Find below the latest from Westpac’s Elliot Clarke on the taper:

A 6 December Bloomberg poll of US economists showed 34% expect an initial taper at the December meeting and a further 26% anticipate a January move. Our base case remains no taper through 2014 for a number of important reasons.

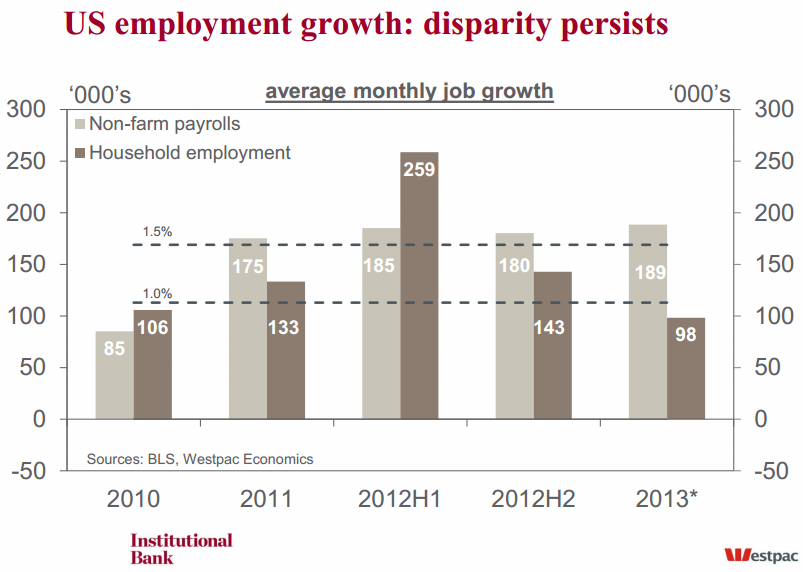

Starting with the labour market, October and November’s respective 200k+ prints have been seen by proponents of tapering as evidence of accelerating momentum. But, while the current 193k three-month average is well above that at the time of the September ‘no taper’ decision (148k, revised to 166k), it is weaker than the average of the five months to May (199k), and only marginally above 2012’s 183k monthly average. The implication: there has been little pick-up in payrolls in 2013.

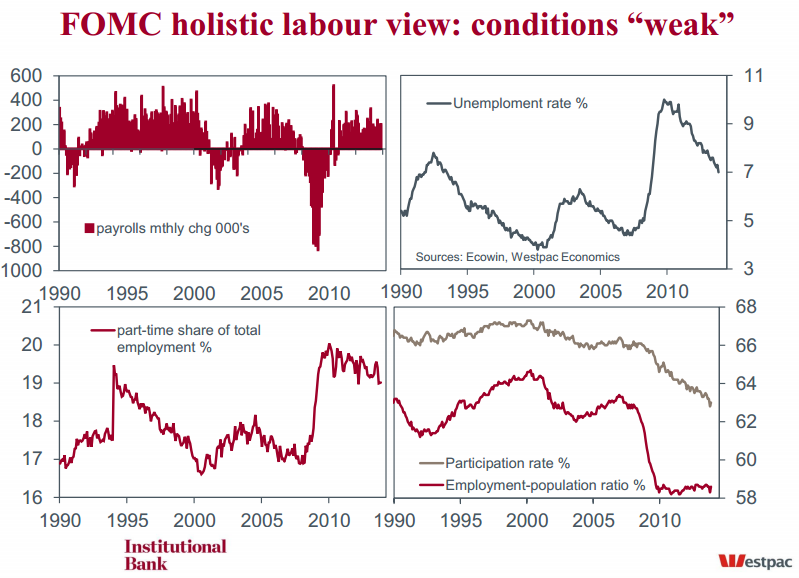

From the household survey, the market’s key November take out was the 7% unemployment rate – a previously cited (later distanced) indicator of ‘considerable improvement’ in the labour market, as assessed by the FOMC. The issue with focusing on this number is that it is the result of a persistent decline in the participation rate, the result of younger cohorts remaining out of the workforce and older participants now exiting. We prefer to focus on the employment-to-population ratio as our key indicator of cumulative improvement in the labour market, on which basis there has been little.

On activity, again the Q3 GDP second estimate headline received the attention, but it was the detail that mattered. Abstracting from the abnormally large inventories contribution, domestic demand was sub-trend, with annualised growth of 1.8%, 1.5%yr. Of more concern, the foundations for the Q3 gain look decidedly shaky. Consumption growth experienced its weakest quarter since 2009, with momentum driven by credit-supported durables spending as services growth remained weak. October partial data points to this trend continuing into Q4. For investment, following a flat Q3, a decline in Q4 is a material risk. As outlined last week, perhaps with the exception of large-scale manufacturers, conditions are not conducive to a near-term increase in capacity, limiting investment to efficiency-oriented initiatives.

One bright spot for activity which is unquestionably positive is this week’s announcement of a compromise budget deal. The deal (if passed) will see some $60bn of spending cuts removed through FY15, the majority in FY14. The direct impact on growth will be limited to around 0.1ppts for 2014, but the indirect impact through improved confidence is an upside risk. This is until we once again hit debt ceiling negotiations, likely in Q2, ahead of the November mid-term election.

That no compromise has been reached on extending unemployment benefits past 31 December could result in an interesting near-term dynamic for the unemployment rate: long-term unemployed no longer receiving extended benefits may be regarded as having left the workforce by the BLS, potentially resulting in a sub-7% unemployment rate in early 2014. Again, this will not be an ‘improvement’ born of employment growth, but rather re-categorisation.

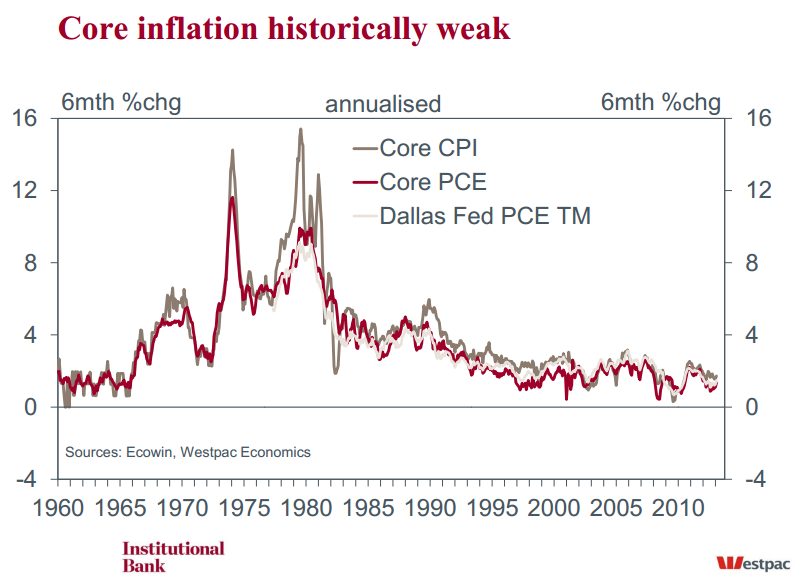

The absence of real momentum in activity is made all the more clear when one considers available prices data, with inflation historically weak on all measures. The FOMC’s preferred inflation measure, the personal consumption deflator, has decelerated to 0.7%yr in headline terms and 1.1%yr less food and energy. The three-month annualised pace for the core measure is only marginally higher at 1.3%. At its current level, annual core inflation is close to its lowest point in this recovery (0.9%–1.0%yr), last seen in late-2010 and mid-2009. The absence of inflation pressures should unnerve the FOMC, not merely because inflation is so far below their longer-run 2% goal, but because of what this says about organic, demand-driven revenue and wages growth – needed to stoke greater investment and income (not debt) funded household consumption.

So, where does this leave us with the FOMC? Our forecast for no taper is based on what would be best for the economy. Growth has disappointed for four years and we expect it will for a fifth. Equally, the FOMC is yet to annunciate that the efficacy of QE has been questioned or that the risks associated with continuing the policy outweigh its benefits, so we cannot base a case to taper on either point.

That being said, we cannot entirely rule out an initial taper at the January or March meeting, based once again on hopeful expectations of next year and perhaps fears of never being able to normalise policy. If it transpired, a sub-7% unemployment rate driven by labour-force departing unemployed could get the committee over the line. Any initial taper would be small and come with an offsetting ‘expansionary’ adjustment to forward guidance and/or a cut in the interest rate paid on excess reserves (IOER) – in net terms, a broadly neutral policy shift.

If the FOMC does move to taper, we expect the tapering process would quickly grind to a halt later in H1 2014 as growth disappoints and momentum wavers amidst higher market rates. The net effect would be a monthly purchase rate of $70–$80bn from Q2 onwards and a 2014-end balance sheet target modestly below our current $5.05trn forecast. A final point: it would not be prudent to eliminate the possibility of an increase in purchases later in 2014.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.