Goldman Sachs offers some more insight today into the progress of the current earnings season:

Trends remain soft: More misses than beats

It is still early days, with only 18% of companies under our coverage (or 26% of the ASX200) that are expected to report during February having reported. Early trends show more companies surprising to the downside vs GS expectations, with GS analysts downgrading F1 earnings for around a third of companies. Although the magnitude of the downgrades is lower than in the February and August 2013 reporting seasons. The percentage of companies achieving guidance has increased (to 65% vs 51% in the prior February reporting season); history suggests this figure tends to fade as the reporting season progresses.

Lower top-line growth driving cost-out focus Sales growth continues to be the area of disappointment, and cost-out is featuring as a strong theme with a number of companies delivering margin expansion on low or negative sales growth. Median sales growth for companies that have reported for the 6 months to December 2013 is 3.1% on pcp, with EBITDA margins up 0.5% on pcp.

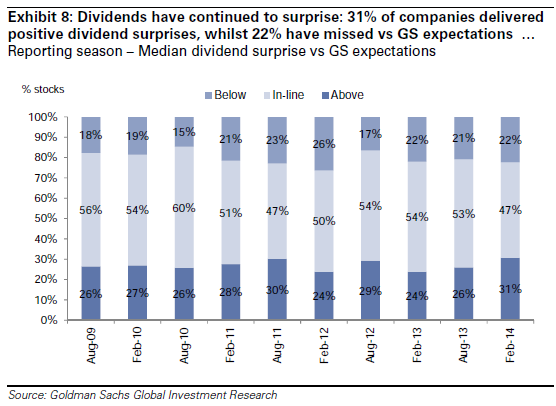

Dividends surprising

With pay-out ratios at all-time highs we continue to believe dividend surprises will be harder to deliver. To date in this reporting season, 31% of

companies (11) have surprised versus GS expectations, with a median surprise of 7.7%, similar to pcp; however, where companies are missing on dividends, the magnitude of disappointment has increased.

As reported earlier, earning’s growth is on track with consensus estimates which will please investors but the it’s the quality of that growth that reflects upon the economy and the two dominant drivers identified by GS are a little discouraging.

Top-line misses, combined with cost-out deflation and margin expansion is a recipe for economic stagnation. It is precisely the combination of forces that has dogged the US since the GFC as a demand deficit has led firms into a never-ending cycle of productivity improvements that has suppressed investment and employment, leading to further demand deficit.

Advertisement

Add in a fixation with dividends and firms have even less motivation to invest and their grow head count. It’s a jobless profit season and recovery.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.