Veda has released its Consumer Credit Demand Index results for the December quarter of 2013, which registered flat consumer credit demand over the year, but big growth in the number of mortgage applications, although first home buyer demand continues to fall.

According to regular commenter and mortgage broker Peter Fraser, Veda are the largest credit recording agency in Australia, and every application for any formal loan through any retail lender is recorded with them. As such, results published by Veda should be taken seriously.

Advertisement

According to Veda:

Overall consumer credit demand for the December quarter compared to the same period in 2012 was flat (+0.4%) year on year, representing an easing in the pace of growth from the increase of 7.4% recorded in the September quarter.

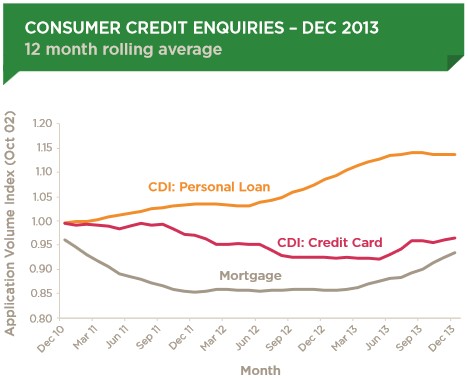

The index measures the volume of unsecured and secured credit enquiries that go through the Veda Consumer Credit Bureau by financial services credit providers in Australia.

Mortgage enquiries continued to rise, increasing by 15.3% year on year, an increase from 9.7% in the September quarter and 7.9% in the June quarter.

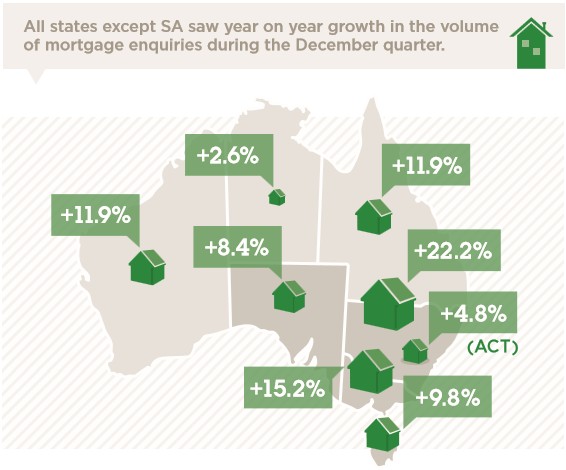

All states except SA saw year on year growth in the volume of mortgage enquiries in the December quarter. For the second consecutive quarter mortgage enquiries were strongest in NSW (+22.2%) with significant increases also recorded in VIC (+15.2%), QLD (+11.9%) and WA (+11.9%). Other states to experience mortgage enquiry growth were TAS (+9.8%), SA (+8.4%), ACT (+4.8%) and the NT (+2.6%).

“An extended period of low interest rates is supporting the lift in mortgage enquiries, which have stepped up a level and are now showing the strongest growth since late 2009. It is likely that we will see a continuing increase in the near term, along with sustained house price growth. We saw a further shift to mortgage applications from older demographics, with more first home buyers leaving the market,” said Angus Luffman, General Manager of Consumer Risk at Veda.

In contrast, credit card enquiries eased sharply in the December quarter. Nationally, annual growth in credit card enquiries eased to 2.4% in the December quarter, from 13.4% in the September quarter. Reduced demand for credit cards was apparent in all states with VIC (+6.9%) recording the strongest growth, followed by ACT (+6.2%), NT (+3.9%), WA (+2.6%), and NSW (+1.1%). Enquiries were flat in SA (+0.2%) and contracted in QLD (-0.2%) and (-1.0%).

“The December quarter was the second consecutive quarter of growth for credit card enquiries after an extended period of decline. Whilst it was a softer result than the previous quarter, the weeks leading up to Christmas had solid growth and 2013 ended with overall growth in credit card enquiries of 4.3%.”

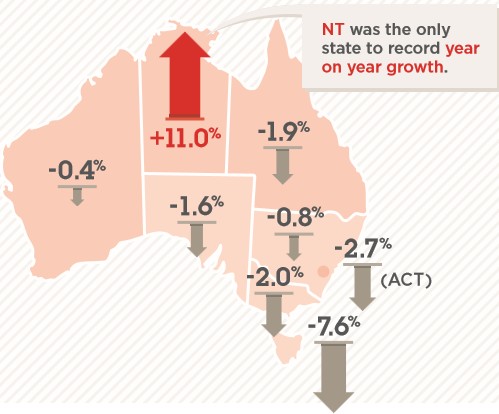

Nationally, personal loan enquiries recorded a decrease of -1.4% over the year to the December quarter. The NT (+11.0%) was the only state to record year on year growth, with reduced demand apparent in NSW (-0.8%), VIC (-2.0%), QLD (-1.9%), SA (-1.6%), WA (-0.4%), TAS (-7.6%), and the ACT (-2.7%).

“Personal loans enquiries have stabilised at a much higher level after a period of strong growth. This suggests ongoing challenging conditions for retailers of big ticket items and reflects a slowdown of car sales, which have shown no growth year on year, and a reduced demand for larger purchases among consumers in the mining states.

“The December quarter is typically a strong period for credit demand, reflecting the seasonal peak in spending associated with the Christmas period. The relatively weak outcome in loans and credit cards suggests low interest rates are not leading to a significant lift in consumer borrowing as households remain cautious about rising unemployment.”

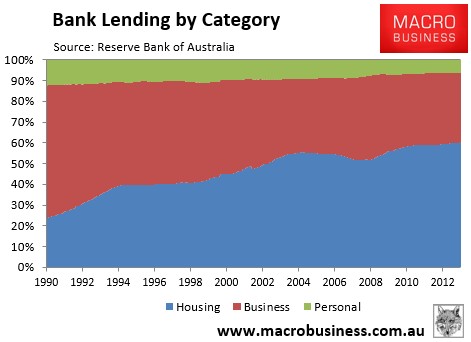

It’s worth also pointing out that the latest credit aggregates data from the Reserve Bank of Australia revealed that the share of credit flowing to mortgages hit the highest level on record (60.2%), with the share of loans flowing to business (33.4%) hitting a record low (see next chart).

Advertisement

This suggests that mortgage lending is crowding-out other forms of lending.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.