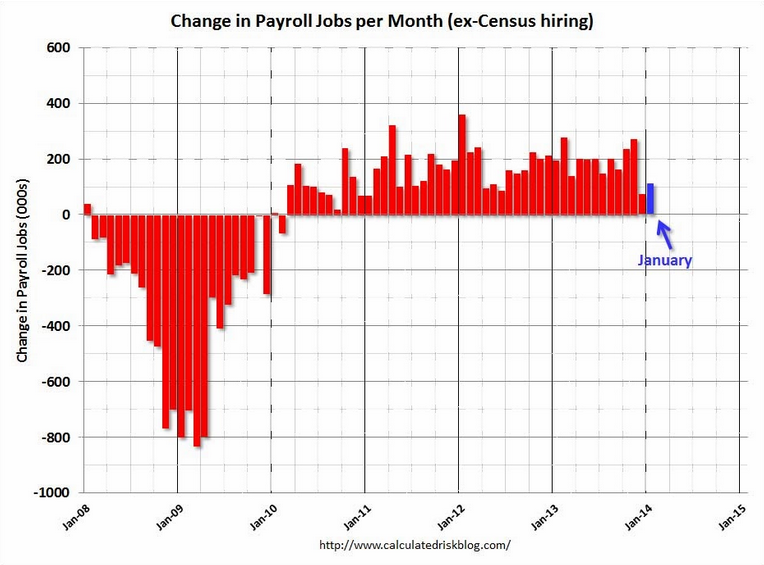

The US payrolls report was another dud, delivering miles below consensus at 113k versus 180k expected. Here’s Goldman with the details (chart from CR):

BOTTOM LINE: The January employment report contained a confusing set of data, as payroll job growth significantly disappointed, but the unemployment rate declined by one-tenth, reflecting large gains in household employment. Overall we see the report as slightly weaker than expected.

Nonfarm payroll employment rose a disappointing 113k in January (vs. consensus +180k). By industry, retail trade declined 13k (vs. +63k in December), while health and education services?normally a consistent support for headline job growth?declined for the second consecutive month (-6k). Construction employment, which declined 22k in December amid adverse weather, added 48k, suggesting little negative weather impact in the January report. Government employment fell 29k, the worst performance since October 2012, split between federal (-12k) and state and local (-17k). Payroll job growth in November and December was revised by a cumulative 34k, consistent with the general tendency for positive back-revisions in the January report. Over the past three months, payroll employment rose an average rate of 154k per month.

The January report also contained annual benchmark revisions to the establishment survey data, which increased the level of employment in March 2013 by 369k, compared with +345k in the preliminary estimate. However, the upward revision was mainly due to adding new categories of home health care workers under the scope of payroll employment.

The unemployment rate declined by one-tenth to 6.6% in January. Employment rose by 638k according to the household survey, while “payroll-consistent” employment?adjusting for definitional differences between the two surveys?rose by 901k. Labor force participation rose two-tenths to 63.0%, against expectations that the expiration of Emergency Unemployment Compensation benefits might lead some unemployed workers to stop reporting that they were actively seeking employment. The effect of new population controls accounted for only 22k of the rise in employment and did not affect the unemployment rate or the participation rate. The January report also showed a four-tenths decline in the broader “U6” underemployment rate to 12.7% as a result of a decline in the number of involuntary part-time workers.

Average hourly earnings rose 0.2% in January (vs. consensus +0.2%), and increased 1.9% over the past year (vs. consensus +1.8%). The average workweek remained unchanged at 34.4 hours (vs. consensus 34.4), consistent with little adverse weather impact in the report.

With payrolls, unemployment claims, consumer sentiment, and a number of business surveys in hand, our preliminary read on the January current activity indicator (CAI) is 2.7%, up from December’s 1.9%.

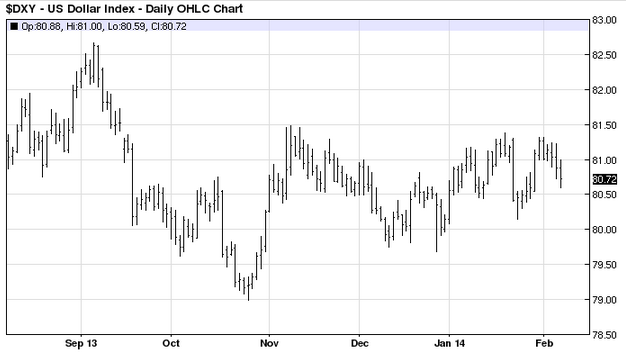

Hardly a ringing endorsement. Some markets immediately signaled a slowing taper. Stocks took off for 1%. The US dollar shrank marginally but is caught in a range:

Advertisement

Gold jumped one percent but has not broken out despite a clear uptrend:

Some taper taper movement then but far from convincing. Fed mouthpiece, Jon Hilsenrath also shot down the idea (the whole video is worth watching):

Advertisement

“They laid out a strategy for gradually unwinding this thing. I think that they stick to that until they see more convincing evidence that the economy is somehow receding back the disappointing that they were trying to get us off”

Long bonds did rally a little but the thirty yield breakdown has proven a false break so far and the 10 year looks firm above support:

Advertisement

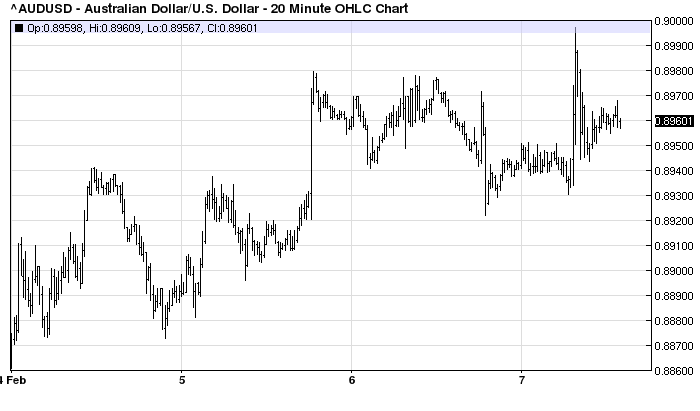

The confused or mixed market reaction was also expressed in the Australian dollar, which first jumped to 90 cents then sold off and settled slightly above Friday’s close:

Advertisement

That’s probably as good a read as any. Taper taper is closer but no cigar.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.