Earnings season is tracking in line with expectations, says Mac Bank:

We analyse the Dec HY13/1H14 Australian profit reporting season to date with 41 companies having reported profit results by COB 13 Feb, representing 17% of companies to report by number (35% by market cap).

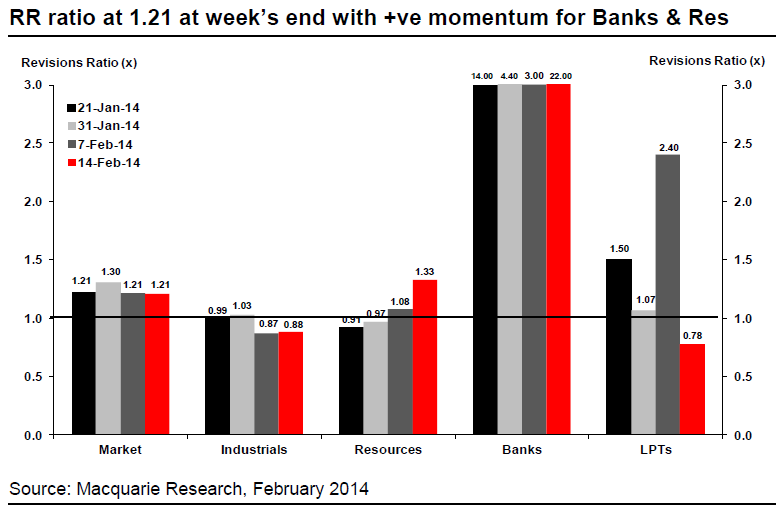

Macquarie’s aggregated All Companies FY14 EPSg (Jun pro-rated) forecast lifted back to +13.1% (+0.2ppts) this week driven by Banks (+1.0ppt to +8.3%) with CBA & ANZ upgraded on an improved impairment outlook. Industrials FY14 EPSg is now +4.8% (-0.4ppt this week) following a week of mixed earnings results (+ve results from NWS, CPU, SGH, DMP offset by BKN, FOX & COH earnings misses), while an accounting standard change driven downgrade to TLS accounts for half this slippage. Resources FY14 EPSgforecast fell 0.5ppt to +44.3% following downward revisions to RIO’s forecast which was partly offset by +ve pre-result forecast adjustments to BHP & FMG. LPTs EPSg is largely unchanged +5.3% (+0.1ppts) with results broadly in line.

Notably post this week’s slippage Industrials EPSg forecast (+4.8%) is now only just above that delivered in FY13 (+4.6%) and surprisingly a higher net interest expense has been a key driver. Revenue growth expectations however have lifted with FY14 revenue forecast +4.6% vs +4.4% previously.

A large number of companies have this reporting season to date upgraded or maintained earnings guidance (CPU, DMP, ANZ, CSL, SGH, CRZ, TCL, TLS & MIN), and have outweighed those to have downgraded guidance, or have a big 2H to deliver (FOX, ASX, GFF, COH, PRY & SKE).

Another standout aspect of this reporting season to date is dividends which continued to positive surprise with 12 out of 41 companies beating MRE’s prereporting season forecast by > +5% from. This week we saw RIO, BKN, SGH, OZL & MCR all delivering better-than-expected dividends.

It’s about bloody time the analysts got it right, just quietly.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.