More atrocious US data on Friday night. This time industrial production:

Industrial production decreased 0.3 percent in January after having risen 0.3 percent in December. In January, manufacturing output fell 0.8 percent, partly because of the severe weather that curtailed production in some regions of the country

…The severe weather in January contributed to a decrease of 0.8 percent for manufacturing production. Output had risen in each of the previous five months, though the rates of increase for October through December are now reported to be slower than previously stated: Steel, semiconductors, motor vehicles, and organic chemicals made the largest contributions to the downward revision for the fourth quarter. The level of factory output in January was 1.3 percent above its year-earlier level.

Capacity utilization for manufacturing moved down 0.7 percentage point in January to 76.0 percent, a rate 2.7 percentage points below its long-run average.

Nasty. A few points. The downward revisions to past months show that this deceleration is not all weather related but it is important to note that the Fed thinks it’s a significant cause so will probably “look through” it for a while. Such events offer quick snap backs but because US inventories are so full right now (which is why growth was so strong late last year) the bounce is unlikely to be spectacular.

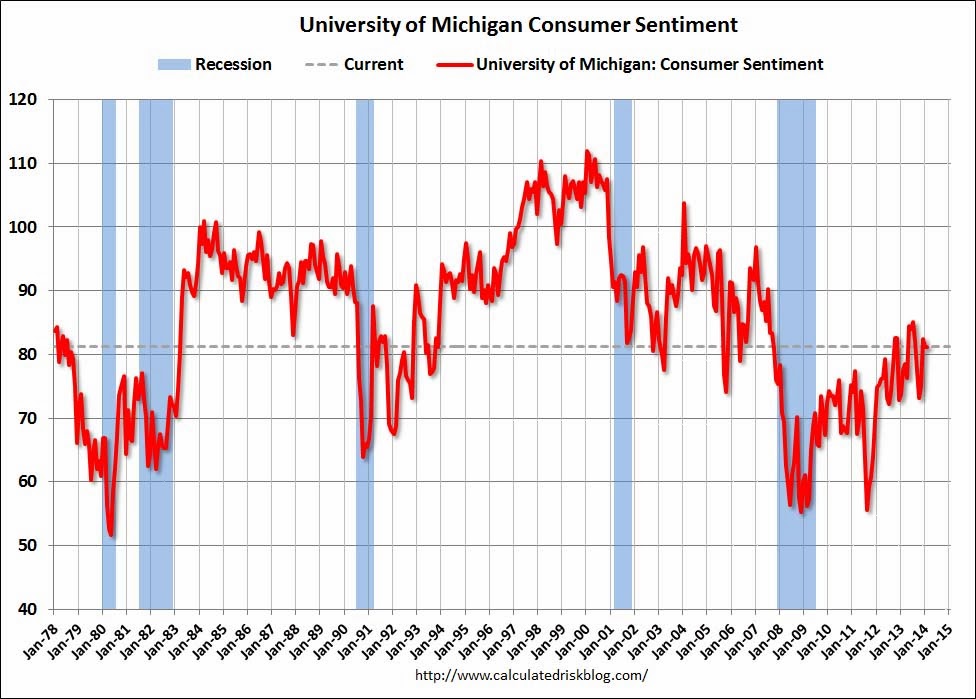

In better news, preliminary consumer confidence came in firm and unchanged at 81.2 points suggesting weather may also have played a material role in last week’s awful January retail number. From Calculated Risk:

Weather the economy will slow enough to prevent the conclusion of tapering is now a real question. That’s certainly what gold, forex and stocks are telling us. The latter piled on the better part of one percent and at 1840 we’re just one good day short of the record high at 1850.

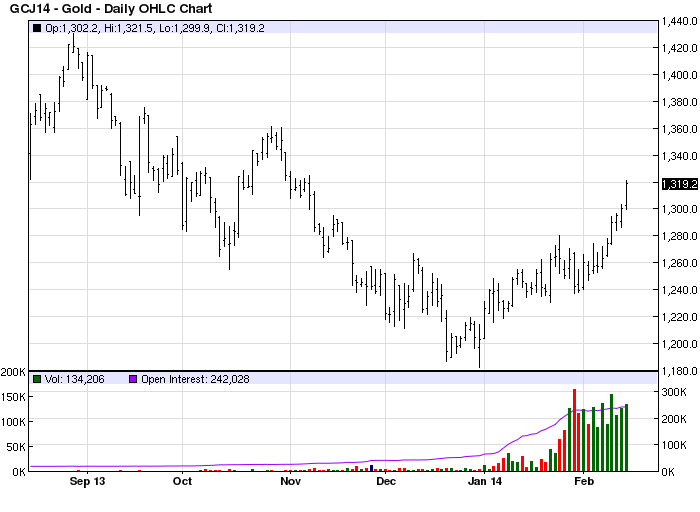

Gold added one percent and is running in clear air:

The Aussie is hovering at 90.4 cents and was up significantly against everyone except yestermonth’s EM dogs turned today’s super-currencies:

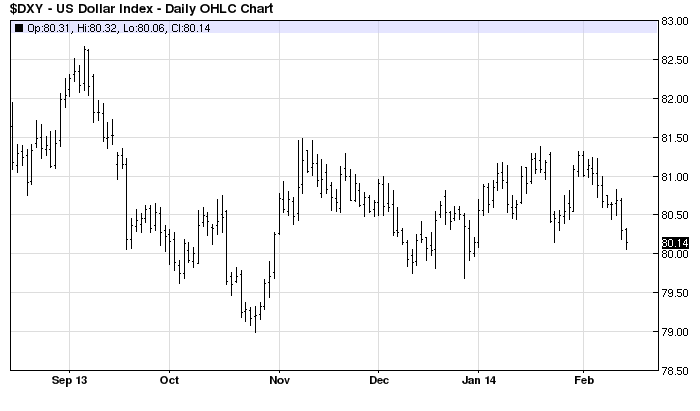

The US dollar also fell 0.2%:

That broken jawbone at the RBA must really be starting to ache in the cold!

It wasn’t all bad news is good news. Bond markets kept their heads and yields rose a touch at the long end. Any renewed easing is not yet clear to the inflation vigilantes.

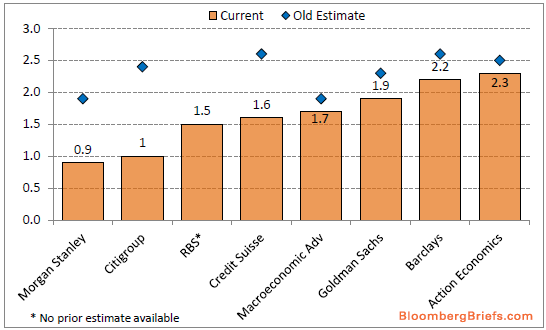

But, growth forecasts are being slashed left right and centre on the sell-side:

And these growth rates are quite consistent with renewed QE.

The sun will shine again shortly and perhaps all will pass like blackened snow in a rotten New York alley, or not. Whatever the weather, that burning oil drum you can see through the gloom is the Yellen “put” still warmly in place. From last week’s Congressional testimony:

“I would agree that one of the channels by which monetary policy works is asset prices, and we have been trying to push down interest rates, particularly longer term interest rates. Those rates do matter to the valuation of all assets, both stocks, houses, and land prices. And so I think it is fair to say that our monetary policy has had an effect of boosting asset prices. We have tried to look carefully at whether or not broad classes of asset prices suggest Bubble-like activity. I’ve not seen that in stocks generally speaking.