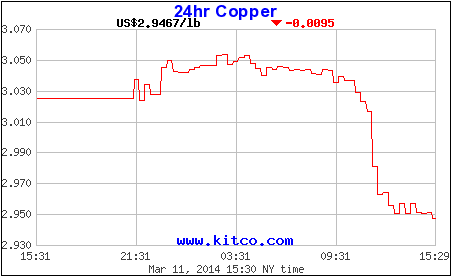

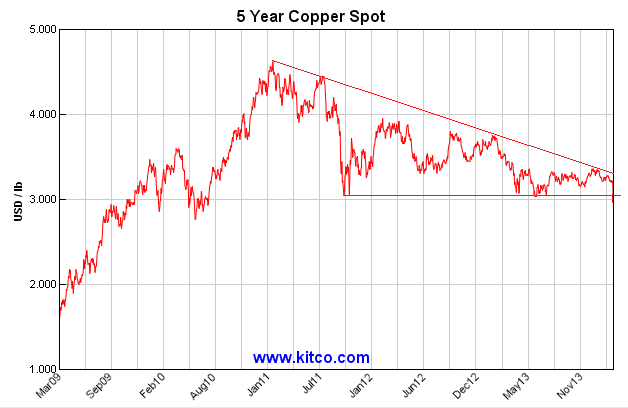

Copper broke through its three year support line last night falling 2.5%:

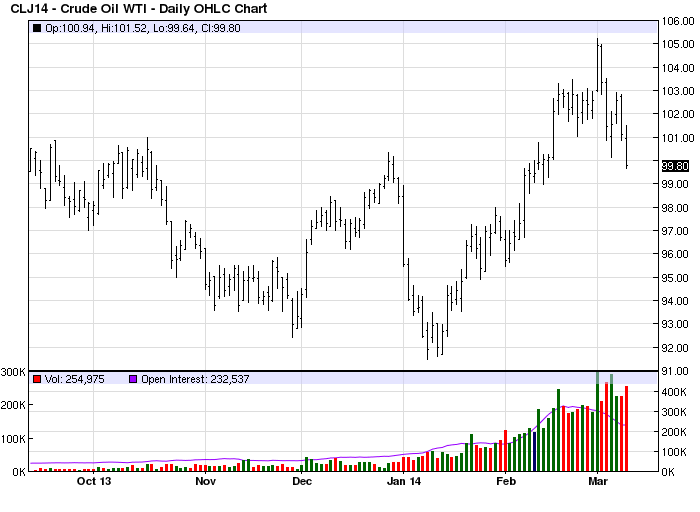

Oil is also looking toppy down, 1.3% on the night:

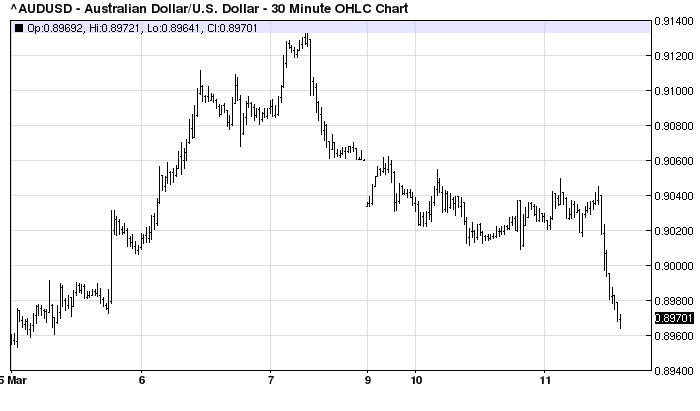

In an absence of substantial data in the US, that was enough to spook markets about Chinese growth prospects. The S&P500 fell half of one percent and bonds were bid with yields down roughly the same. The risk-off mood lifted gold a little too and smacked the Australian dollar firmly below 90 cents:

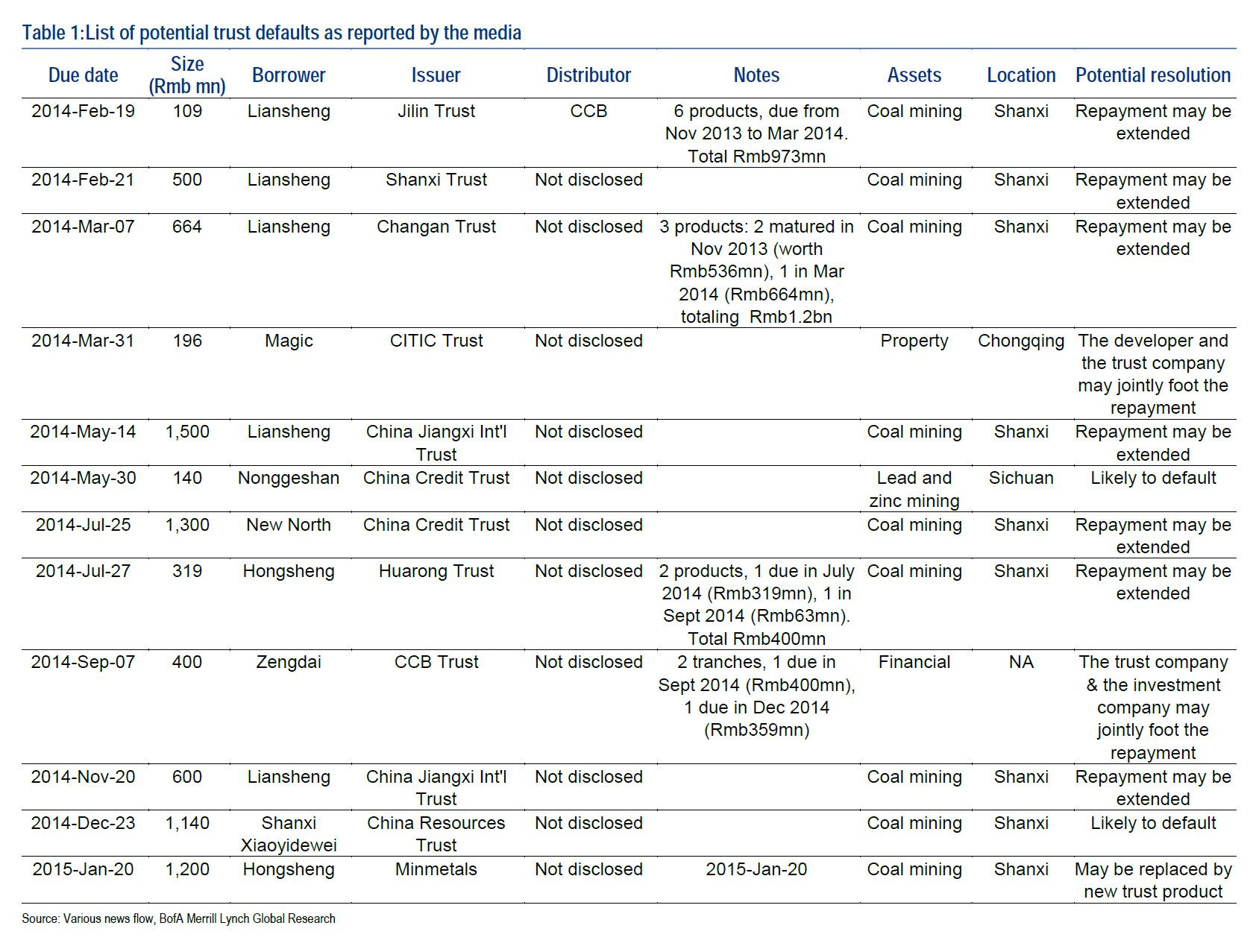

As I said yesterday, so long as commodities and Chinese growth remain an open question, the drivers of Australian dollar value point down. And that looks set to continue with a pipeline of potential defaults marching our way. In the trust market, From BofAML:

And in corporate bonds as well where it’s not at all clear who will get bailed and who won’t. From J Capital via FTAlphaville:

For well-connected companies, government is deeply intertwined with business operations, managing prices, mandating production volumes, buying and warehousing output for which there is no real market, promoting specific technologies, directing bank lending and otherwise investing in company equity and debt, manipulating collateral values, colluding to defraud public investors, providing subsidies to makers and consumers, and intervening more directly with the banks and new varieties of equity investment funds, both before any crisis becomes evident and, quietly and obscurely, at the last minute, as witnessed in Credit Equals Gold #1.

That is why a default or near default is significant not as “China’s Bear Stearns moment” but as a sort of spoor that indicates how badly an industry is wounded. The initial default of Chaori does not mean that the government will end the backstop, but it does mean that China’s solar industry has no more resources to spread around.

And then there is this from Lombard Street:

The term ‘bond market’ conjures up the cut and thrust of a developed economy, but in the Chinese context it means something very different. The market is distorted and fails to price risk appropriately. To start with, the authorities determine the risk-free cost of capital in the government bond market. Bond prices in the primary market, set below the clearing level of supply and demand, are priced off the regulated one-year deposit rate. State-owned banks own the bulk of government debt and typically hold the bonds to maturity. Secondary trading is very thin as the underwriters have no incentive to sell the debt. Banks are guaranteed a return, while the government can use them as ATMs to bankroll its fiscal expansion without having to worry about its credibility, as it would in a truly contested market.

That is the game that is about to end with credit tightening and eventually interest rate liberalisation as well and it doesn’t take Einstein to figure out there will be many losers. Also from BofAML about CITIC’s “Magic” trust, the next default candidate on its list:

Details: invested in an office building in Chongqing. The Chongqing developer ran into financial problems in mid-2013. CITIC Trust tried to auction the collateral but failed to do so because the developer has sold the collateral and also mortgaged it to a few other lenders.

Now that’s some ponzi lending. China reform pressures are the new normal.