In their discussion of the path for monetary policy, most participants judged that the incoming information about the economy was broadly in line with their expectations and that a further modest step down in the pace of purchases was appropriate. A couple of participants observed that continued low readings on inflation and considerable slack in the labor market raised questions about the desirability of reducing the pace of purchases; these participants judged, however, that a pause in the reduction of purchases was not justified at this stage, especially in light of the strength of the economy in the second half of 2013. Several participants argued that, in the absence of an appreciable change in the economic outlook, there should be a clear presumption in favor of continuing to reduce the pace of purchases by a total of $10 billion at each FOMC meeting. That said, a number of participants noted that if the economy deviated substantially from its expected path, the Committee should be prepared to respond with an appropriate adjustment to the trajectory of its purchases.

Participants agreed that, with the unemployment rate approaching 6-1/2 percent, it would soon be appropriate for the Committee to change its forward guidance in order to provide information about its decisions regarding the federal funds rate after that threshold was crossed. A range of views was expressed about the form that such forward guidance might take. Some participants favored quantitative guidance along the lines of the existing thresholds, while others preferred a qualitative approach that would provide additional information regarding the factors that would guide the Committee’s policy decisions. Several participants suggested that risks to financial stability should appear more explicitly in the list of factors that would guide decisions about the federal funds rate once the unemployment rate threshold is crossed, and several participants argued that the forward guidance should give greater emphasis to the Committee’s willingness to keep rates low if inflation were to remain persistently below the Committee’s 2 percent longer-run objective. Additional proposals included relying to a greater extent on the Summary of Economic Projections as a communications device and including in the guidance an indication of the Committee’s willingness to adjust policy to lean against undesired changes in financial conditions.

A few participants raised the possibility that it might be appropriate to increase the federal funds rate relatively soon. One participant cited evidence that the equilibrium real interest rate had moved higher, and a couple of them noted that some standard policy rules tended to suggest that the federal funds rate should be raised above its effective lower bound before the middle of this year. Other participants, however, suggested that prescriptions from standard policy rules were not appropriate in current circumstances, either because the target federal funds rate had been constrained by the lower bound for some time or because the equilibrium real rate of interest was likely still being held down by various factors, including the lingering effects of the financial crisis, and was significantly below the value of the longer-run rate built into standard policy rules.

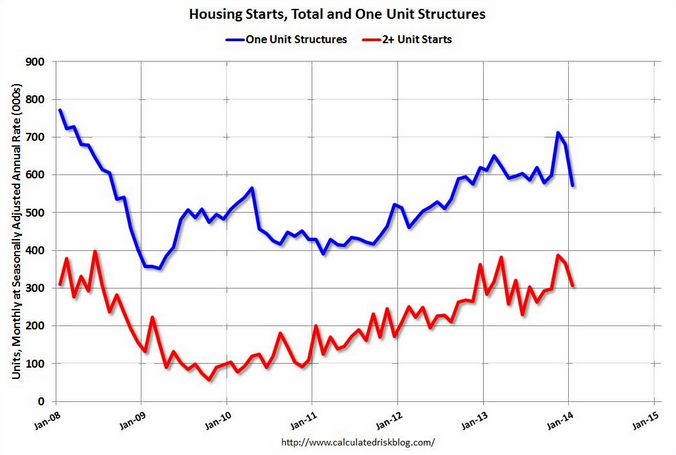

Housing Starts:Privately-owned housing starts in January were at a seasonally adjusted annual rate of 880,000. This is 16.0 percent below the revised December estimate of 1,048,000 and is 2.0 percent below the January 2013 rate of 898,000. Single-family housing starts in January were at a rate of 573,000; this is 15.9 percent below the revised December figure of 681,000. The January rate for units in buildings with five units or more was 300,000.

Building Permits:Privately-owned housing units authorized by building permits in January were at a seasonally adjusted annual rate of 937,000. This is 5.4 percent below the revised December rate of 991,000, but is 2.4 percent above the January 2013 estimate of 915,000.Single-family authorizations in January were at a rate of 602,000; this is 1.3 percent below the revised December figure of 610,000. Authorizations of units in buildings with five units or more were at a rate of 309,000 in January.

Advertisement

This data is partly weather affected. The biggest fall was in the frozen Mid West, where the pace of starts dropped 68% month on month. Having said that, the worst-effected North East rose by roughly the same amount and the South and West (where weather is no issue) both fell sharply. Permits showed weakness in the Northeast, strength in the Mid West and South and a collapse in the West.

The 2013 surge is now gone. It’s a mix of bad luck and a struggling housing pulse.

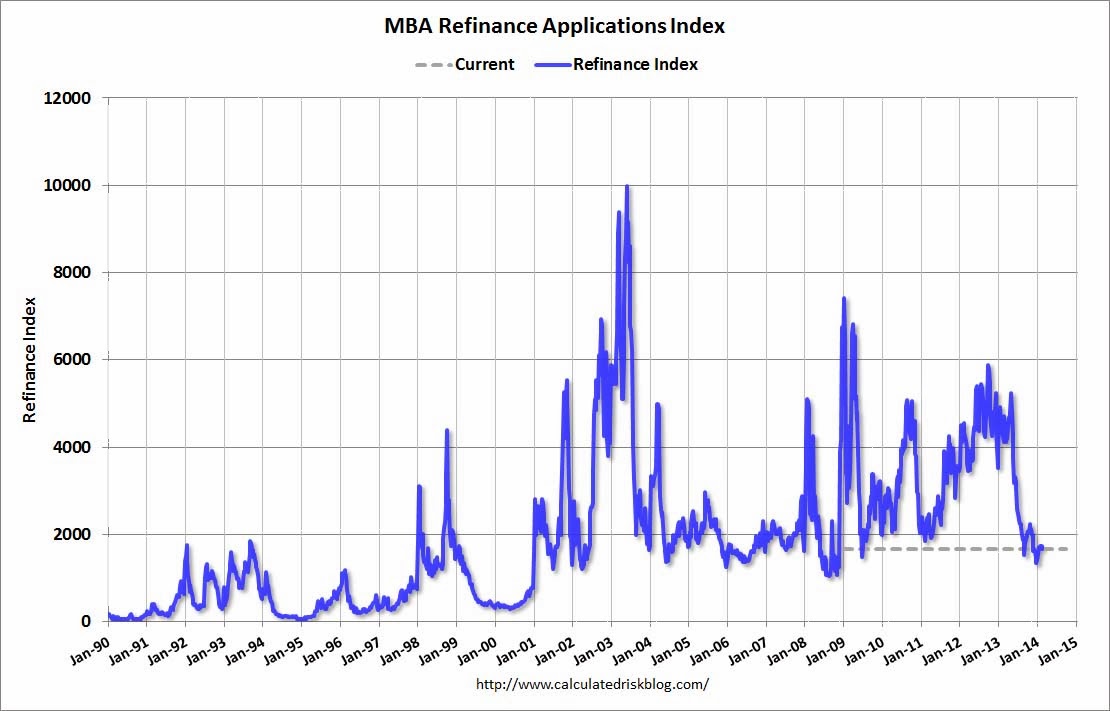

The same fade was apparent in the Mortgage Bankers Association (MBA) weekly mortgage applications data which is plumbing new lows every week now:

Advertisement

Mortgage applications decreased 4.1 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending February 14, 2014….The Refinance Index decreased 3 percent from the previous week. The seasonally adjusted Purchase Index decreased 6 percent from one week earlier and is at its lowest level since September of 2011.

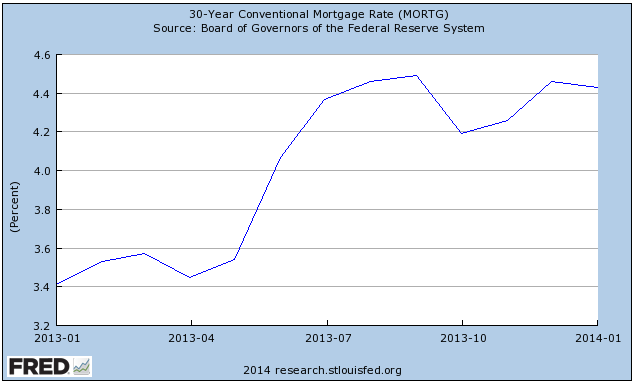

…The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($417,000 or less) increased to 4.50 percent from 4.45 percent, with points decreasing to 0.26 from 0.34 (including the origination fee) for 80 percent loan-to-value ratio (LTV) loans.

The refi index has a good history of leading house prices so I expect gains to whither in the months ahead, slowing the whole caboodle further.

This is despite a clear plateau (and mild falls) in mortgage rates as long bond yields have responded to the spate of weak data:

Advertisement

So, a determined Fed, more weather troubles and more weakness under that as well but markets were happy enough with the cold. Stocks couldn’t find a bid, bond yields rose a half percent, gold fell the same, the US and Australian dollars were up and down a bit. Lots of under-reaction to strong Fed words.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.