The Business Council of Australia (BCA) has called for a shifting of Australia’s tax base away from personal, company and inefficient indirect taxes, towards more efficient taxes like the GST. From The Australian:

The government is relying too heavily on personal and company income taxes. Individual taxes will reach a 17-year high of nearly 12 per cent of GDP by 2016-17, because of inflation pushing more income into higher tax brackets and the rise in the Medicare levy.

Company tax revenue is vulnerable as mining companies complete new projects and start claiming deductions for them. The BCA calculates that the share of company tax paid by mining firms rose from 7 per cent to close to a quarter over the past decade.

“To the extent that the tax base becomes more reliant on direct and less efficient taxers, then it is likely to be more volatile and detract more from economic growth,” the council says. “It will therefore be important that the government’s white paper on tax reform examines the current tax mix and options such as abolishing inefficient state taxes and broadening the base of the GST.”

A similar view was put forward yesterday by The Guardian’s Greg Jericho, who evaluated the OECD’s suggestion that Australia reduce its reliance on company taxes in favour of GST:

Advertisement

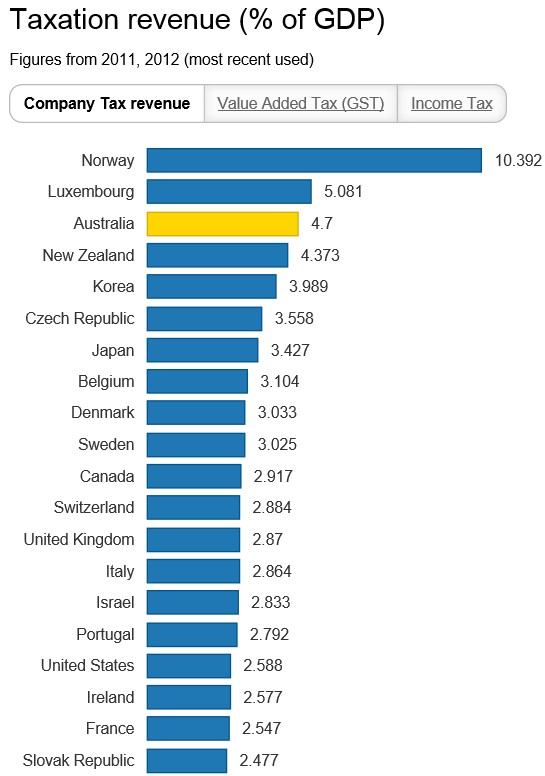

Of all nations in the OECD, we rank third in the amount of company tax revenue we raise as a percentage of our GDP [see next chart]…

While we are less highly ranked on income tax revenue, what is really striking is how little we raise through value-added taxes – like our GST. Of the nations that have such taxes (Ireland, the USA and Korea don’t), Australia takes in the second least amount relative to its GDP. And, given Japan’s consumption tax is about to rise from 5% to 8%, pretty soon we’ll be the lowest.

Jericho also notes that shifting Australia’s tax base from company taxes to GST would greatly improve certainty, since company tax receipts tend to fluctuate wildly in response to the business cycle:

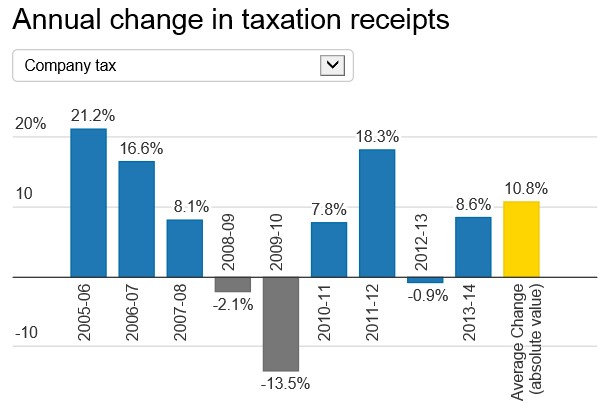

Australia has three main taxes: individual income tax, company tax, and the GST. Of the three, company tax varies the most wildly.

Since 2005-06, company tax revenue has changed in absolute terms on average by 10.8% each year. The average income tax change is 6.8%, while the GST goes up or down on average by only 4.4%:

That provides governments with a lot more surety when they come to planning their budget. And as you can see, during the GFC years of 2008-09 and 2009-10, the GST was the first tax to recover.

Advertisement

Another argument for shifting away from company taxes towards taxes on consumption is that international capital is inherently flighty, making high rates of company tax a big disincentive for international firms looking to locate here. By comparison, consumption is less responsive to increases in tax (we’ve all gotta eat after all!).

Indeed, the Henry Tax Review showed that company tax has “a high marginal excess burden” (i.e. a big loss in consumer welfare relative to the net gain in government revenue), because “it is applied to capital, which is highly mobile”. By contrast, GST is relatively efficient, since it is broadly applied, is difficult to avoid, and does not significantly distort behaviour (see next chart).

Advertisement

That said, another source of taxation that should be considered are broad-based land taxes and mineral rent taxes (back to the future, I know).

While not shown above, both taxes would have similar efficiency to the Petroleum Resource Rent Tax (PRRT) and Municipal rates, since they would be applied to a tax base that is completely immobile – land. In fact, the only loss in efficiency cause by land taxes would come from them being applied non-uniformerly to different land users (as occurs with municipal rates), thereby distorting the pattern of land use. They are also more equitable than consumption taxes, which tend to hit lower income earners harder.

Any discussion about tax reform should, therefore, also include implementing taxes on land/resources in place of less efficient and/or inequitable sources.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.