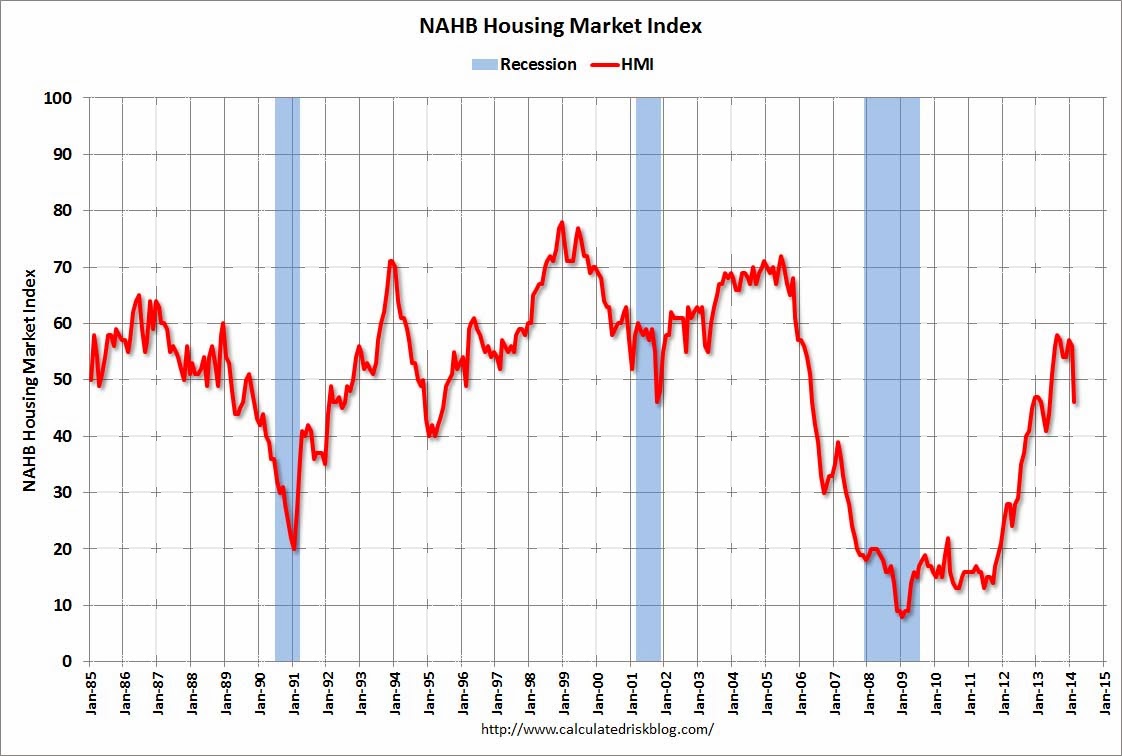

US data is still lousy and now everyone, everywhere is blaming the weather. The NAHB Builder Confidence Index tanked, from Calculated Risk:

Unusually severe weather conditions across much of the nation along with continued concerns over the cost and availability of labor and lots resulted in builder confidence in the market for newly-built, single-family homes to post a 10-point drop to 46 on the National Association of Home Builders/Wells Fargo Housing Market Index (HMI), released today.

“Significant weather conditions across most of the country led to a decline in buyer traffic last month,” said NAHB Chairman Kevin Kelly, a home builder and developer from Wilmington, Del. “Builders also have additional concerns about meeting ongoing and future demand due to a shortage of lots and labor.”

…All three of the major HMI components declined in February. The component gauging current sales conditions fell 11 points to 51, the component gauging sales expectations in the next six months declined six points to 54 and the component measuring buyer traffic dropped nine points to 31.

The February 2014 Empire State Manufacturing Survey indicates that business conditions improved marginally for New York manufacturers. The general business conditions index fell eight points, but remained positive at 4.5. The new orders index fell to about zero, indicating that orders were flat, and the shipments index declined thirteen points to 2.1.

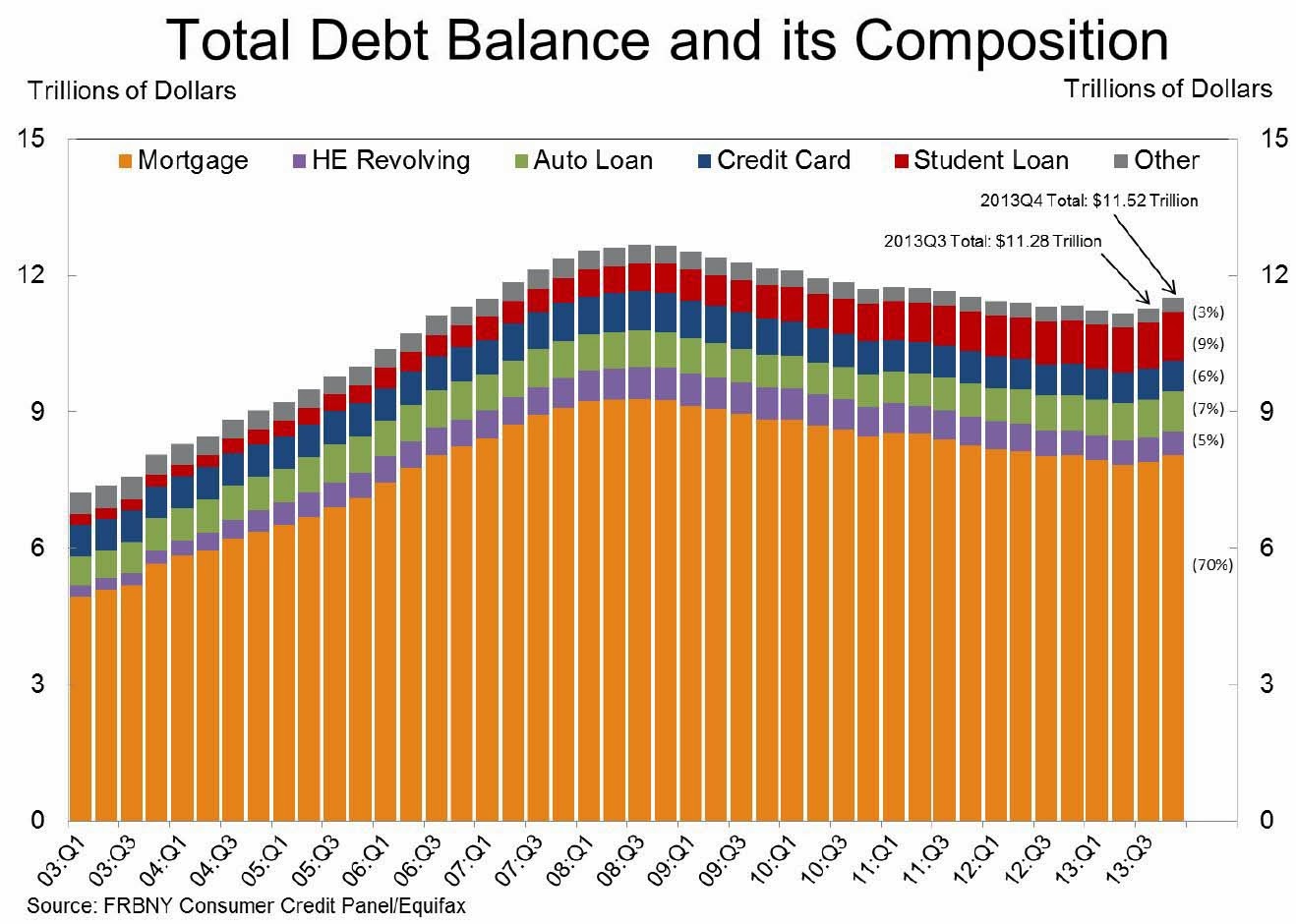

Aggregate consumer debt increased in the fourth quarter by $241 billion, the largest quarter to quarter increase seen since the third quarter of 2007. As of December 31, 2013, total consumer indebtedness was $11.52 trillion, up by 2.1% from its level in the third quarter of 2013. The four quarters ending on December 31, 2013 were the first since late 2008 to register an increase ($180 billion or 1.6%) in total debt outstanding. Nonetheless, overall consumer debt remains 9.1% below its 2008Q3 peak of $12.68 trillion.

Mortgages, the largest component of household debt, increased 1.9% during the fourth quarter of 2013. Mortgage balances shown on consumer credit reports stand at $8.05 trillion, up by $152 billion from their level in the third quarter. Furthermore, calendar year 2013 saw a net increase of $16 billion in mortgage balances, ending the four year streak of year over year declines. Balances on home equity lines of credit (HELOC) dropped by $6 billion (1.1%) and now stand at $529 billion. Non-housing debt balances increased by 3.3%, with gains of $18 billion in auto loan balances, $53 billion in student loan balances, and $11 billion in credit card balances.

It was bond markets that reacted most strongly to the data mix, rallying hard and cutting 2% from the 10 year yield and a bit less from the 30 year. The vigilantes are spooked by taper taper today. Broader markets were more circumspect with stocks stuck on the spot, the US dollar edging lower, gold sitting on yesterday’s losses and the Australian dollar going nowhere.

Advertisement

The weather is clearly complicating matters for all.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.