearish to prices. We think CCFDs will be unwound over the medium term, mainly triggered by an increase in Chinese FX volatility, as indicated by recent CNY depreciation and PBOC’s latest move to widen the daily trading band. FX volatility could result in a higher cost of currency hedging, effectively closing the interest rate arbitrage. Higher US rates are another likely catalyst for an unwind in the long run. A continuous CNY depreciation in the short term, however, would trigger some deals to be unwound sooner than expected, and hence place downside risks to our short-term commodity price forecasts.

It should now become apparent why the ongoing sharp devaluation of the CNY, far more than merely impacting a few massively levered speculators, and recall that the European Knock In point of maximum vega is about USDCNY 6.20 as discussed previously, will have a far more broad hit to asset levels not just in China but across the world if and when the inevitable moment of CCFD unwind finally begins, and in a reflexive fashion, initial selling begets more selling, more CNY devaluation, greater margin calls, further CCFD unwinds, and so on, until finally the PBOC has no choice but to come in and bail out the financial system one more time.

On top of that, this level of volatility will deter other forms of carry trade that support Chinese credit creation, via any number of informal channels that get around capital controls, seeking to benefit from the interest rate differential and an appreciating yuan.

This is more reason to think that the Chinese are quite serious about their reform agenda.