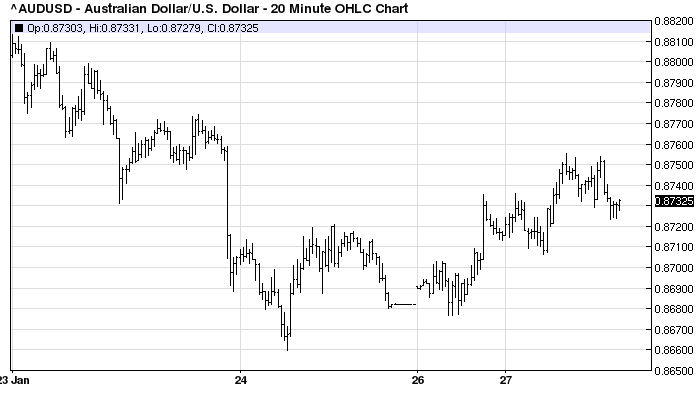

While we’ve all been enjoying Australian Day the rest of world has been not so quietly celebrating by flogging our currency. On Friday evening last week we plunged deeply into the 86’s as RBA board member Heather Ridout told markets we need 80 cents:

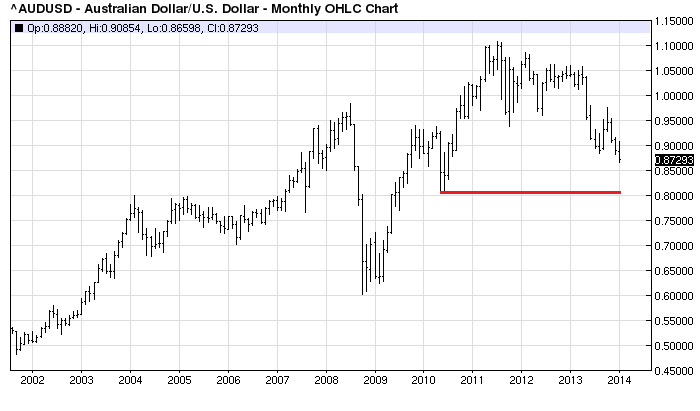

The technical damage on the weekly chart is done. The odds favour a return to 80 cents in the medium term:

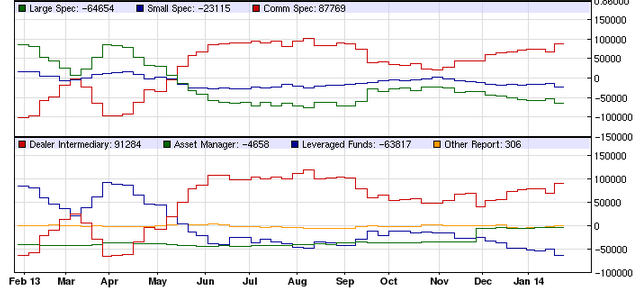

The currency is oversold. The recent Commitment of Traders report shows large and small speculators very short:

We may see a rally here. Indeed, the Australian dollar out-performed just about everyone in its bounce back last night:

However, with a backdrop of an emerging market currency rout triggered by the Chinese slowdown, as well as an overdue US equities correction, any rebound in the Aussie is on thin ice.

What has supported it most of all, in my view, is the successful resolution to China’s threatened shadow banking default. From the FT:

A Chinese fund company has avoided a high-profile default, reaching a last-minute agreement to repay investors in a soured $500m high-yield investment trust, in a case that had sent tremors through global markets.

China Credit Trust, one of the country’s biggest “shadow bank” institutions, raised Rmb3bn from investors three years ago for the investment, which was backed by loans to a coal miner that later collapsed.

Chinese authorities, alive to the ramifications for the country’s booming shadow banking sector, had been scrabbling to prevent a default. Nonetheless, investors were braced to lose their money when the fund matured at the end of January.

The “Credit Equals Gold No. 1” product – a tiny slice of China’s $1.2tn trust market – was sold through the private banking arm of Industrial and Commercial Bank of China to rich individuals rather than to retail punters.

Trust loans, which have typically been given to higher-risk borrowers such as property developers and mining companies, make up the largest slice of China’s vast shadow banking sector.

…The last-minute resolution in this particular case does not spell the end of trouble for the sector. Many analysts believe that the default of a Chinese trust product is now inevitable, and may even be desirable as the country moves to improve investor perceptions of credit risk.

“The underlying problem is a corporate sector insolvency issue, so there may be many more products threatening to default over time”, wrote David Cui, strategist at Bank of America Merrill Lynch, in a research note. “We suspect that, at a certain point, the involved parties will be either unwilling or unable to bail them out, which may trigger a credit crunch.”

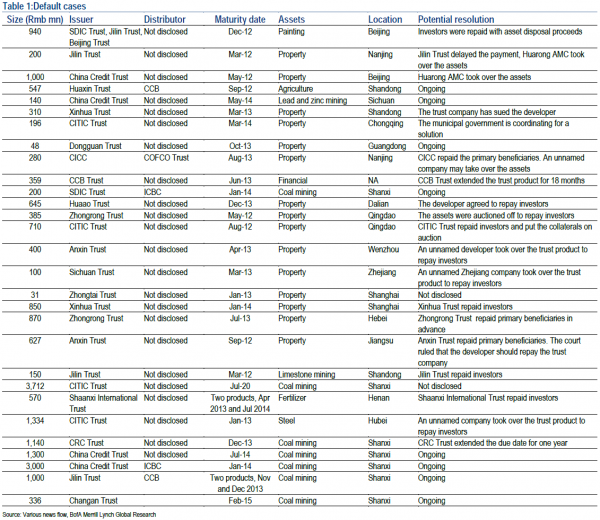

The underlying problem is Chinese rebalancing which is driving insolvency in yesterday’s red hot sectors with much more to come. Also from David Cui via Zero Hedge:

Australian assets are sensitive to Chinese liquidity via iron ore, bank funding, economic growth and the dollar. The support for the latter is temporary.