Australian economics’ number one bull, Stephen “Kouk” Koukoulas , has written a snappy and fascinating take on the next few years of Budget politics that is worth a look:

On 12 May 2015, Treasurer Joe Hockey will deliver his second budget and in doing so, he will announce that the budget is back on track, the Labor mess has been cleaned up and that for 2016-17 and beyond, there will be budget surpluses.

The 2016-17 surplus will be the result of the unwinding of the disingenuous forecasts and spending distortions that were contained in Mr Hockey’s Mid-Year Economic and Fiscal Outlook document, released in December 2013, plus some fiscal policy tightening that will start with this year’s budget on May 13.

…The current starting point for the 2016-17 budget bottom line presented in last month’s MYEFO is a budget deficit of $17.7 billion. This seems a large amount but it is just 1 percent of GDP.

The first step in moving from a $17 billion deficit to a surplus number is the reversal of some of the smoke, mirrors and accounting measures presented in the MYEFO.

One important step will be the payment of dividends from the Reserve Bank of Australia to the government as it gives back part of the $8.8 billion that Mr Hockey unnecessarily gave the Bank this year. Further, with the Australian dollar low and interest rates rising, the RBA has more than enough money in reserves that a strong lift in its profits will see it start to give some of the excess cash back. If history is any guide, the RBA dividend in 2016-17 should be around $4 to $5 billion. That’s a nice instalment on the road to surplus.

Another critical element will be the fact that MYEFO presented an unrealistically down beat view of the economy over the three years to 2016-17 which in budgeting terms slices about $10 billion from the budget bottom line in 2016-17 alone.

The level of nominal GDP will be higher, inflation will be higher and the unemployment rate lower than the MYEFO projections, all of which means that even a do-nothing policy approach will see the government pocket at least $10 billion. A stronger upswing will of course mean even more revenue.

…Such is the petty nature of the budget problem that on these two issues alone, the budget deficit for 2016-17 is all but gone.

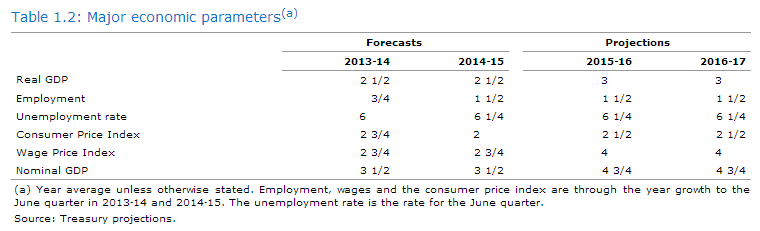

OK, let’s unpack this a little. I can accept the argument about the RBA, even if I don’t agree with it for reasons I’ve cited before. But on this line about unrealistic forecasts I just don’t agree at all. Here are the major parameters from the MYEFO:

None of these is outside of consensus market forecasts. Yes, some economists that focus more on the cycle and expect a successful rebalancing, via house prices and construction, see lower unemployment and better growth. But just as many see roughly this outcome.

Moreover, the old hands of Australian economics – Saul Eslake, Bill Evans, Alan Oster, Tim Toohey – not to mention probably the balance of prominent academic economists – are by and large more bearish than this. Many have unusually high recession risks as caveats as well. All see further interest rate cuts. This is because they are focused on the post-boom structural adjustment to improved competitiveness that Australia must undergo, which includes likely material falls in the terms of trade and a huge plunge in mining investment. MB sides with the old hands.

As well, Treasury economic forecasts have been far too bullish for three consecutive years causing the previous Labor government to miss its Budget surplus forecasts badly and repeatedly. This includes the period that the Kouk himself advised PM Gillard. Can Joe Hockey really be blamed for bringing some sobriety to that recent record?

Given these facts, why is Joe Hockey being tricky rather than prudent? And if the cycle proves to be stronger than the old hands fear, why is that such a crime for the Budget and nation? It’s not. It’s called good budget management. If that works well politically too then that’s a job doubly well done.

The Kouk is forecasting the most aggressive growth and the fastest interest rate hikes for the Australian economy in the market place. He may prove to be right. But he is currently the outlier, not Treasury, nor Joe Hockey.