Credit Suisse asks that question today and it’s answer is reassuring. Asia is in decent shape:

In Figure 3, we detail why some EMs have been more vulnerable than others. Those with the horrendous combination of a large CAD deficit, persistent and high inflation, a large stock of external debt and considerable near-term funding requirement are likely to be prone to further bouts of liquidity withdrawal. Many of these Emerging Markets are concentrated in Central and Eastern Europe. Encouragingly, Figure 3 shows that Emerging Asian economies, some of Australia’s biggest trading partners, remain relatively sound on these measures. Indeed, our simple framework suggests China is the least vulnerable EM. In general Asian economies have current account surpluses, low consumer price inflation and little external debt. They also have considerable FX reserves that can be employed to insulate against potential currency moves. Perhaps the exceptions in Asia are India and Indonesia.

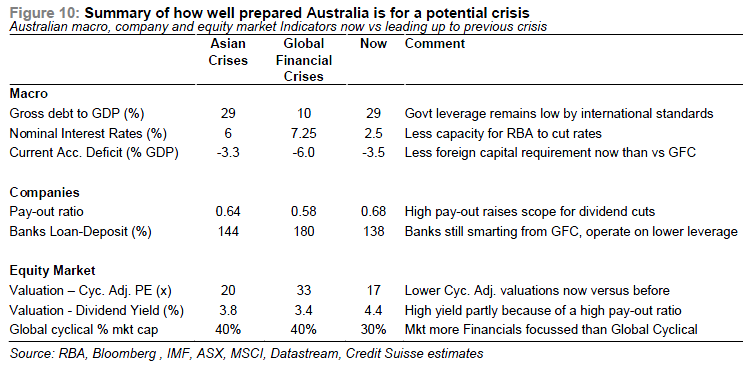

And Australian metrics are solid:

Advertisement

Leading to the conclusion that:

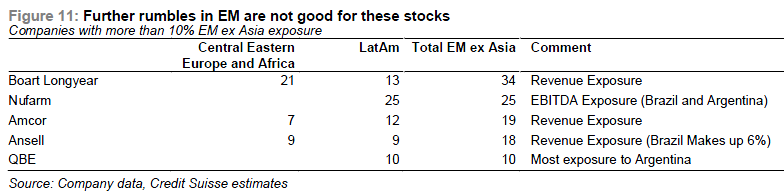

We started the year forecasting a below consensus 9% total return for the ASX 200. Given the recent sell-off our return forecasts are now more interesting and have risen to 14% by year-end. We would be happy to be more aggressive buyers of Aussie equities from here. However, investors need to tread cautiously around those stock more exposed to the current EM concerns. In Figure 11 we highlight five companies where our analysts can identify exposure to Emerging Markets other than those in Asia. We exclude Asia as we believe the region is least vulnerable to the issues currently engulfing other Emerging regions.

This is fair enough. Australia does have significant scope for further fiscal stimulus (though not as large as last time) and the RBA could still cut another 1% or so.

But I wouldn’t be quite so sanguine about equities. The Australian dollar would fall hard and international money would flee to Japan and the US very predictably.

Advertisement

Moreover, the way CS frames its question is that there won’t be an EM crisis in Asia so one should only be wary of those firms with direct exposure to particular markets.

That ignores the fact that there are two forces pressuring emerging markets, not one. The first is the withdrawal of global liquidity via taper. The second is the slowing in, and rebalancing of, Chinese growth so it’s not entirely fair to assume that China is least vulnerable given its centrality to the problem. Even a continuation of lower level disturbance in EMs therefore has the potential to impact Australia more fully than CS suggests via those stocks with China exposure that constitute our major export revenues.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.