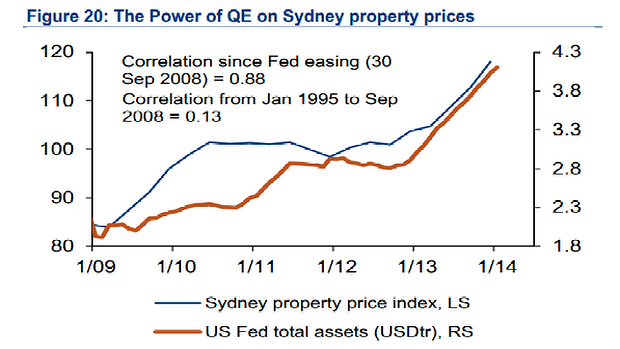

This chart shows how Sydney property prices have been highly correlated to US monetary expansion.

It reveals “the power of the Fed balance sheet since 2009 and its impact on asset prices,” say analysts Bank of America-Merrill Lynch.

It’s one of a number of exhibits from the investment bank’s strategists, who in their note warn investors to get ready for the end of the carry trade in emerging markets as QE is pulled back.

“Carry trade” refers to a strategy where investors borrow cheaply in a low-yielding currency, such as the US dollar, to buy a range of high-yielding assets around the world.

London property is another asset that has moved in line with monetary expansion out of the US, although these also reflect “some spillover EM demand” write the analysts.

Other assets that have been highly correlated to QE according to BoA-ML are: US biotech and tech stocks, EM gaming stocks, and EM internet stocks.

“Could the party go on? Yes, if for some reason – a significant deterioration in the US labour market, or a deflationary shock from China, or any other surprise that could lead to a cessation of the US tapering could prolong this carry trade,” write the analysts.

“This is not the house base case. We believe it is better to start preparing for a post-QE world. As one of our smartest clients told us: ‘The main theme in the past five years was QE; if that is coming to an end, investments and themes that worked in the past five years must therefore be questioned.’ We agree.”

It’s an interesting thought and has relevance to the past eighteen months when the RBA has had to cut interest rates in part to drive down the dollar because of the QE carry into it. All things equal that should reverse with taper and US rate rises.

A second channel of influence for the Fed in Australian house prices is through our bank’s cost of funds. If some element of the US dollar carry trade effects bank bond demand (and it probably does) then there’ll be an impact when the money tide goes out. We already saw that when bank bond prices spiked during the ‘taper tantrum” mid last year, though it was difficult to dis-aggregate that from the influence of China’s interbank credit crunch at the time.

Advertisement

There is almost certainly a strong element of hot money in the major bank’s deposit bases as well, so draining those will also place upwards pressure on interest rates.

Advertisement

However, to date, none of that has been especially apparent in bank funding costs and certainly not enduring. Indeed it’s all been far outweighed by the relaxation in markets following the beginning of European QE and Australians own new found savings habits.

And there’s a much bigger issue emerging with the taper which suggest it could actually boost Australian house prices for a time as interest rates fall further. The China slowdown dovetails with the taper to create a negative feedback loop between emerging market (EM) exports, cost of funds, and falling commodity prices.

Advertisement

Australian interest rates were always going to have to fall heavily as China slowed and the capex cliff approached. The magnitude of this headwind is the major reason I see interest rates falling further in this cycle. Add an emerging markets crisis and the cash rate could be cut again, though if markets were disrupted enough then the bank’s cost of funds will rise as well, meaning the bank cartel might may keep the cuts for themselves. There is ultimately a significant risk that slowing EMs eventually overtake and reverse the taper as well.

Advertisement

Correlations between the Fed and Australian house prices are neither as simple, direct nor predictable as the SMH post suggests.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.