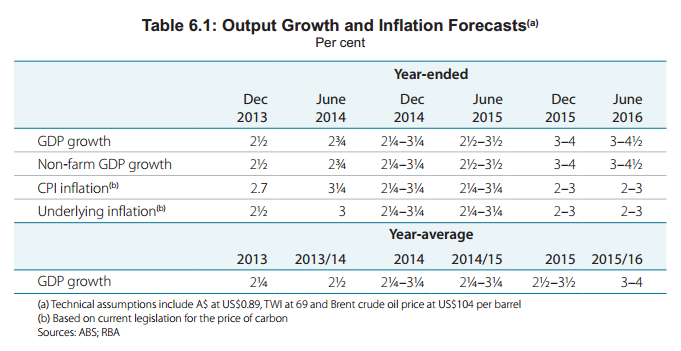

The RBA’s Statement of Monetary Policy is out and had raised growth and inflation forecasts, more for the latter:

The year to June growth is up .25% but inflation is up .75% on November forecast. The year to December gets an extra .25% for both as well and 2015 narrows the forecast for growth to 3-4% from 2.75% to 4.25%. Inflation gets roundup by .5% to a 2-3% range.

Here are the new ranges:

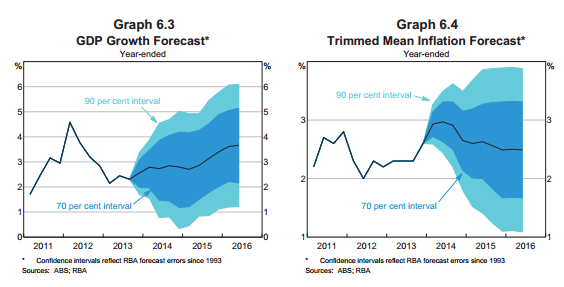

Most importantly for all rate watchers, inflation is expected to fall away. This is a “look through” moment. Here’s the commentary:

The inflation forecasts have been revised higher in the short term, reflecting a combination of the lower exchange rate and the higher-than-expected December quarter CPI outcome, which have more than offset the effect of the softer outlook for wage growth.

The various measures of underlying inflation suggest that the quarterly pace picked up to between ¾ and 1 per cent in the quarter – around ¼ percentage point higher than the assessment of underlying inflation a quarter ago. In year-ended terms, the pace of underlying inflation increased to be a touch above 2½ per cent.

Underlying inflation is expected to reach 3 per cent over the year to June 2014, about ½ percentage point higher than forecast in November. This upward revision reflects the higher-than-expected inflation reported for the December quarter – which is assumed to persist somewhat into early this year – as well as the effect of the further depreciation of the exchange rate since November. Given the slow growth of wages and the limited extent of domestic cost pressures more generally, year-ended underlying inflation is expected to ease back later this year.

Headline inflation is forecast to reach 3¼ per cent over the year to June 2014. In addition to the same factors influencing underlying inflation, the upward revision to headline inflation reflects the increase in the price of tobacco in December. As this and the large rise in fuel prices in the September quarter drop out of the year-ended rate, headline inflation is expected to fall back. Over the forecast horizon, inflation is forecast to be consistent with the target.

The depreciation of the exchange rate since April 2013 is expected to exert mild upward pressure on inflation for several years, reflecting the drawn out pass-through that has occurred historically. The depreciation has seen a rise in import prices, which firms are expected to pass through gradually to final retail prices. In turn, this should encourage consumers to shift some of their spending toward domestically produced goods and services, and may allow domestic producers to lift prices and margins.

Altogether, the lower exchange rate is expected to add around ½ percentage point to underlying inflation over each of 2014 and 2015. However, it could be that the ‘second stage’ of exchange rate pass-through – from import prices (across the docks) to the prices facing consumers – may have been more rapid than has been the case historically.

Working in the other direction, the subdued outlook for the labour market is expected to exert downward pressure on wages and so inflation. Growth in labour costs is expected to remain moderate, while labour productivity is expected to continue to grow. While it is difficult to ascertain the extent to which slower wage growth has been passed on to final prices, the relatively high December quarter inflation outcome suggests that, so far, there has been less pass-through of the slowing in wages to final prices than had been anticipated.

The CPI will also be affected by changes in the price for carbon. As in the previous Statement, the forecasts incorporate a path for the carbon price that is based on current legislation. On this basis, a floating carbon price will be introduced on 1 July 2015, which on present indications would be expected to see the carbon price fall to be similar to that of European permits. Consistent with the previous forecasts, and estimates in the 2013/14 Australian Government budget, this change would subtract a bit less than ½ percentage point from CPI inflation in 2015 and around half that much from underlying inflation.

The government has stated that it intends to repeal the carbon price on 1 July 2014. Based on modelling by Treasury, the introduction of the carbon price was expected to add 0.7 per cent to the CPI and its removal may well result in a reduction in the CPI of a similar magnitude. Under this outcome, the forecast for CPI inflation would be lower by around 0.7 percentage points over the year to June 2015 at around 2 per cent (with inflation in the subsequent period being higher than the current forecasts because the price of carbon would not be declining at that time).

Underlying inflation would respond by less than this, with the forecasts a little more than ¼ percentage point lower over the year to June 2015, at around 2¼ per cent.

The government has also stated its intention to increase tobacco excise in a sequence of steps over a period of four years. The first of these increases was implemented in December, which contributed to inflation in the December quarter and will do so again in the March quarter. Further increases in the excise have not yet been legislated and therefore are not incorporated in the forecasts. If they came to pass,

they would be expected to add around ¼ percentage point per year to the forecasts for headline inflation over the next few years. Underlying inflation would not be affected.

The only point I’ll add is that by declaring this, the RBA has already half of the currency fall engineered since November so it’s increasingly wrong!

There’s more scary stuff on inflation in the risks section:

On the domestic front, at this stage the implications for activity and prices of the higher-than-expected inflation data for the December quarter are unclear.

It could be that there was a higher than usual degree of noise in the data, which can occasionally occur owing to the difficulties of measurement or the timing of price changes. This would imply that the higherthan- expected inflation recorded in the quarter will not persist.

Alternatively, the stronger inflation outcome raises the possibility that there is less spare capacity in the economy than previously thought, which would suggest that the outlook for inflation would be somewhat higher than previously anticipated. This could be because there has been some strengthening of demand in recent months that enabled firms to increase prices. But, while some measures of trading conditions and profitability have improved, the behaviour of share prices for listed retailers and information from liaison do not yet point to a broadbased increase in demand and evidence on changes in profit margins over the recent period is mixed.

There could also be less spare capacity in the economy if supply is increasing more slowly than previously thought. However, this is hard to reconcile with the weak state of the labour market.

Another possibility is that the December quarter CPI outcome reflected, in part, faster pass-through of the exchange rate depreciation than in the past. Such faster pass-through could persist for several quarters, adding to inflation in the near term, or it could prove temporary.

You better hope that the old hands not wrong about the spare capacity in the economy because if the RBA concludes that it will be forced to jack rates and it will be time to run for the hills.

The dollar rose 20 pips.