Royal Bank of Canada (RBC) puts its money where its mouth is today:

We are taking out our last RBA cut following Q4 CPI, further A$ weakness, and ongoing signs of policy traction. But we expect an easing bias to linger with cash to stay at an historical low into 2015.

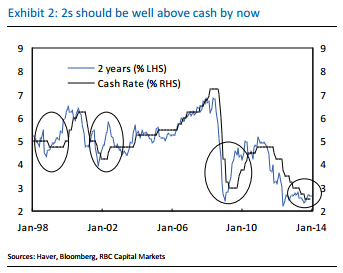

Given that we think cash has bottomed, 2 year ACGBs look expensive at 2.65% and we are entering a strategic short. Setbacks may occur amid ongoing domestic growth/labour market challenges and global risks, but history suggests that cash-2s should be much steeper than 15bps at this stage of the cycle. We target 3.30% by year-end.

The odds of further RBA easing have declined further over the last several weeks, such that the balance of risks now suggest that the RBA’s cut in August 2013 was the last for this cycle. We are consequently removing the Q2 cut from our profile but we expect cash to stay at 2.50% until well into 2015. We outline three key factors for our view change.

i) Q4 CPI provides a little less policy flexibility

As we noted in our analysis of the data, Q4’s CPI raised more questions than it answered. In particular, the failure of weak wage and unit labour costs to weigh on inflation of discretionary services is puzzling. We suspect this uncertainty will be echoed at the RBA, which is now faced with a higher starting point for inflation at slightly above the midpoint of its 2–3% target over the forecast period. Our own revised forecasts now envisage core inflation trending around 2½% or slightly above, which provides an inflation outlook that is distinctively different from our previous profile of ~2.25%.

ii) The exchange rate weakens further

The TWI is at fresh three-year lows, having fallen 7% since the RBA last updated the public on its forecasts and a total of 16% since its April peak. This fall has been larger than we had envisaged, and it comes without material falls in bulk commodity prices. There have been tentative signs of improvement in trade-exposed sectors, with the services trade balance showing trend improvement and sentiment indicators also ticking higher over Q4. And, tradeable inflation appears to be trending higher.

iii) Signs of policy traction continue

House prices are running ~10%y/y nationally and the supply side appears to be (finally) responding. Approvals rose to historically high levels in Q4, and finance data, whilst still a little patchy, suggest that construction should firm throughout 2014. Household spending has also picked up, reflecting firmer asset prices, lower mortgage payments, and also the solid rate of population growth.

However, RBC also provides one big, fat caveat:

Our views around the cash rate into 2015 remain broadly unchanged; whilst the low point may be 25bps higher than we were previously expecting, cash is likely to stay at an historical low for an extended period amid both domestic and global challenges. Sub trend growth as the rotation in activity away from capex/mining remains tough, and a weak labour market suggests that an easing bias will linger and the risks for 2014 are still skewed toward a cut rather than a hike. Indeed, we find it hard to make the case for policy normalisation until further into 2015. Globally, uncertainty over EM, Chinese growth, credit and banking, and lingering European headwinds are all likely to flare up at various times during the year.

I continue to expect policy innovation rather than rate rises from the RBA and still see a rate cut as the next move.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.