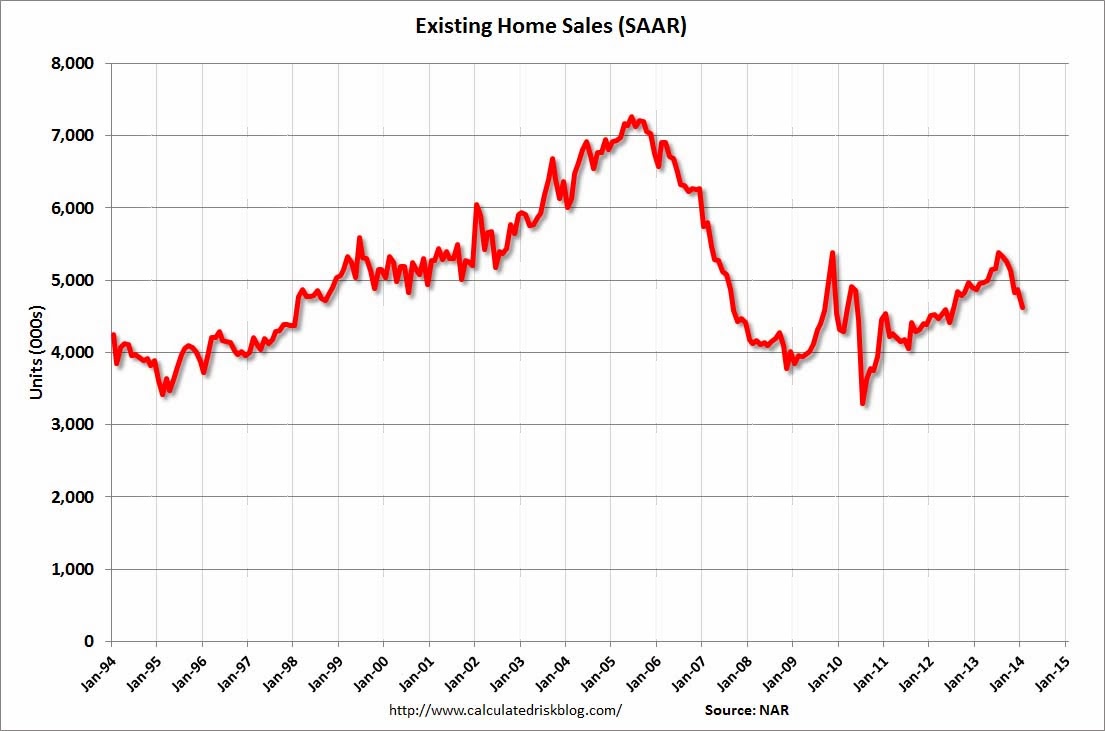

Friday night saw the release of the latest poor US housing data with NAR existing home sales missing big in January (chart from Calculated Risk):

Total existing-home sales, which are completed transactions that include single-family homes, townhomes, condominiums and co-ops, dropped 5.1 percent to a seasonally adjusted annual rate of 4.62 million in January from 4.87 million in December, and are also 5.1 percent below the 4.87 million-unit pace in January 2013. Last month’s level of activity was the slowest since July 2012, when it stood at 4.59 million.

Lawrence Yun, NAR chief economist, said unusual weather is playing a role. “Disruptive and prolonged winter weather patterns across the country are impacting a wide range of economic activity, and housing is no exception,” he said. “Some housing activity will be delayed until spring. At the same time, we can’t ignore the ongoing headwinds of tight credit, limited inventory, higher prices and higher mortgage interest rates. These issues will hinder home sales activity until the positive factors of job growth and new supply from higher housing starts begin to make an impact.”

In short, the housing slowdown is becoming a concern and weather is only partly to blame. The question is how partly?

I already covered the new housing starts data last week, in which there was firm evidence of weather-related slowing but the case for existing homes seems to me far less strong and should largely be accounted for in seasonal adjustment. Snow and cold will slow the search for a home but can’t stop it the way frozen earth can new housing construction.

Advertisement

US housing is largely slowing because of the spike in interest rates. It’s really that straight forward.

So far, house prices have shown momentum but they are going to slow as mortgage applications wane. There is a lot of cash activity in the market that should (barring its exit too) prevent a rout but slowing house prices will weigh on incomes and consumption at the margin.

The more important question is what will happen with new housing given its role in growth and job creation. Capital Economics asks that question in a note today:

Advertisement

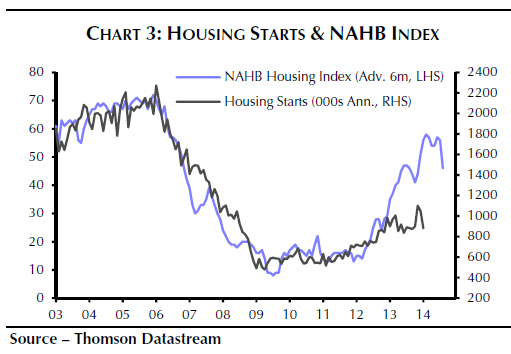

That’s not to say that the bad weather explains all of the fall in January. Some of it is probably a correction after starts were unusually strong at the end of last year. As Chart 3 shows, the level of starts is now just back to where it was last summer. This could mean that there is less scope for starts to bounce back once the bad weather has passed and workers have returned to the construction sites.

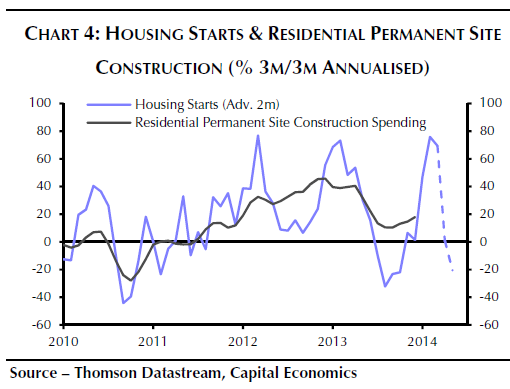

But even if starts did rebound in February and March, residential investment will still fall in the first quarter. As the dotted blue line on Chart 4 shows, a rebound in starts to December’s level wouldn’t prevent the three-month-on-three month annualised growth rate from plunging to -20% from +69%. And if starts don’t rise back, the fall would obviously be larger.

This implies that real residential investment will decline in the first quarter of this year. That would build on the drop in the fourth quarter of last year, which was the first fall in three years. The result is that annualised GDP growth in the first quarter may be between 0.3 and 0.5 percentage points lower than would otherwise have been the case.

As we have pointed out before, however, weather distortions don’t tend to have a lasting impact on the economy for two reasons. First, there are always some offsetting effects, such as more spending on heating. Second, most of any activity postponed by the bad weather just takes place at a later date. (See US Economics Weekly “Economy will avoid a deep freeze”, 13th January.) So the weather won’t extinguish the housing recovery.

In theory, the rise in mortgage rates last summer could. But in practice, while the rise has taken some of the heat out of the housing recovery, we don’t think it will send it into reverse. To start with, 30-year fixed rates have fallen back from August’s peak of 4.8% to 4.5%. Although this hasn’t reversed the entire rise from the trough of 3.5%, mortgage rates remain low by historical standards. On top of that, the steady rise in the loan-to-value ratio of new mortgage lending over the past year suggests that banks are gradually becoming keener to extend credit. (See our US Housing Update “Will mortgage demand recover this year?” sent to clients of our US housing service on 14th February.)

That seems fair to me although I’ll add that mortgage credit has kept falling even as bond rates have eased. The Fed’s taper will have plenty of weakness to “look through” if it is to persist.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.