Morgan Stanley has an argument today that I can’t swallow:

Can Australia cycle from engineering to resi and non-resi?

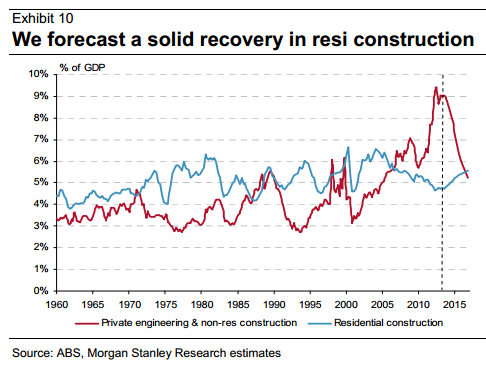

In Exhibit 8, we see why the engineering boom has dominated the focus of the market and policymakers over the past five years. Reaching a peak of almost 7% of GDP, private engineering has crowded out activity across the housing, non-resi and public engineering sectors.

However, with the housing market responding strongly (both in terms of prices and lead activity indicators) to the RBA’s 225bps in rate cuts over the past 27 months, our base case has been optimistic that Australia can transition to an East Coast Recovery (see 2014 Outlook: Go East, 16 Dec 2013).

Residential building approvals have picked up strongly through 2013, with a surge in apartment approvals taking the 3-month annualised rate almost to historical peaks. While this has not yet shown up in activity levels, we see conditions picking up in 2014 as approvals become starts.

Interestingly, we have also seen signs of improvement in non-residential building approvals. While the data can be choppy, it does reconcile with stronger feedback on the ground, including anecdotes in the 1H14 reporting season from BSL and BLD that non-resi volumes had improved.

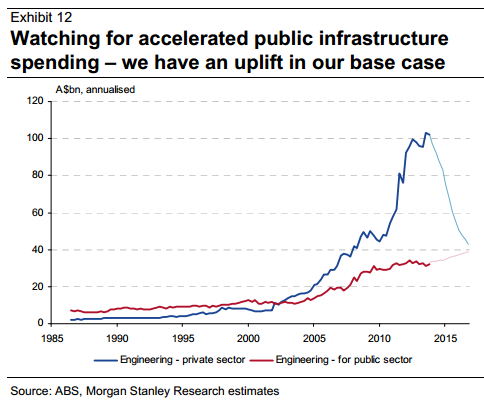

Waiting for confirmation of public infrastructure stimulus

Finally, we remain optimistic about the potential for a public infrastructure program to be announced in the lead up to the May Budget. The capex data this week follow closely on the G20 meeting of Finance Ministers and Central Bank Governors last weekend, where the Australian government made infrastructure a point of focus, whilst also convincing our counterparts to develop individual growth strategies to deliver

a collective additional 2% of GDP over the next five years. While some may view the G20 growth target as a token gesture, we believe the domestic political narrative that the government is creating should not be completely overlooked.

By backing away from the near-term focus on a budget surplus and repeatedly emphasizing the need for ‘productivity -boosting infrastructure’, we think the government is paving the way to pair any expenditure cuts with a boost to public investment, particularly in transport sectors on the East Coast.

The mechanism for any infrastructure spending will involve greater cooperation with the State governments, which are in most cases party-aligned and also keen to boost spending on infrastructure (particularly if it comes at Canberra’s expense).

At the last COAG meeting, the Federal government confirmed that it was willing to offer incentives for a State government privatization program, with the aim of recycling capital into greenfield public infrastructure projects.

While we acknowledge that public construction is modest as a share of GDP (2.8%), such a program could help support business confidence in the demand outlook, and help improve the supply of infrastructure-equipped land to sustain the housing cycle that is getting under way.

Take a close look at those charts and tell me you see hope that both government and residential construction can in any way offset the collapse in mining investment? They are hopelessly, hilariously, out-gunned.

Advertisement

There are other offsets in net exports and consumption (if it can hold together) but let’s not kid ourselves, business investment drives jobs growth and it is blowing an enraged gale into our faces.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.