UBS today asks if the recovery in industrials in the share market is overdone:

Median Valuation Less Demanding

The Industrial Ex Financial PE at 17x (cap weighted) looks expensive versus history though there are some partial offsets. The current median of 15.7x suggests the high aggregate P/E is partly a result of highly rated larger stocks, though this doesn’t fully negate the overvaluation argument.

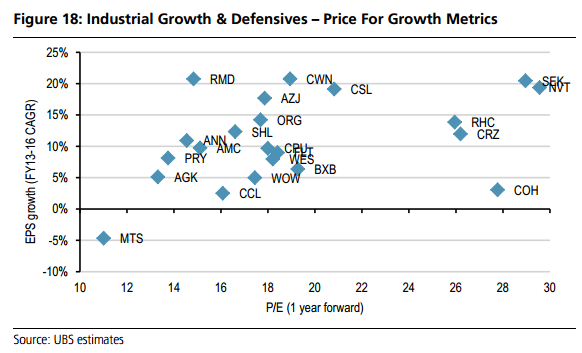

Market Not Clearly Overpaying For Growth

While P/Es appear high it is not clear that there is a generalised overvaluation of “growth”. High P/E stocks are trading only slightly above their average while low P/E stocks are trading well above their average. This is also reflected in a lower than average P/E dispersion.

Market Is Paying Up For Cyclical Recovery

Perhaps linked to the lack of low PE stocks is that the other clear tendency in the market is that the market appears to be pricing in a cyclical recovery. This seems plausible though cyclicals (based on our top 100 universe) appear notionally expensive by historical standards. For cyclicals it is likely to come down to who delivers the earnings. Investors are advised to also consider some small cap cyclicals or non-bank financial cyclicals.

In short, it’s actually low growth stocks that are over-valued relative to history, owing to financial repression. One must always pay for growth and this cycle is little different.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.