The Friday default of a tiny corporate bond in China appears to have triggered larger ripples for commodity markets. From the FT:

Copper for delivery in three months on the London Metal Exchange fell by as much as 3.7 per cent to $6,785 a tonne. Other base metals were also under pressure. Three-month nickel, which hit a nine-month high earlier in the week, dropped 1.5 per cent to $15,242 a tonne, while zinc lost 2.5 per cent to $2,056 a tonne and aluminium fell 1.7 per cent to $1,765.

“China’s authorities could decide to let some of these trusts default, which may destabilise the shadow banking sector. In the worst case, this could lead to a credit crunch, further damping China’s commercial copper demand and that may not be offset by a potential rise of copper shipments for financing purposes,” Michael Widmer, metals strategist at Bank of America Merrill Lynch, wrote in a report this week.

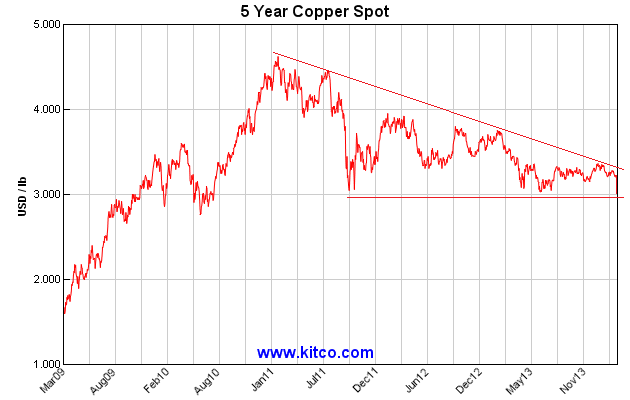

Here is the chart:

At 3.09 $US per pound, copper is sitting right on a three year support level in an ugly descending triangle pattern that looks like breaking.

The jury is out on whether this is fears about economic growth or a seizure in the copper financing arbitrage complex. It’s probably both. Let’s recall the scam:

Advertisement

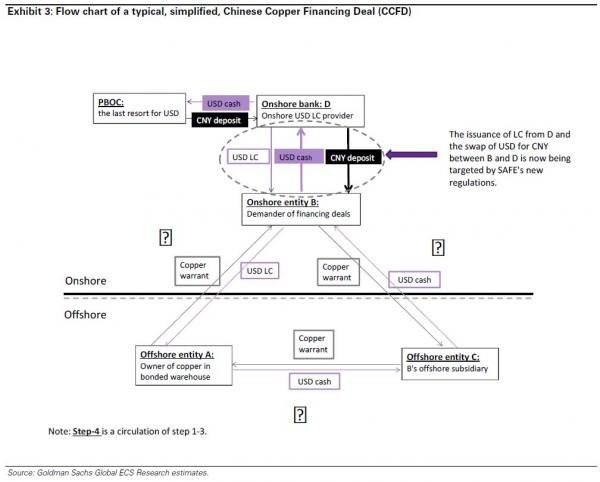

An example of a typical, simplified, CCFD

In this section we present an example of how a typical Chinese Copper Financing Deal (CCFD) works, and then discuss how the various parties involved are affected if the deals are forced to unwind. Exhibit 3 is a ‘simplified’ example of a CCFD, including specific reference to how the process places upward pressure on the RMB/USD. We believe this is the predominant structure of CCFDs, with other forms of Chinese copper financing deals much less profitable and likely only a small proportion of total deal volumes.

A typical CCFD involves 4 parties and 4 steps:

Party A – Typically an offshore trading house

Party B – Typically an onshore trading house, consumers

Party C – Typically offshore subsidiary of B

Party D – Onshore or offshore banks registered onshore serving B as a client

Step 1) offshore trader A sells warrant of bonded copper (copper in China’s bonded warehouse that is exempted from VAT payment before customs declaration) or inbound copper (i.e. copper on ship in transit to bonded) to onshore party B at price X (i.e. B imports copper from A), and A is paid USD LC, issued by onshore bank D. The LC issuance is a key step that SAFE’s new policies target.

Step 2) onshore entity B sells and re-exports the copper by sending the warrant documentation (not the physical copper which stays in bonded warehouse ‘offshore’) to the offshore subsidiary C (N.B. B owns C), and C pays B USD or CNH cash (CNH = offshore CNY). Using the cash from C, B gets bank D to convert the USD or CNH into onshore CNY, and trader B can then use CNY as it sees fit.

The conversion of the USD or CNH into onshore CNY is another key step that SAFE’s new policies target. This conversion was previously allowed by SAFE because it was expected that the re-export process was a trade-related activity through China’s current account. Now that it has become apparent that CCFDs and other similar deals do not involve actual shipments of physical material, SAFE appears to be moving to halt them.

Step 3) Offshore subsidiary C sells the warrant back to A (again, no move in physical copper which stays in bonded warehouse ‘offshore’), and A pays C USD or CNH cash with a price of X minus $10-20/t, i.e. a discount to the price sold by A to B in Step 1.

Step 4) Repeat Step 1-Step 3 as many times as possible, during the period of LC (usually 6 months, with range of 3-12 months). This could be 10-30 times over the course of the 6 month LC, with the limitation being the amount of time it takes to clear the paperwork. In this way, the total notional LCs issued over a particular tonne of bonded or inbound copper over the course of a year would be 10-30 times the value of the physical copper involved, depending on the LC duration.

Copper ownership and hedging: Through the whole process each tonne of copper involved in CCFDs is hedged by selling futures on LME futures curve (deals typically involve a long physical position and short futures position over the life of the CCFDs, unless the owner of the copper wants to speculate on the price).

Though typically owned and hedged by Party A, the hedger can be Party A, B, C and D, depending on the ownership of the copper warrant.

Very similar scams operate in iron ore and are thought to be behind recent sky-rocketing port inventories as credit was squeezed. So, how is the steel sector holding up? Back to the FT:

“The Chinese steel industry is in total disarray today, following rumours surfacing of the first debt defaulting mill (3.6m tonnes per annum) from Shanxi province shutting 5-6 furnaces,” commented Melinda Moore, analyst at Standard Bank. “Rumours then spiralled that banks are seeking to call in 20 per cent of loans to some [private] steel industry participants.”

“Potentially these rumours are actually one and the same, in which case it’s an isolated instance. Nonetheless iron ore [futures] and coking coal on the Dalian Exchange both gapped down to their full 4 per cent daily trading lower limits,” she added. “And this panic could potentially reverberate further; firstly into another destock across both physical steels and iron ore . . . but also beyond, into other commodities and other sectors more generally.”

Advertisement

I noted last week that authorities’ drive to close 27 million tonnes of steel mills capacity this year – in the name of addressing pollution – was a tiny figure in the scheme of things. Here we may here have an insight into why. Until stimulus is renewed, production is going to get knocked by economic factors far more quickly than than regulators can shut them down

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.