The RBA has released a new research paper looking at past terms of trade booms and how the economy coped with their demise. Here is the conclusion:

Australia’s current terms of trade cycle has parallels with earlier episodes.

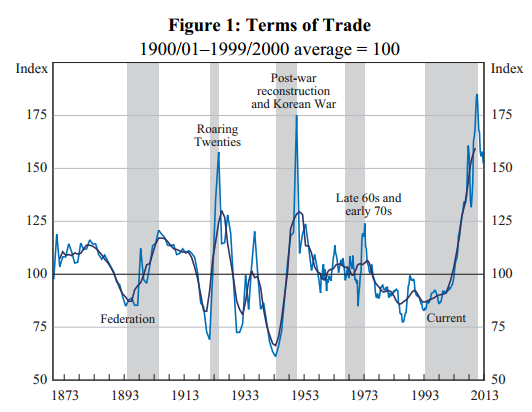

Historically, large movements in the terms of trade were mainly driven by changes in export prices, particularly wool, which reflected strong demand from industrialising economies, coupled with adverse supply developments, such as drought. Upswings in the terms of trade have generally boosted domestic demand, usually with a sizeable contribution from investment, probably reflecting both a direct response to higher commodity prices and the associated improvement in wealth and confidence. In some episodes, growth in immigration and pent-up demand following war also supported growth in investment. Typically, net exports have contributed little to economic growth during the upswing in the terms of trade; sluggish supply responses are exacerbated by the real exchange rate appreciation, which dampens growth in other exports and supports imports. Many of these features have been present in the current episode.

The current episode, however, has some distinct features. One is that it has been mostly related to bulk commodities, instead of rural commodities. Consequently, the sluggish response of supply partly reflects the characteristics of resources investment – namely long periods to plan and gain approval for projects and the need to develop infrastructure. However, just as Australia was the world’s major source for internationally traded wool throughout previous episodes, today it is the world’s largest exporter of steel-making materials and it is likely that Australia will also become a major source of liquefied natural gas exports in the coming years. A decline in the terms of trade is therefore, to some extent, the result of new supply from Australian producers coming on-line.

The most recent upswing was the largest sustained increase of the terms of trade on record, and the Australian economy is likely to continue to be a beneficiary of strong growth in Asia. Indications suggest China’s industrialisation and urbanisation process, which has underpinned the increase in demand for steel-making commodities, is likely to continue for a number of years, although it may well grow more slowly than in the past. Chinese infrastructure needs remain large; an example is that steel demand for residential construction is not estimated to peak until around 2024 (Berkelmans and Wang 2012). While the path of economic development is not always smooth, it is important to remember that this is not the first episode during which one country and a narrow range of commodities have been of particular importance to the Australian economy; rather, that is the norm.

Another stark difference is that despite the unprecedented movement in the terms of trade, the macroeconomic adjustments in Australia have been relatively smooth.

Inflation, for example, has remained contained, in contrast to many previous experiences, such as the Korean War wool boom. Furthermore, inflation expectations have remained relatively low and stable. Factors facilitating this include the greater flexibility present in the labour market, the inflation-targeting regime adopted by the RBA, and the flexible nominal exchange rate, which has enabled the necessary appreciation of the real exchange rate to occur in a less disruptive manner.

Historically, for several years following a peak in the terms of trade, growth in investment and output per capita tends to be below average. As we have emphasised, the real exchange rate and the terms of trade generally move together. Consequently, the expected easing in the terms of trade, reflecting growth in the global supply of the bulk commodities, may be accompanied by falls in the real exchange rate. More generally, an increase in Australia’s competitiveness would help facilitate the macroeconomic adjustments necessary during the transition from the investment to production phase by providing support to sectors outside of the resources sector, thereby helping to rebalance growth in the economy. Reflecting the unparalleled magnitude of the expansion, the transition necessary is considerable and is likely to pose challenges to both firms and policymakers.

The current policy frameworks and institutional structures, which were important in facilitating better macroeconomic outcomes during the upswing than occurred historically, may also assist this transition.

That’s about as bearish as the central bank gets. BS’s Callam Pickering is an RBA graduate and follows through with his take:

In Australia, the end of a terms of trade boom has historically resulted in two years of below-trend growth before returning to trend after five years. However, this time I expect growth will be weaker and the return to trend may take longer.

First, the decline in mining investment is expected to be particularly nasty and this may result in more weakness than in previous terms of trade declines. Second, weak employment growth resulting from an ageing population suggests that not only will below-trend growth persist longer than in previous episodes, but when the economy does return to trend growth, that trend will be a lot lower than we have come accustomed to in the past.

We have enjoyed the benefits of the boom and now Australia has to get ready to face some significant economic challenges.

Advertisement

I will add that this all assumes strong ongoing Chinese growth, which the RBA seems unable to free itself from. If China slows further, which is my base case, then adjustment shifts from “considerable” to “epic”.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.