The share of economists predicting the Federal Reserve will reduce bond buying in December doubled after a government report showed back-to-back monthly payroll gains of 200,000 or more for the first time in almost a year.

The Federal Open Market Committee will probably begin reducing $85 billion in monthly bond purchases at a Dec. 17-18 meeting, according to 34 percent of economists surveyed yesterday by Bloomberg, an increase from 17 percent in a Nov. 8 survey. In November, 53 percent predicted a tapering in March, compared with 40 percent in yesterday’s poll of 35 economists.

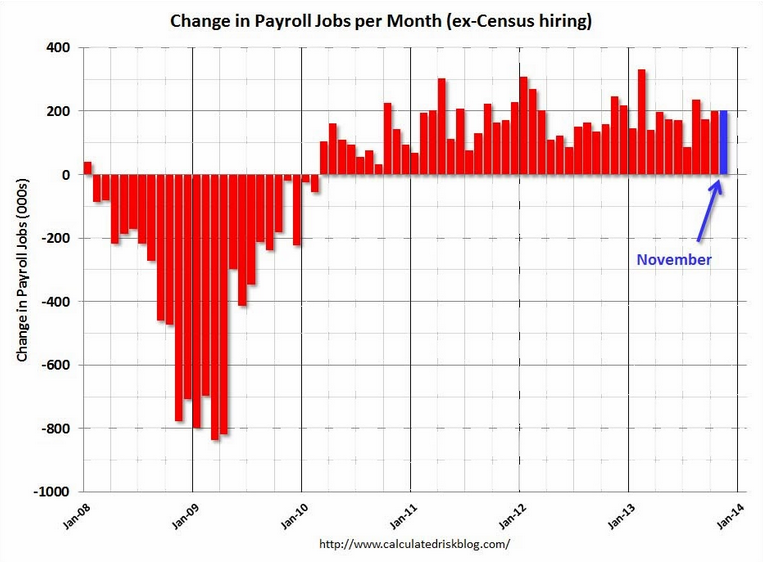

The jobless rate fell to a five-year low of 7 percent last month as payrolls swelled by 203,000 after a revised 200,000 increase in October, the Labor Department said yesterday. The November gain exceeded the 185,000 median forecast of 89 economists surveyed by Bloomberg.

“Clearly the economy is performing far better than the FOMC expected, and there’s no reason not to get started with tapering,” said James Smith, chief economist at Parsec Financial Management Inc. in Asheville, North Carolina, and a former economist at the Fed. He predicts the Fed will reduce monthly purchases to $65 billion in December.

Both the number of unemployed persons, at 10.9 million, and the unemployment rate, at 7.0 percent, declined in November. Among the unemployed, the number who reported being on temporary layoff decreased by 377,000. This largely reflects the return to work of federal employees who were furloughed in October due to the partial government shutdown.

…The civilian labor force rose by 455,000 in November, after declining by 720,000 in October. The labor force participation rate changed little (63.0 percent) in November. Total employment as measured by the household survey increased by 818,000 over the month, following a decline of 735,000 in the prior month. This over-the-month increase in employment partly reflected the return to work of furloughed federal government employees. The employment-population ratio increased by 0.3 percentage point to 58.6 percent in November, reversing a decline of the same size in the prior month.

…The change in total nonfarm payroll employment for September was revised from +163,000 to +175,000, and the change for October was revised from +204,000 to +200,000. With these revisions, employment gains in September and October combined were 8,000 higher than previously reported.

Advertisement

The CR chart does a nice job of illustrating a point I’ve made before, which is the cyclical ebb and flow of US employment around Christmas as retail hiring and inventory builds boost the labour market. Even so, overall this year was more consistent for hiring.

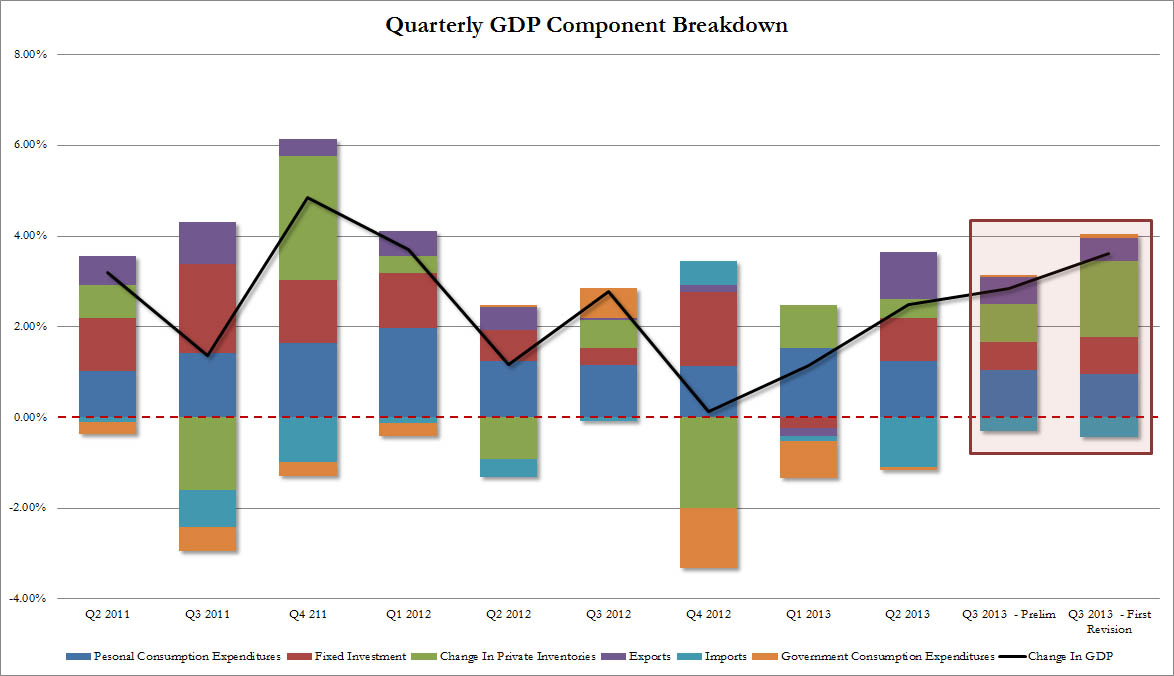

But these cycles are important. The tearaway GDP figure of last Thursday evening was a case in point. GDP was very strong largely on said inventories:

Advertisement

In short, there will be strong give back in growth figures for the few quarters. Back to jobs, JPMorgan has a good summary:

The labor market had another solid month, generating a net 203,000 jobs last month. The big story for November, however, was the unemployment rate, which dropped 0.3%-point to 7.0%. That decline occurred as the participation rate only partly reversed October’s huge drop, and at 63.0% the participation rate is 0.2%-point below the September level. The continuing disappointment in labor supply will prompt some soul-searching at the Fed, where the house view has been that the participation rate would bounce back once job creation picked up. Over the past two years the labor market has created almost 4-1/2 million jobs, yet the participation rate has continued to decline. At some point the Fed will have to accept that the labor supply is trending lower, and hence that the decline in the unemployment rate truly represents progress toward their full employment mandate. In the meantime, we still think December is a close call but that the FOMC will hold off on tapering until January. While fiscal issues appear less ominous and employment prospects look favorable, we still think that before pulling back on asset purchases the Fed would like to see more evidence that housing is stabilizing and that inflation is finding a floor.

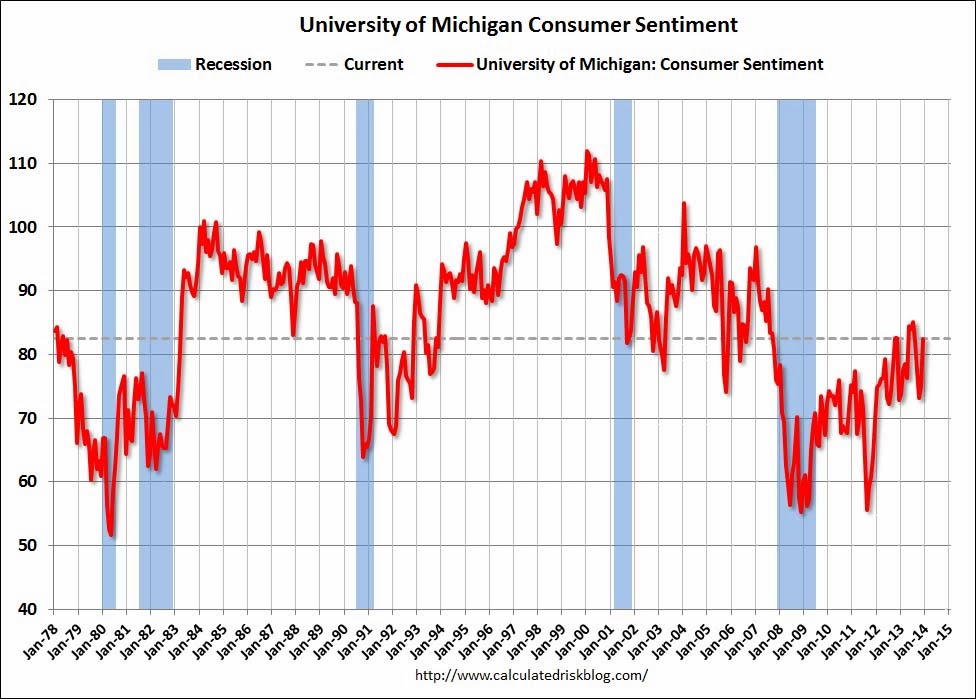

I agree on December and think January is also unlikely given shutdown data will still be washing through the housing market and the new debt-ceiling deal is not yet done. However, data is strong enough for me to shift my current focus from June to March of next year. That is born out by sharp snap back in consumer sentiment Friday. Again from Calculated Risk:

Advertisement

The preliminary Reuters / University of Michigan consumer sentiment index for December was at 82.5, up from the November reading of 75.1.

PCE spending also looked solid for October at 0.3 despite weak income growth. The consumer appears to be weathering the political storm OK.

But can they weather higher interest rates? That’s what’s coming. The 10 year bond yield was up two points to 2.88%, and is trending towards a new high at 2.97%. Moreover, the 30 year, which benchmarks mortgage rates, is already at a new high of 3.92 and looks to have a yield bullish (bearish for face value) ascending triangle chart:

Advertisement

Perhaps a more convincing breakout is needed but I wouldn’t bet against it. And that’s the rub. Whether we get actual tapering or not, we’re already getting rapid tightening.

Interestingly, wider markets did not back a firming taper. Stocks flew, the US dollar was stable, gold was firm, the Australian dollar dumped sharply on the employment figures but rallied all night to recapture the 91 cent handle. Some of these moves may be technical but they also represent a lack of conviction about taper timing. It’s either that, or the taper has been priced in.

A top Federal Reserve official said on Friday he was open to reducing the U.S. central bank’s bond buying stimulus program this month, although he would like to see a stronger labor market first.

Chicago Fed President Charles Evans said hiring data released earlier in the day showed the economy was improving, but he wasn’t fully convinced it was time to reduce the pace of bond buying.

“I’ll be open-minded,” Evans said in an interview with Reuters Insider when asked about the December meeting. “Everything else (being) equal, I would like to see a couple of months of good numbers, but this was improvement.”

That’s the best policy. My view at this point, then, is the front runner is a move in March then a half length to June and no taper, with Dectaper another half length behind.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.