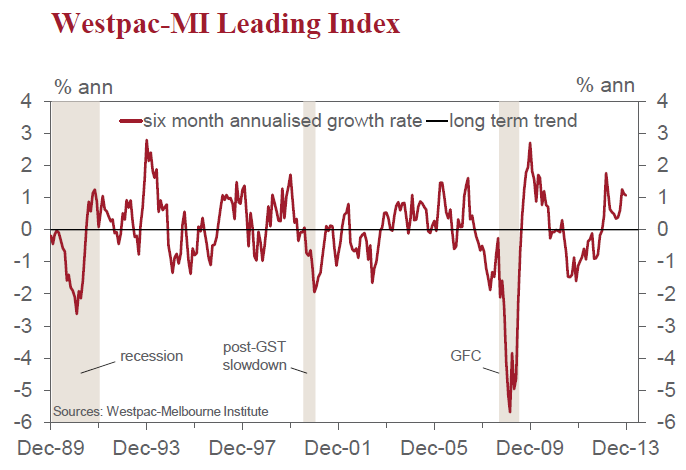

The six month annualised deviation from trend growth rate of the Westpac Melbourne Institute Leading Index of Economic Activity which indicates the likely pace of economic activity three to nine months into the future fell to 1.06% in December from 1.12% in November.

This slight moderation in the growth rate of the Leading Index is moving more into line with our own view that growth in the Australian economy in 2014 will remain below trend for another year. The Index is giving us a sound guide around the endogenous components of the growth outlook but cannot adequately capture the exogenous weakness associated with the downturn in mining investment and persistent below trend growth in government spending. Imposing those factors on the fairly fragile picture painted by the Index seems to be in line with our thinking that the growth pace in the economy in the first half of 2014 will be around 2.4% (annualised).

Note that this is the third release of the restructured Leading Index. Following an extensive review, significant changes were made to the composition of the Index in October 2013. The new Index is less prone to revision, timelier and quicker to detect turning points in the cycle. More detail on the changes is available on request.

Despite some softening in recent months, the growth pace of the Index lifted notably over the second half of 2013, from 0.46% in June to 1.09% in December. Component-wise, the main drivers of that pick-up were: US industrial production (+0.28ppts); the sharemarket (+0.22ppts); dwelling approvals (+0.16ppts); the yield spread (+0.12ppts); and the Westpac–MI Unemployment Expectations Index (+0.09ppts). These positives were partially

offset by bigger drags from hours worked (–0.19ppts) the Westpac CSI Expectations Index (–0.08ppts); and the RBA Commodity AUD Price Index (–0.04ppts).

Over the December month, the level of the Index fell from 98.55 to 98.64. Five of the eight components of the Index contributed positively: the ASX (up 0.6%); the Westpac-Melbourne Institute Expectations Index (up 2.0%); US industrial production (up 0.3%); commodity prices (up 3.3%); and the yield spread (rose 0.10ppts). Aggregate monthly hours worked were flat. Dwelling approvals fell 1.5% and the Westpac- Melbourne Institute Unemployment Expectations Index also contributed negatively (up 0.7% in the month, with higher readings indicating weaker labour market conditions).

The Reserve Bank Board next meets on February 4. The recent upward surprise on inflation precludes any further rate cuts for some months until the Bank is able to assess whether there has been a sustained upswing in inflation. We expect that the sharp depreciation in the AUD in 2013 was mainly responsible for the jump in inflation and, with the AUD stabilising as we move through 2014, the downward pressure on wages will deliver more benign inflation outcomes. With growth prospects remaining challenged we see a likely interest rate cut in August by which time the Bank will have had sufficient evidence to be comfortable with inflation prospects.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.