The past month has added much colour (and a great deal of uncertainty) to the taper debate. Post December’s taper, FOMC communications have remained very upbeat, while available data has been erratic. This disparity is a forerunner of the tension that will be with us throughout 2014. Now that the Fed has begun the tapering process, they will be much more willing to weather poor data before seeing a need to respond by halting the process.

The FOMC has initiated the tapering process on the expectation that it will not impair aggregate growth and that underlying momentum will outweigh dwindling headwinds. The problem is that, as attested by the data, there is a great deal of uncertainty over the financial and economic impact of tapering and whether the FOMC’s growth perceptions are in keeping with reality.

San Francisco Fed President John Williams recently highlighted just how optimistic some FOMC members had become. He noted that, following Q3’s 4.1% annualised GDP outcome, growth of above 3.0% was expected in Q4 and that this momentum should continue through 2014 and 2015. This is consistent with FOMC members’ 2014 and 2015 forecasts of 3.0% and 3.2%. These forecasts are based on a theoretical assessment of what underlying momentum is, i.e. growth absent the assumed 1–1.5ppt 2013 fiscal drag.

The problem with this position is that real underlying momentum is very difficult to assess. Indeed, there is reason to suspect that the sequestration is still being felt, owing to time delays between budgeting and enacting spending cuts, and that negligible income growth is limiting the capacity of US households to bounce back from 2013’s tax increases. Ergo, the fiscal drag could prove more protracted and underlying momentum may be well below the FOMC’s expectation.

A better proxy for the overall current wellbeing of the US economy is the pace of domestic final demand. At 2.3% annualised, it was reasonable in Q3, but at best could be described as around trend. Note that the 4.1% headline GDP outcome was primarily driven by inventories. What’s more, over the year to Q3, domestic final demand growth was weak at 1.6%. Aside from the impact of direct government spending cuts, the primary reason for this poor momentum is continued lacklustre growth in household consumption and associated soft business investment.

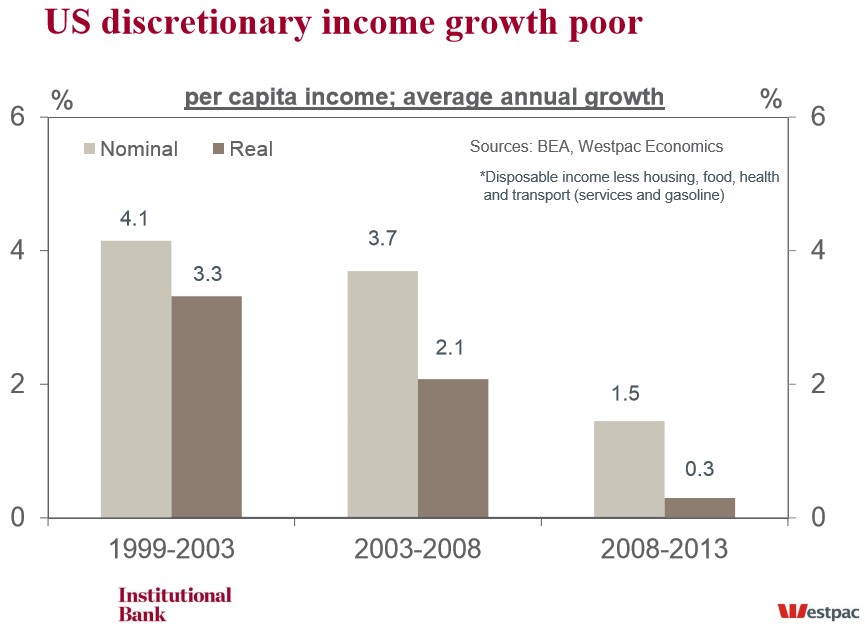

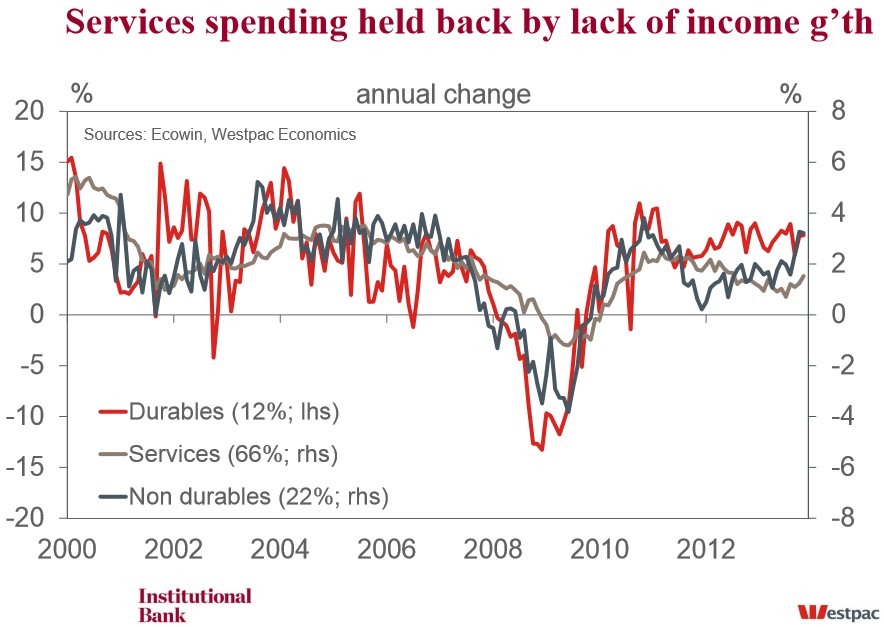

For households, while much has been made of robust retail sales (despite November’s strengthening momentum being revised away), little has been said about the soft pace of services consumption (two thirds of total household outlays), or the importance of consumer credit to durables demand. Annual growth to Q3 in services consumption was underwhelming at 1.0%yr. Set against the almost 8%yr growth in durables goods and near-record low savings rate, this result highlights consumers are being forced to compress spending on services to finance consumption elsewhere. This is not a picture of a broad, self-reinforcing upswing; rather, it is indicative of households just getting by.

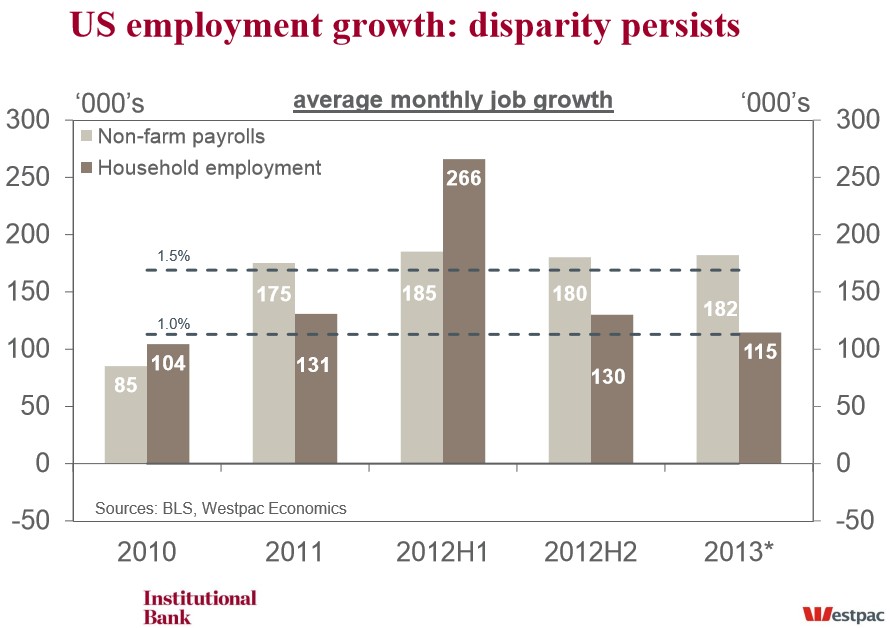

For 2013 as a whole, monthly payrolls growth has averaged 182k, basically unchanged from 2012’s 183k. Also, through Q4, payrolls growth averaged 172k. Job creation is therefore not only below the FOMC’s oft cited 200k threshold, but momentum is heading in the wrong direction.

What is missing are improvements in income growth that households can trust as permanent. Tracking jobs is just a shortcut to estimating income: hours worked times the remuneration of those hours. Real wages remain moribund, simply because employers retain the upper hand over employees due to still considerable labour market slack.

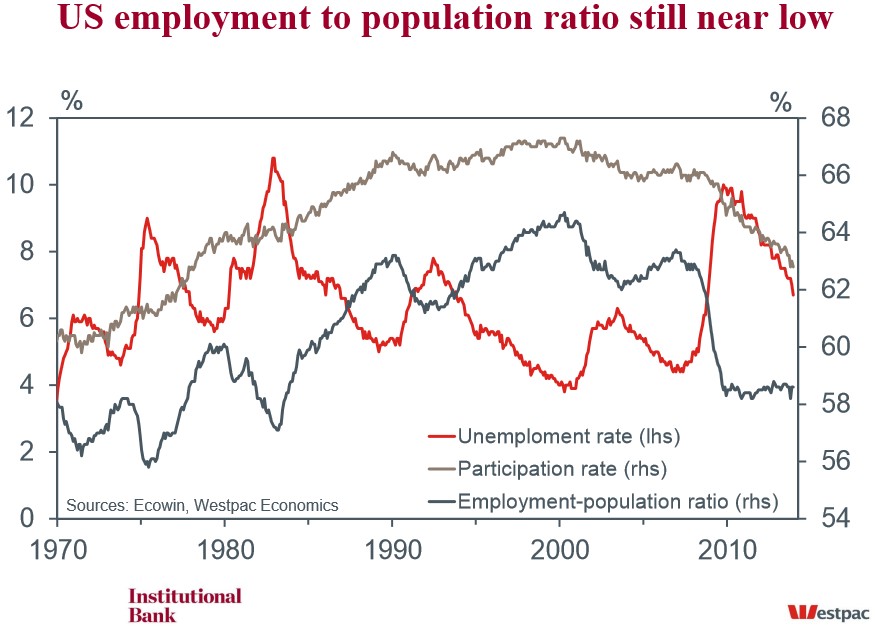

The degree of slack is best represented by the employment-to-population ratio which has barely risen off its multi-decade low. As we have noted many times, it is important to recognise that a material portion of this slack is owing to the lower participation of 25–54 year old workers, not just the ageing workforce. What’s more, the end to unemployment benefits for the long-term unemployed looks to be further discouraging job seekers. This is a fundamentally different picture to the FOMC’s perception of the labour market, primarily based on the participation-rate driven decline in the unemployment rate.

As made clear in a recent speech by Philadelphia Fed President Charles Plosser, FOMC participants are concerned that the GFC and ensuing recession has lowered the level of potential GDP, creating the possibility of higher inflation even under modest growth conditions. But, if our broader focus on activity is accurate, then inflation will remain benign for the foreseeable future. We agree that potential GDP is lower, but interpret this finding differently from the point of view of future growth and inflation outcomes.

In conclusion then, if 2013 has taught us anything, it is that the US economy remains in a frail state. We are yet to see a protracted upturn in hiring and, more broadly, excluding the contribution from inventory accumulation, demand over the year has remained sub-trend. This is not to say that the FOMC will not look to continue to taper in a considered way as and when the economy and markets allow, but it does mean that the end of systematic Fed asset purchases remains further off than many observers are thinking.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.