From the AFR today:

The prospect of a price ceiling for liquefied natural gas being set in Japan has compounded worries about mounting pressure on high-cost suppliers such as Australia.

It has also put a cloud over expectations of price increases for existing deliveries from producers such as Woodside Petroleum.

A move being considered by Japan’s powerful Ministry of Economy, Trade and Industry (METI) to extend its “Top Runner” initiative to cover LNG could set a $US13 per million British thermal unit limit on prices paid for LNG by utilities in Japan, the world’s largest importer of the fuel, according to Credit Suisse.

Such a price cap, which would include a requirement for prices to reduce further over time, would particularly hit new projects targeting the Japanese market such as Woodside’s Browse floating LNG venture and the expansion of ExxonMobil’s Papua New Guinea venture, Credit Suisse’s energy team said. The impact could also be felt by limiting price increases expected at Woodside’s Pluto project, and in price renegotiations due over the next few years by the North West Shelf venture, it added.

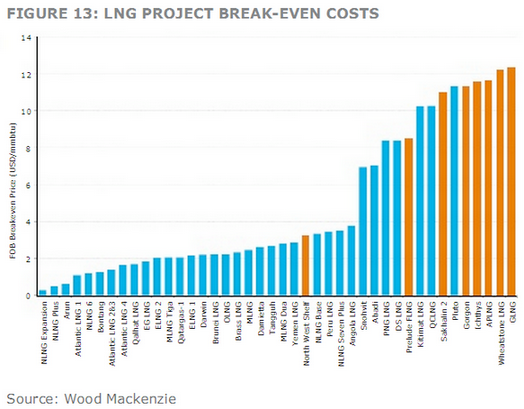

$13mmbtu! Here’s the cost curve for LNG:

This chart is now eighteen months old and has probably gotten worse.

There’ll be some protection for projects in their existing price contracts but if Japan puts a hard cap on LNG prices all earnings upside to these projects is gone and the late coming Queensland outfits in particular will face serious viability questions.