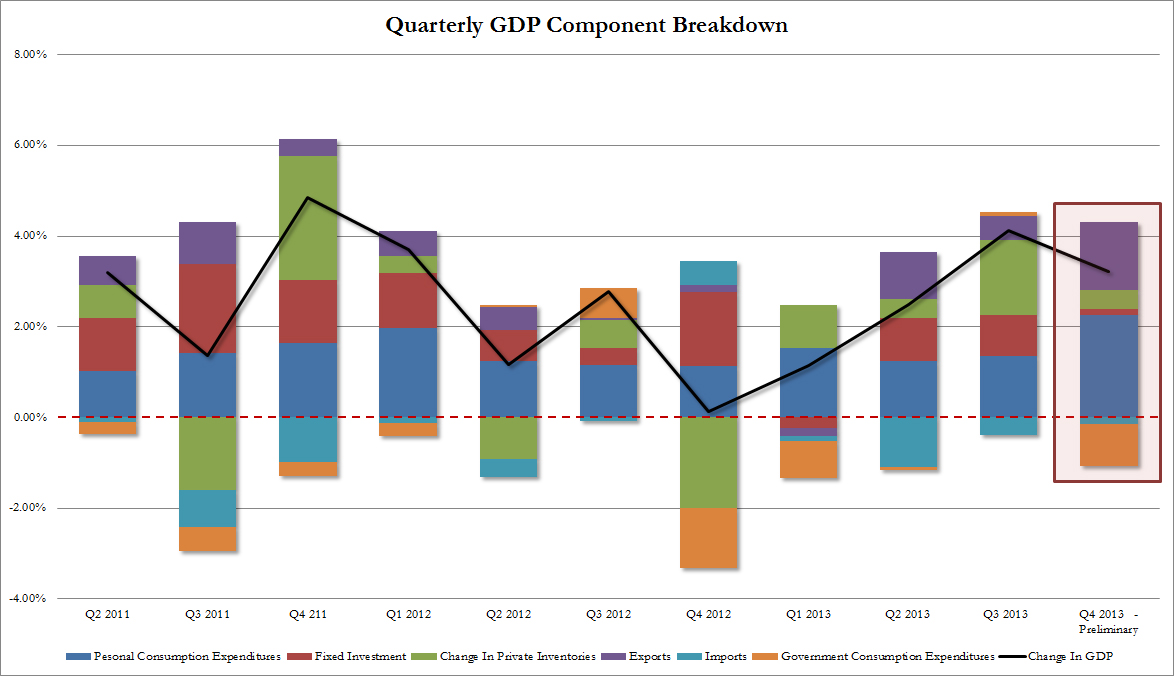

A positive preliminary Dec QTR GDP number helped steady markets last night registering 3.2% annualised, down from 4% in Q3. The composition improved too with inventories contributing far less and the consumer far more:

But that’s where the good news ended. In fact, all other data on the night was poor and rather begged the question did markets rally because of growth or because taper is looking a little more shaky? Wider markets answered that question decisively with the US dollar up half a percent, gold punished nearly 2%, bonds sold modestly and stocks up one percent. Markets liked the growth.

Still the lineup of misses was impressive. Goldman lowered its Q114 GDP estimate:

Real GDP increased at a 3.2% rate in Q4 (vs. consensus 3.2%). Personal consumption expenditures rose a smaller-than-expected 3.3% (vs. consensus 3.7%), which was still the fastest rate since 2010. Business fixed investment rose 3.8%, held down by a 1.2% decline in structures investment following two quarters of strong gains. Equipment investment rose a solid 6.9%. Business inventories added four-tenths to headline growth. Residential investment declined 9.8%, reflecting in part the lagged impact of weaker housing starts in past quarters. Net exports were also a strong positive contributor, adding 1.3 percentage points to growth. Federal government spending fell 12.6%, pushing total government spending down 4.9%. The Commerce Department estimated that the federal government shutdown subtracted three-tenths from GDP growth. Although the composition of this morning’s report was slightly softer than expected, solid 2.9% growth in real final sales to private domestic purchasers suggests positive underlying momentum heading into 2014.

The Pending Home Sales Index, a forward-looking indicator based on contract signings, fell 8.7 percent to 92.4 in December from a downwardly revised 101.2 in November, and is 8.8 percent below December 2012 when it was 101.3. The data reflect contracts but not closings, and are at the lowest level since October 2011, when the index was 92.2.

Lawrence Yun, NAR chief economist, said several factors are working against buyers. “Unusually disruptive weather across large stretches of the country in December forced people indoors and prevented some buyers from looking at homes or making offers,” he said. “Home prices rising faster than income is also giving pause to some potential buyers, while at the same time a lack of inventory means insufficient choice. Although it could take several months for us to get a clearer read on market momentum, job growth and pent-up demand are positive factors.”

The weather looks like an excuse to me with a coast to coast slowdown underway.

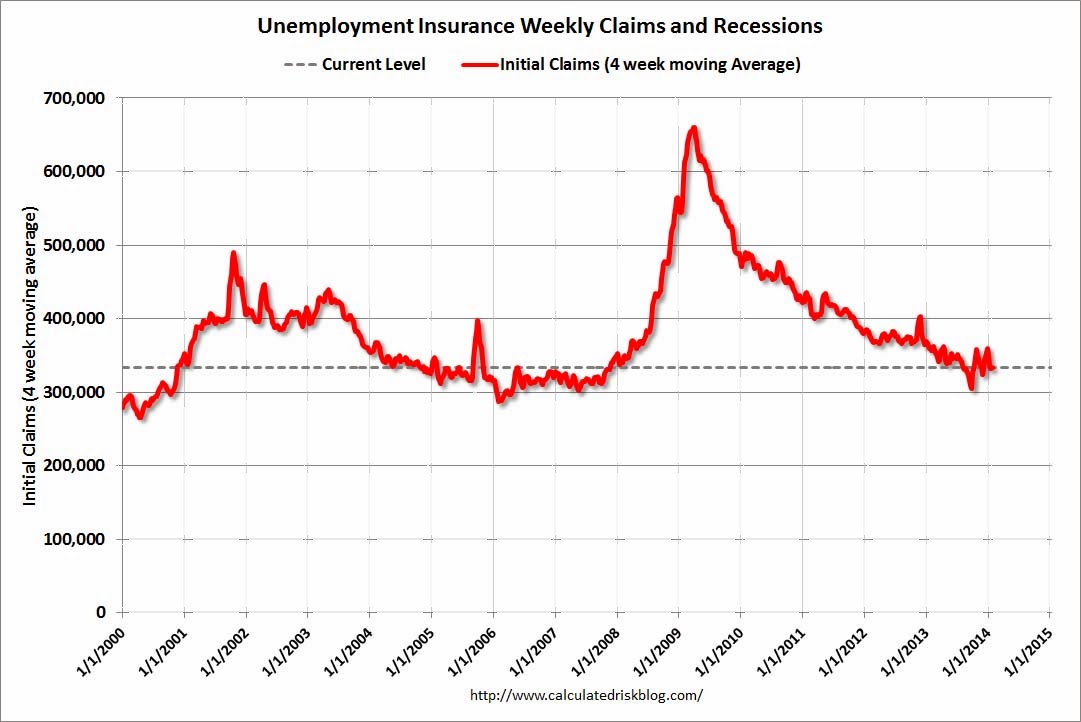

Also missing was Weekly Unemployment Claims, which have clearly plateaued (chart from CR):

In the week ending January 25, the advance figure for seasonally adjusted initial claims was 348,000, an increase of 19,000 from the previous week’s revised figure of 329,000. The 4-week moving average was 333,000, an increase of 750 from the previous week’s revised average of 332,250.

There was no doubt a bit of dead cat bouncing going on in markets last night as well.

Don’t get me wrong, I still expect decent US growth this year, closer to 3%, and recent market turmoil will actually help the housing market as the long bond is bought and interest rates are capped or even fall. If not, the Fed will slow down!