KPMG’s Bernard Salt claims to have uncovered the key ingredient for measuring housing demand and the trajectory of the housing market: household formation. From The Australian:

There is a single demographic driver that underpins the residential property industry…

The thing that drives demand for houses and units is the rate of household formation…[which]…translates more or less directly into demand for residential property…

Imagine if the property industry had a dataset that measured and monitored the rate of household formation on a city-by-city basis with associated commentary to assess whether this demand was rising or falling? I have set up just such a dataset…

I have measured the net growth in households for each of the 10 largest cities in Australia between the 2006 and 2011 censuses…

The question for the property industry is how demand will shift, is shifting, over the five years to 2016?

The market for residential property has shifted and continues to shift…

To be successful in today’s property market, business more than ever needs to respond to what used to be known as the vagaries of the market but which in reality is the shifting and the shuffling in the key demographic driver of household formation.

Can household formation can be accurately forecast?

Estimates of household formation typically attempt to quantify what the demand for housing might be given the growth in population, trends in household size, demand for second (or holiday) homes, and economic conditions (e.g. employment, interest rates, etc). Like all modelling, it is fraught with danger.

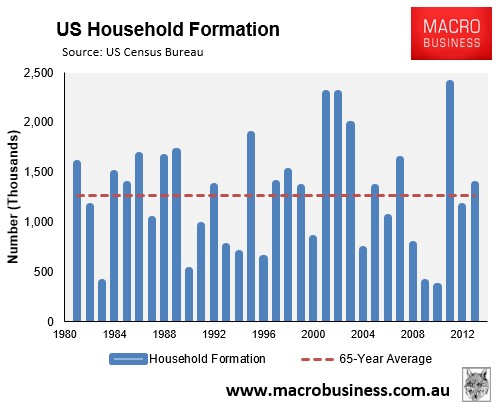

In the lead-up to the US housing bust, underlying demand was running strong. Unemployment was low, the US economy was motoring along, credit was readily available, and household formation was running well above the long-run for most of this period (see next chart).

The surge in household formations through most of this period led to numerous suggestions that the US was facing a housing shortgage, especially in areas where strict land-use regulations were in effect, such as California.

The rest is history. The US housing bubble popped, the economy tanked, and the rate of household formation fell to less than half the long-run average, leaving a vast oversupply of homes, even in supply-restricted markets like coastal California.

The key lesson from the US experience is that household formation is highly changeable depending, largely, on prevailing economic conditions.

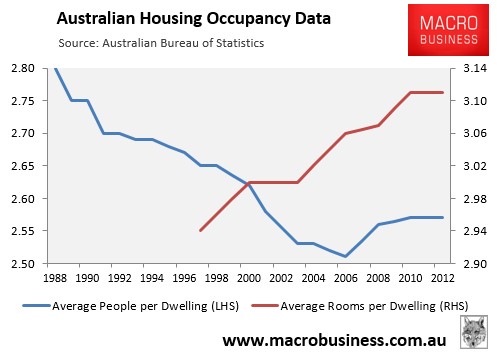

While Australia is in some respects fortunate that it has not experienced the types of over-building experienced in some other nations, it could equally be argued that there is latent capacity (excess bedrooms) in the pre-existing housing stock versus persons per dwelling (see below chart).

Should economic conditions deteriorate significantly, such as via a disorderly unwinding of the mining boom, the number of Australians opting for group accommodation (or the number of young people moving back into mum and dad’s) could rise significantly, smashing the rate of household formation and potentially turning a housing shortage into a short-term surplus.

unconventionaleconomist@hotmail.com