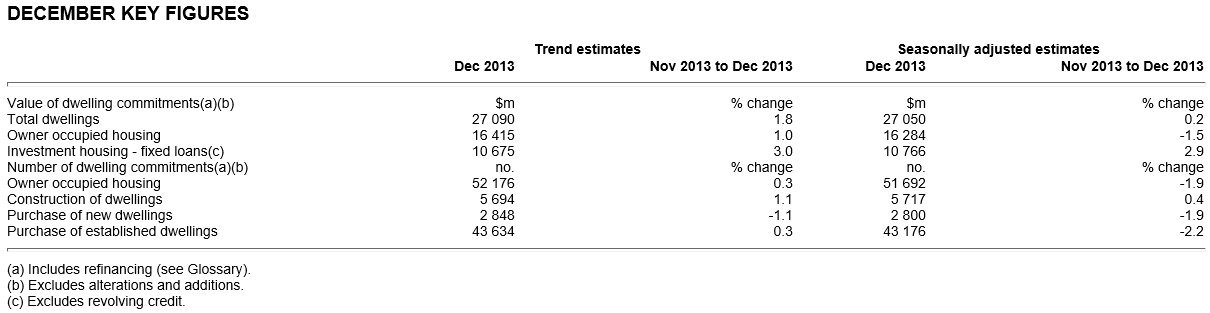

The Australian Bureau of Statistics (ABS) has just released housing finance data for the month of December, which registered a seasonally-adjusted 1.9% fall in the number of owner-occupied finance commitments over the month:

The number of owner-occupied housing finance commitments excluding refinancings registered a seasonally-adjusted 1.0% fall over the month to be tracking 8% above the five-year moving average level. The number of commitments were also up 14.8% on December 2012 (see next chart).

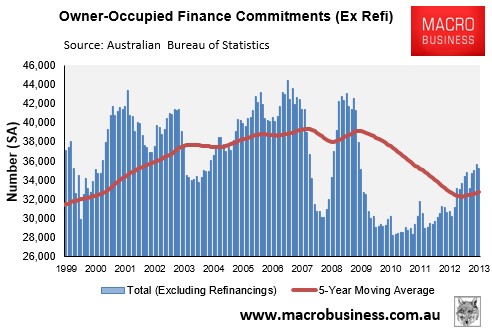

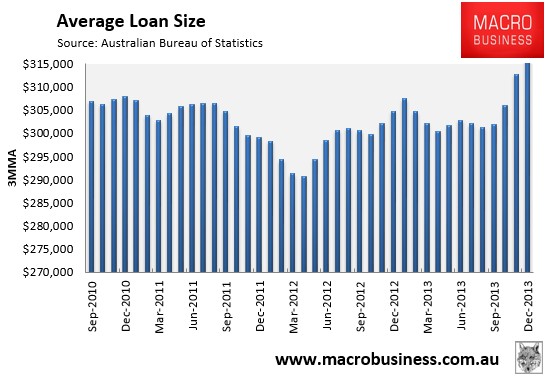

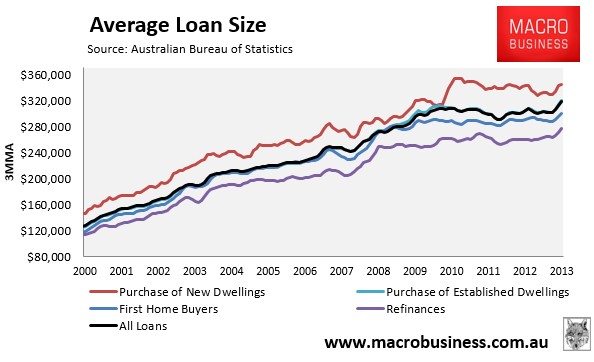

The average loan size rose 0.6% over the month and was up 4.5% over the year. The below charts show the series on a 3-month moving average basis (in order to smooth volatility). Note the recent spike in average loan size after falling since the beginning of last year.

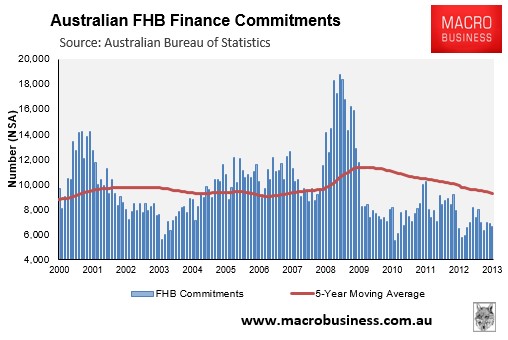

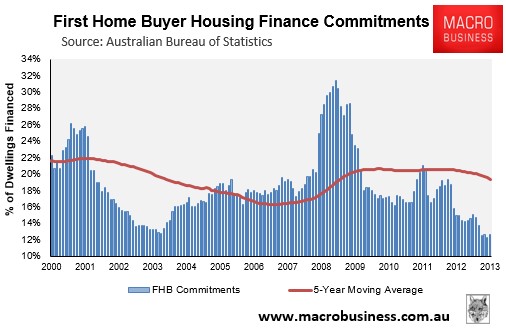

First home buyer (FHB) commitments fell by a non-seasonally adjusted 3.1% in December and represented just 12.7% of total owner-occupied commitments. However, they were up by 2% over the year (see below charts).

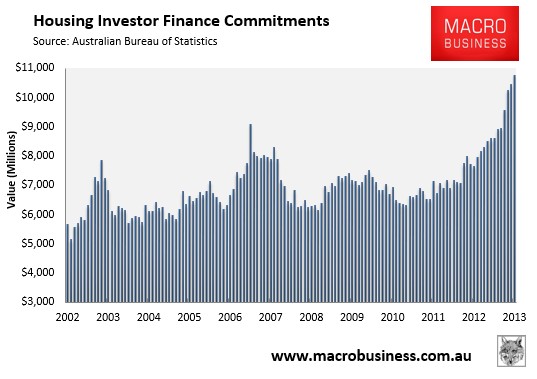

Finally, if you’re wondering what’s primarily driving house price at the moment, look no further. While the ABS only provides the value of investor finance commitments, these were up by another 2.9% in December, 41% over the year, and hit the highest level on record (see next chart).

unconventionaleconomist@hotmail.com