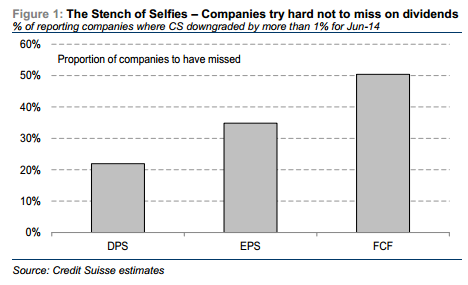

Credit Suisse has a couple of chart about profit season that underline a few points about the vulnerabilities of future growth. The first is that, as I’ve noted before, the misses were all in the top line, profits were better still but dividends were strongest in terms of meeting expectations:

The Stench of Selfie — Companies have tried hard to keep their dividend-hungry investor-base happy. In many cases this is the self-managed super funds who now own more than 16% of the Aussie equity market. For example, only 22% of companies missed on DPS, while 35% missed on EPS but a considerable 50% missed on FCF. We applaud companies attempting to keep their shareholders happy. However, we hope they are not spreading themselves too thinly.

In short there’s not going to be enough capital in the tank to fund growth, which bodes poorly for the economy.

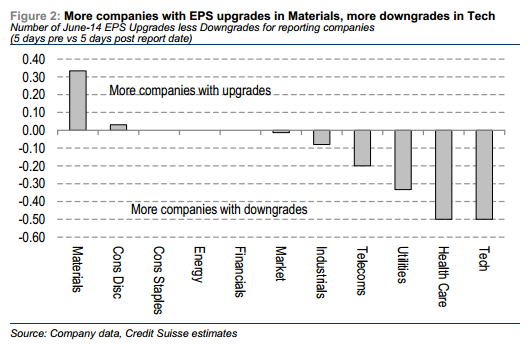

But there is another problem. The EPS out-performance is all in the resource sector:

Advertisement

This has largely been driven by the better forecast earnings of the big iron ore miners. As the iron ore price falls, the market’s expectations of EPS growth is going to get hit hard.

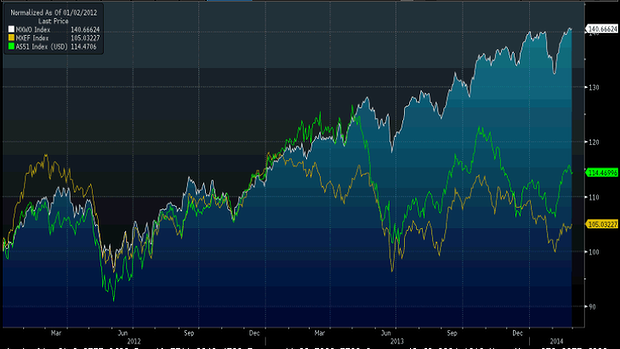

Dividends are great but without FCF and EPS growth why would investors pay a premium for equity risk? They won’t, and that’s why we’re seeing the ASX diverge from other developed economy bourses and track developing economies instead as the following chart from the SMH blog shows:

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.