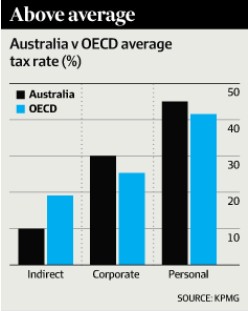

Analysis released today by KPMG research shows that Australia’s 30% corporate tax rate and 45% top marginal tax rate are well above the OECD average of 25.3% and 41.5% respectively, whereas indirect taxes, like the GST, are well below the OECD average (see below chart).

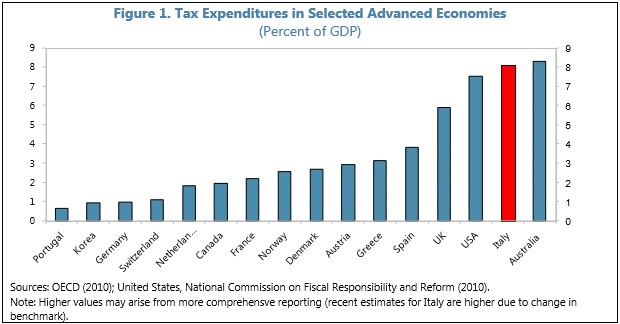

One of the key reasons behind Australia’s high personal and company tax rates is that we lose a significant share of revenue through tax concessions, with tax concessions on capital gains and superannuation alone costing the Budget some $60 billion per year, according to the Australia Treasury. In fact, a report released last month by the IMF revealed that Australia has the highest tax expenditures in the OECD when measured against GDP (see next chart).

With tax expenditures defined by the IMF as:

…government revenues foregone as a result of differential, or preferential, treatment of specific sectors, activities, regions, or agents. They can take many forms, including allowances (deductions from the base), exemptions (exclusions from the base), rate relief (lower rates), credits (reductions in liability) and tax deferrals (postponing payments).

The IMF estimates that tax expenditures reduce Australian government revenue by around 8% of GDP – theoretically enough to eliminate Australia’s Budget deficit. In fact, the huge loss of revenues to tax concessions explains why Australia simultaneously has some of the highest personal and company taxes in the world, yet is also one of the lowest taxing countries in the OECD – a contradiction in terms.

The fact remains that Australia’s tax base has been shrinking – a process that will only worsen as the baby boomers retire en masse and the proportion of workers across the economy declines. It also highlights why reforms must be made to entitlement spending – especially superannuation concessions that overwhelmingly benefit the wealthy and tighter means testing of the aged pension, as well as winding back egregious tax concessions like negative gearing.

More broadly, Australia’s tax base also needs to shift away from personal and company taxes, which the Henry Tax review showed have a “a high marginal excess burden” (i.e. a big loss in consumer welfare relative to the net gain in government revenue), towards the GST, which is considered relatively efficient, since it is broadly applied, is difficult to avoid, and does not significantly distort behaviour (see next chart).

While not shown above, a broad-based land tax should also be considered by the government as a replacement for inefficient and inequitable sources, like stamp duties. Land tax would have similar efficiency to the Petroleum Resource Rent Tax (PRRT) and Municipal rates, since it would be applied to a tax base that is completely immobile – land. In fact, the only loss in efficiency cause by land taxes would come from them being applied non-uniformerly to different land users (as occurs with municipal rates), thereby distorting the pattern of land use.

With the terms-of-trade falling, placing ongoing pressure on national income and tax collections, and the share of workers to retirees set to worsen, revenue holes will need to be plugged and new sources found if Australia’s Budget is to be placed on a sustainable footing.

unconventionaleconomist@hotmail.com