Boy oh boy. The ISM was out last night and was the worst print I can remember, sending stocks into a tailspin, bonds into melt-up and, worryingly, doing nothing to halt the emerging markets slide.

The ISM gauge collapsed:

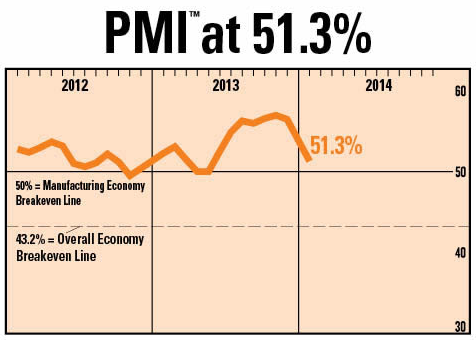

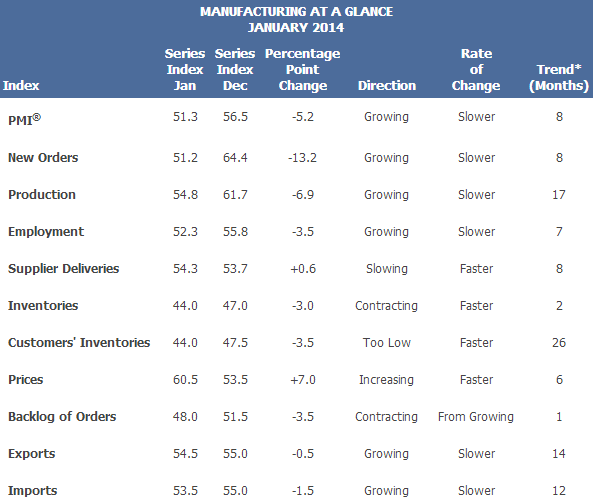

“The January PMI® registered 51.3 percent, a decrease of 5.2 percentage points from December’s seasonally adjusted reading of 56.5 percent. The New Orders Index registered 51.2 percent, a significant decrease of 13.2 percentage points from December’s seasonally adjusted reading of 64.4 percent. The Production Index registered 54.8 percent, a decrease of 6.9 percentage points compared to December’s seasonally adjusted reading of 61.7 percent. Inventories of raw materials decreased by 3 percentage points to 44 percent, its lowest reading since December 2012 when the Inventories Index registered 43 percent. A number of comments from the panel cite adverse weather conditions as a factor negatively impacting their businesses in January, while others reflect optimism and increasing volumes in the early stages of 2014.”

Check out new orders. So, weather issues, yes, but not all. There were downward revisions to previous months as well. The inventory build that has been helping US GDP for the past few quarters may be unwinding a little after an ordinary Christmas. If it is predominantly weather-related it will pass quickly with give back.

Yet taper expectations were hit. As foreshadowed yesterday, the 30 year bond yield took out support at 3.58% and is now in technical free fall at 3.55%:

Advertisement

The ten year rallied sharply as well with yields down to 2.6% but has more technical breathing room with downside support at 2.48%:

Advertisement

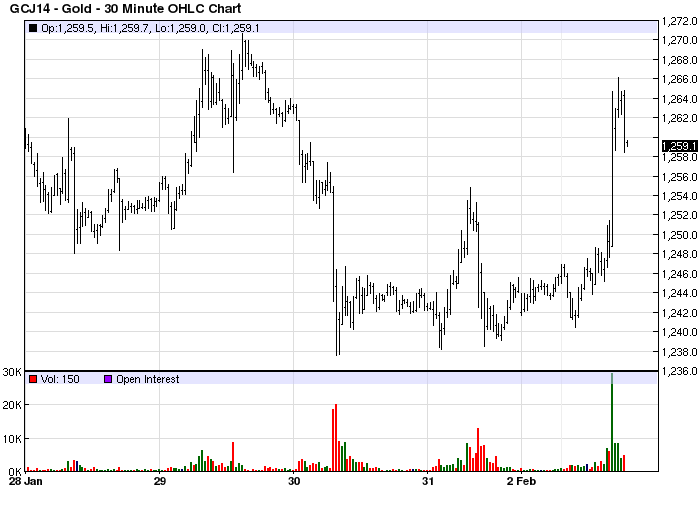

It’s not confirmed “taper taper” until the 10 year yield breaks. Same goes for gold, which liked it, but still hasn’t broken out:

The US dollar weakened by 0.3% and the Australian tried and failed to rally. Stocks were smashed 2%. Disconcertingly, emerging markets FX kept selling:

Advertisement

For now, and with the exception of the 30 year bond yield, these moves look event-based and an opportunity to rid markets of some froth. But we are closer to taper taper than we were yesterday. Welcome Janet Yellen!

Looking forward this week, Non-farm payrolls are not until Friday. Here are a couple of notes on such from Goldman and Merrill via Calculated Risk, Goldies:

Advertisement

Our preliminary forecast for the nonfarm payroll report is a bounceback to a 200,000 pace of increase. There are two key reasons why we expect the report to look strong … Better weather (yes, really). Although the month of January as a whole was quite cold, the payroll survey week was actually somewhat warmer than normal … Even excluding the weather impact, the December employment gain looks to be about 50,000 below the recent trend. In our view, this is implausibly weak relative to other job market measures … This could result in a bounceback to an above-trend pace even outside the weather impact, although it is also possible that the December reading will be revised up.

… we see a drop in the unemployment rate from 6.7% to 6.6%, partly because the expiration of emergency unemployment benefits at yearend may have caused another drop in labor force participation and partly because we expect a good increase in household employment, which has likewise underperformed job market indicators such as claims.

And Merrill:

We forecast nonfarm payrolls to increase 185,000, an improvement from the 74,000 gain in December, but still somewhat below the recent trend. The unemployment rate is likely to slip to 6.6% from 6.7%.

Typically when poor weather conditions result in a downward bias to payroll growth, there will be a positive reversal the subsequent month when those “missing” payrolls reappear on the books. Although job growth was held back in December by the harsh weather, we do not think a strong snap-back will occur in January. … On balance, the weather in January was worse than normal, which would depress activity. While conditions improved for the survey week (since the 12th falls on a Sunday, the pay period is the week of the 13th), the rest of the month was quite cold. In particular, the week prior experienced the “polar vortex.”

…

The benchmark revision to nonfarm payrolls will also be released along with this report. The preliminary revision was for an upward revision of 345,000, or 0.3% of payrolls. This will impact the data from April 2012 through March 2013.

Take that as you will. It would be a circuit breaker if met.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.

{kind=link}